The 5-Minute Guide to Exelon's Stock

Image Source: Exelon Corporation corporate website

Exelon is an electric utility. On the surface that sounds pretty simple, but there's more to understand about this company. Here's the down and dirty about what you need to know before you dive in.

How Exelon makes moneyAt its core, Exelon generates and sells electricity. That's pretty simple to understand, but there are a lot of moving parts before you switch a light on in your house. For example, Exelon owns and operates power plants and owns and maintains the power lines that take power from the plant to your home. From beginning to end, this is a capital-intensive industry.

Moreover, utilities are often regulated. So the government gets to tell Exelon how much it can earn in profits. That might not sound so good, except that Exelon is basically being granted a monopoly in the regulated regions it serves. The way a regulated utility grows its top and bottom lines is by spending money on new power plants and on maintaining its existing assets. So future spending plans are key to understanding how much growth lies ahead for a utility. But that has to be juxtaposed against how generous regulators are in allowing a utility to pass those costs on to customers.

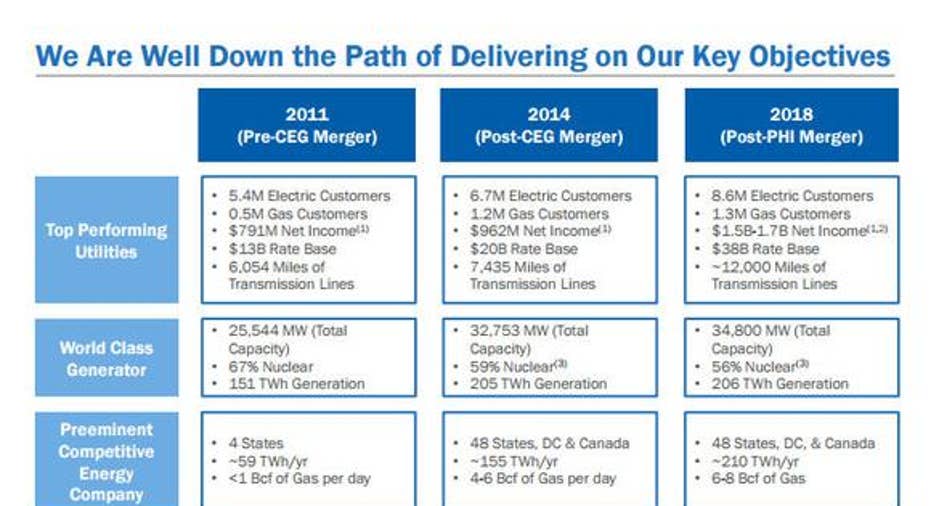

Exelon's changing profile. Source: Exelon.

Like Duke Energy and other peers, Exelon has been shifting more and more toward the regulated space. For example, in 2011 only about 30% of Exelon's business was regulated. But through mergers, including the proposed acquisition of Pepco Holdings , it hopes to get that number up to 60%. This, however, is well below the regulated businesses of competitors. Duke, for example, gets around 90% of its top line from regulated power markets. The rest of Exelon's revenues come from selling power to other utilities on the open market, which is a much more volatile revenue stream.

The same, but differentAnd that's the first big important theme for you to understand. Exelon is trying to become more like a boring old utility, but it isn't just a boring old utility. Assuming the Pepco deal goes through (the deal is getting significant push-back from regulators), Exelon will still generate around 40% of its revenues from the more volatile independent power generation business.

That's been a rough space of late, because historically low natural gas prices have led to low energy prices. This was a big reason behind Exelon's decision to trim its dividend in 2013. That's not something a utility, or any other company, wants to do. For example, Duke and Southern Company have increased their dividends annually for 11 and 15 years, respectively. But both have much greater exposure to regulated markets.

The key takeaway here is that Exelon's results aren't going to be as steady as what you might expect from regulated peers. That can be a bad thing, like now, when power prices are low. Or it can be a good thing. In fact, if natural gas prices were to move notably higher and electric prices followed suit, the 40% of Exelon's business that sells power to other utilities would very likely become much more profitable.

Exelon's nuclear power fleet. Source: Exelon.

Different in other ways, tooThat's great, but there's one more vital piece of information to understand about Exelon and how it's different from other utilities, regulated and otherwise: nuclear power, which accounts for roughly 60% of Exelon's production capacity. At Duke that number is 17%, with Southern's nuclear capacity at an even smaller 7%. Essentially, Exelon has bet heavily on nuclear. In fact, it's the largest nuclear power plant owner in the United States.

Like its combination of regulated and unregulated businesses, nuclear is something of a mixed issue. On one hand, people have a dim view of the energy source. Disasters like the one in Fukushima, Japan, don't help with that image. And Exelon is pretty much dealing with constant calls for its plants to shut down because nuclear is thought of as dangerous. The thing is, despite a few high-profile disasters, nuclear operates safely the vast majority of the time. So Exelon's bet is one that will draw scrutiny and could expose investors to a large disaster, but it will most likely be just fine.

The flip side of this negative view is that nuclear doesn't emit carbon as it creates electricity. So it's a clean fuel source for the environment. Moreover, unlike other clean options, such as solar and wind, nuclear runs constantly at high capacity factors. And, once built, it's fairly inexpensive to generate power from a nuclear plant. So there are some things to like about nuclear that, as carbon fuels get phased out, could make nuclear less of an image liability than it is today. But you had better believe that this image upgrade will come to pass if you buy Exelon.

How to think about ExelonSo when you look at Exelon, you have to think of it as two different parts. One is the regulated business, which is boring and steady. The company is working to grow that via acquisition and will continue to benefit as it invests capital in the business. This entire side of the company, however, is at the disposal of regulators. That's usually not too big a deal, though the push-back on the Pepco merger shows that it can, at times, cause troubles. The regulated business, though, should be looked at and valued like any other regulated utility.

The other part of the business is the non-regulated power generation side of things. That's going to be driven by the price of power on the open market. Right now that's a rough business, but if power prices rise it could quickly turn into a real asset. You need to be aware of the risks as well as the potential benefits here if you buy Exelon. And this business needs to be valued like any other independent power producer.

So to get a full view of Exelon, you need to look at it as two parts first and then put them together. But don't forget about the nuclear overlay. You might decide that this alone is a reason not to own the utility or that it's a great reason to own it. But with so much exposure, you need to factor nuclear into your equation in some way.

The article The 5-Minute Guide to Exelon's Stock originally appeared on Fool.com.

Reuben Brewer has no position in any stocks mentioned. The Motley Fool recommends Southern Company. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.