The 4 Best Dividend Stocks in Waste Management

There are few industries better suited to producing reliable streams of cash for dividends than waste management. It's the type of business that profits from something we do on a daily basis without much thought: throwing stuff away. Companies can take that routine daily task and turn it into an endeavor with high rates of return for investors and one that typically pays a substantial dividend.

There aren't many players in the waste management industry, and a few large ones dominate it. That said, some of them merit an investment more so than others. If you are interested in stable dividend-paying stocks in this business, take a look at Waste Management (NYSE: WM), Republic Services (NYSE: RSG), Covanta Holding(NYSE: CVA), and Veolia Environnement (NASDAQOTH: VEOEY). Here's a brief look at why each of these stocks could make for an attractive dividend investment

Image source: Getty Images.

The traditional stalwarts

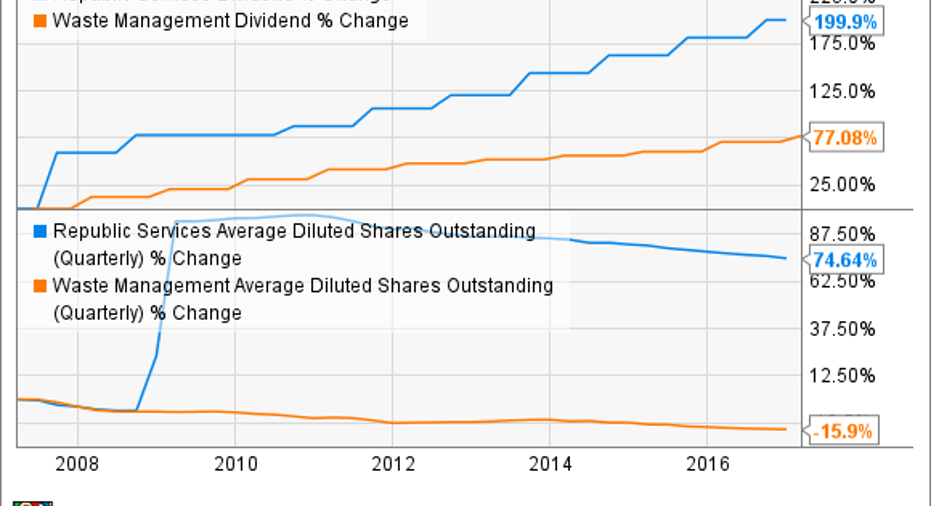

Waste Management and Republic Services are the big fish in theindustry. Combined, the two control about 60% of the waste collection and landfill business in the United States. They are remarkably similar in their operations and the way they reward shareholders over time.

Both generate revenue from three key areas: waste collection, transfer station and landfills, and recycling. None of these sectors are what you would call high growth as it is a saturated market for these services. However, these companies can generate modest growth from either pricing increases from their existing services or from making acquisitions.

Keep in mind that the name of the game for these enterprises is to keep operational costs low. One strategy that both have employed isto convert their waste collection vehicles to run on natural gas instead of diesel. In many cases, they use the methane gas generated at their landfills to fuel those trucks, which significantly decreases fuel costs. These sorts of expense controls help to produce high rates of free cash flow that both companies use to pay rich dividends and buy back lots of stock to improve earnings per share over time.

RSG Dividend data by YCharts.

Today, shares of Waste Management and Republic Services sport dividend yields of 2.35% and 2.05%, respectively. It's also worth mentioning that both trade at a decent premium to their historical averages right now -- enterprise value-to-EBITDA ratios for Waste Management and Republic Services stand at 12.0 and 11.4 times, respectively. Since this a slow-growthindustry, it may not be the best time to buy stock in either because there is a lot of optimism baked into those valuations. That said, you can't go wrong if you want a stable dividend stock in the waste management industry.

The specialist

Aside from the traditional model of collecting and disposing of waste offered by Waste Management and Republic Services, there isone specialty waste handling company that is worth a look if you want a larger dividend yield: Covanta Holdings. Covanta, like its larger peers, generates a significant portion of its revenue from waste collection and recycling. What separates them, though, is how they handle that waste. Rather than putting all refuse into a landfill, Covanta burns it in waste-to-energy facilitiesto generate electric power.

Being able to sell electric power to the grid gives Covanta another revenue stream, and is a relatively stable source of income since 87% of its energy sales are either set with fixed contract rates or are hedged. This means that about 85% of Covanta's overall revenue is either contracted or hedged and affords it a respectable adjusted EBITDA margin of 25%

One thing that Covanta offers that the other waste handling giants don't is some modest international exposure. Covanta currently has a new energy-from-waste facility under construction in Ireland and has plans to expand even further in the U.K. This new facility, coupled with some internal efforts to improve recovery rates of metals and other recyclable materials in the waste stream, should generate 3%-5% annual growth in EBITDA. That doesn't sound like much, but for the waste business, that is remarkable.

From an investor's standpoint, what separates Covanta from its peers is its payout to investors. Today, shares of Covanta have an incredibly high yield of 6.6%. Part of the reason for the high yield is that the company is carrying a high debt load -- net debt to EBITDA is 7.78 times-- and there are some fears that any issues with the new Dublin facility could put some real financial strain on the company.

Covanta is an opportunity for investors to generate a high yield from a conventionally low-growth industry. Also, if the company pulls off this growth plan without a hitch, investors could benefit from a decent share price gain.

The global powerhouse

While Covanta does provide some modest global diversification over the domestic giants of the waste industry, Veolia Environnement is a waste management stock that offers real global diversity. The French conglomerate not only operates solid waste handling around the globe but also water treatment, wastewater treatment, renewable energy from waste, and industrial cleanup services. In many cases, these are regulated utilities that generate fixed rates of returns, but they provide stable cash flows that enable Veolia to pay investors a generous dividend that yields 4.59%.

Just to give you a snapshot of the global reach and diversity of Veolia, here are four of the largest contracts it signed in 2016:

- A $3.3 billion contract with China's Sinopec to provide complete water cycle treatment at a petrochemical site

- A 30-year, $1.26 billion contract for solid waste collection and disposal services in the U.K.

- A 15-year, $870 million contract to provide drinking water and wastewater services for the Republic of Armenia

- A 10-year, $500 million contract extension forsanitation services in Milwaukee, Wisconsin

One of the usual downsides of operating such a sprawling, diverse business can be a lack of cost control. Fortunately for investors, operational expenses have been a managerial point of focus. From 2012 to 2016, return on capital employed has improved from 4.9% to 9.2%. Management hopes to build on these improvements by cutting another $650 million from its operational expenses between 2016 and 2018.

These initiatives over the years have turned Veolia into a company that produces high rates of free cash flow, which supports its dividend as well as reduces its notably high debt load. If Veolia's management can continue on this track, then the stock should remain a very attractive dividend investment.

10 stocks we like better than Waste ManagementWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Waste Management wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Tyler Crowe owns shares of Waste Management. The Motley Fool owns shares of Waste Management. The Motley Fool recommends Republic Services and Veolia Environnement (ADR). The Motley Fool has a disclosure policy.