The 1 Stock I Would Buy Right Now

Image source: Getty Images.

About once a month, I like to take a look and answer the question: If I were to invest in one stock this month, what would it be? Right now, it's tough to find a better value for the money than HCP, Inc. , a healthcare real estate investment trust that's had a turbulent year so far but otherwise has a nearly flawless track record of performance.

HCP: The one-minute version

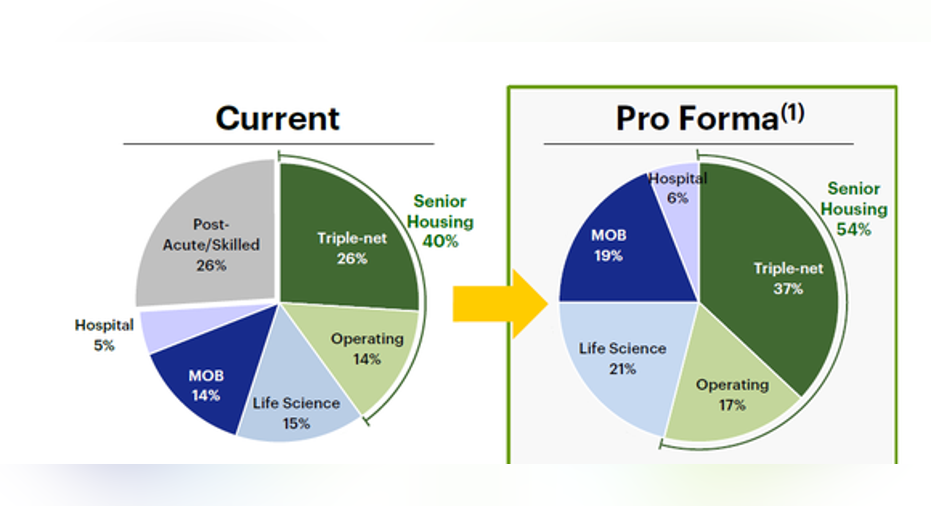

HCP is one of the "big three" REITs that specialize in healthcare properties, along with Welltower and Ventas . HCP owns approximately 1,200 properties, spread out across senior housing (40% of portfolio), post-acute and skilled nursing (26%), life science properties (15%), medical offices (14%), and hospitals (5%).

The business model is relatively simple -- invest in high-quality facilities in attractive markets, alongside some of the best operators in the business. For example, HCP's largest senior housing operating partner is Brookdale Senior Living, the largest operator of its kind in the U.S. All leases are triple-net (tenants pay taxes, insurance, and maintenance), and all are guaranteed by Brookdale and have staggered maturities.

HCP's medical office portfolio consists of partnerships with some of the best hospital operators in the U.S. And the life sciences portfolio derives the vast majority of its income from well-established tenants such as Genentech, Duke University, Johnson & Johnson, and Pfizer.

HCP's track record is quite impressive. The company has increased its dividend for 30 consecutive years, and has produced a 13.6% annualized return during that time -- including this year's price drop brought on by dismal performance of the post-acute/skilled nursing portfolio, which I'll discuss more in a second. At any rate, this is exceptional performance to sustain over three decades.

Data source: HCP company presentation.

The upcoming spinoff

Along with its first-quarter earnings report, HCP announced its intentions to spin off its troubled HCR ManorCare post-acute and senior housing portfolio into a newly created REIT known as HCP SpinCo, Inc. I'm still hoping they come up with a better name for the new REIT, but there are two clearly defined goals of the spinoff.

First, the company wants to unlock value in the HCR ManorCare assets by establishing a focused management team that will be able to use strategies that wouldn't be suitable while the assets are still part of HCP. SpinCo CEO Mark Ordan has led successful turnarounds in the past, and his compensation is tied to creating shareholder value -- something I love to see in situations like this.

The other goal is to create an HCP portfolio that is a blue-chip portfolio of healthcare properties. After the spinoff is completed, HCP will have a rock-solid portfolio of senior housing, life science, and medical office buildings in growing markets, and 95% of the properties will generate their income from stable private-pay sources, a sector-leading amount.

Data source: HCP company presentation.

This stability should lead to more financial flexibility, including increased borrowing ability and lower-cost funding.

Of course, there are bound to be some "growing pains" as both companies adjust to their independent operations, especially in regards to SpinCo. However, the reasons for the spinoff certainly make a lot of sense, and the potential for value creation is there.

The valuation makes up for the risks

Perhaps the most compelling reason to buy HCP pre-spinoff is the cheap valuation. Healthcare REITs in general are trading rather cheaply when compared to other types of real estate, but HCP is trading at a particularly steep discount.

When valuing REITs, the best earnings metric to use is funds from operations, or FFO, as opposed to net income, which is appropriate for most other stocks. A full discussion of the reasoning for this can be found here, but for now just know that FFO is the most accurate measurement of a REIT's income available to pay dividends and to reinvest.

Having said that, here's how HCP compares to the rest of the "big three":

|

Company |

Share Price |

2016 FFO Guidance |

P/FFO (Midpoint) |

|---|---|---|---|

|

HCP, Inc. |

$35.10 |

$2.77-$2.83 |

12.5 |

|

Welltower |

$73.41 |

$4.50-$4.60 |

16.1 |

|

Ventas |

$69.71 |

$4.07-$4.15 |

17.0 |

Share prices as of 6/21/16. FFO guidance obtained from each company's first-quarter earnings report. Adjusted or normalized FFO figures are used, when available.

Invest in HCP for the long term

HCP is a compelling buy right now due to its rock-bottom valuation, and the potential for value creation on both sides after the spinoff occurs later this year. However, no stock capable of double-digit returns is without risk or volatility, so it's entirely possible that investors will face a turbulent ride over the next year or two.

However, I'm completely confident that HCP shareholders will achieve excellent investment returns, as long as they approach their investment with a long-term mentality. There are some pretty compelling reasons to invest in healthcare real estate for the long run, and as soon as HCP figures out the best way to operate post-spinoff, there is certainly some money to be made.

The article The 1 Stock I Would Buy Right Now originally appeared on Fool.com.

Matthew Frankel owns shares of HCP and Welltower. The Motley Fool owns shares of and recommends Johnson and Johnson. The Motley Fool recommends Welltower. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.