Starting to Invest in 2016? Here's What You Need to Know

Image source: Taxcredits.net.

Before you invest another dollar, there are some important things every investor should know to maximize returns, avoid unnecessary costs and losses, and even reduce taxes. Most importantly, it could keep you from making the most common mistake almost every investor repeats.

Use the best tool for the jobThings such as taxes, fees, and matching contributions can have a huge impact on your returns. For instance, if you're not using one or more of the following, you'll probably end up with less money when you need it than you would have otherwise:

- 401(k) or similar through work.

- Roth or traditional IRA with additional funds.

- 529 college savings plan.

Contributions to these kinds of accounts come with a bevy of tax benefits. For example, for every $1,000 you're contributing to a taxable investing account instead of your 401(k), you're paying an extra $150 in federal taxes, based on median U.S. income and tax brackets.Your employer may also match contributions to your 401(k). That's free money -- and it really adds up. If your employer matches 1% of your pay, we're talking about $35,000 over 30 years, based on a 5% annual rate of return.

If your employer doesn't offer a retirement plan, contributions to a traditional IRA are tax deductible in the same manner. Roth IRA contributions aren't tax deductible, but the benefit happens when you retire. While 401(k) and traditional IRA distributions are considered taxable income, Roth distributions are tax-free. Who doesn't want tax-free income in retirement?

If you're saving for a child's college, a 529 plan would also cut taxes, since both growth, and distributions for college expenses, would be federal (and state in some states) tax-free.

Simply contributing to the right account could be worth tens of thousands of dollars in tax savings alone.

Market crashes aren't a bug -- they're a featureFellow Fool Morgan Houselput it best:

The key istime inthe market, and nottimingthe market. So if you're saving for your retirement in 20 or 30 years, you're almost guaranteed to see your portfolio quickly lose 10% of its value dozens of times, fall by 20% 10 times, and possibly fall by half once or twice. Those are losses you'll see every time you look at your portfolio.

But it's how much thinhs go upin between the dropsthat matters. Case in point:

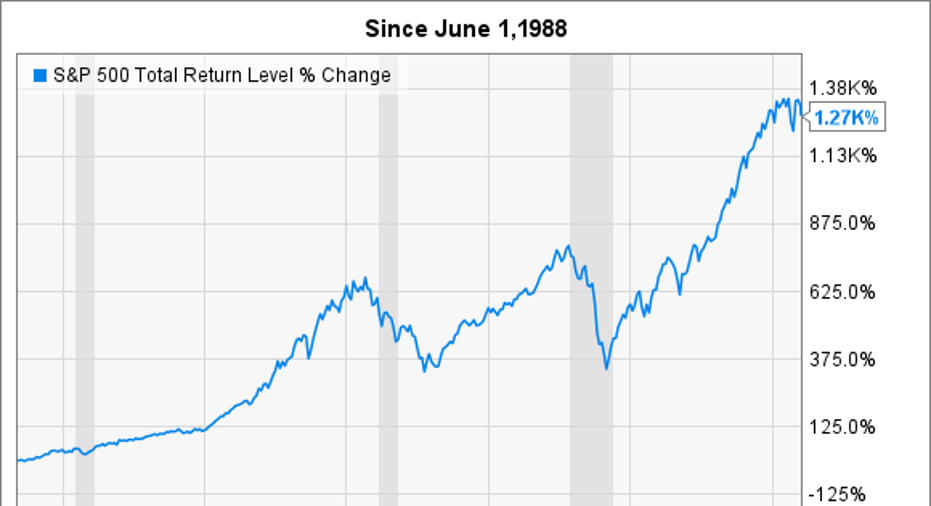

If someone had invested $10,000 in a fund that matched the total returns (i.e., stock appreciation and dividends) of the S&P 500on June 1, 1988, that person would have $127,000 today. America has gone through three recessions, two major wars, and the worst global financial crisis since the Great Depression, yet through all of that, anyone could have made 12 times the money simply by investing in a large group of U.S. stocks, and then doing nothing for 27 years.

Even after thosehugedrops in 2001 and 2008, our theoretical investor was still way ahead of the starting point. That's timeinthe market.

Buy businesses, not stocks One way to help avoid short-term mistakes is by keeping in mind that you own a piece of a real business. If you make the right decisions, you'll own companies with durable competitive advantages, trustworthy management, and a strong market for their products or services.

Not only can this business-focused approach lead you to invest in higher-quality companies, but it will also be a hedge against letting your emotions take control when the next inevitable downturn happens. After all, if you understand that the business behind the ticker is strong, you'll be much less likely to sell simply because the market is falling.

Now get out of the wayInvesting isn't easy -- but we shouldn't make it harder or more complicated. Let's look at what we know, and what we don't.

- We know the market historically goes up more often than it goes down.

- We know we can't reliably predict when it will go down.

- We know what our goals, objectives, and time horizons are.

Put it together, and it's simple. Invest. Stay invested as long as possible. And while none of the things mentioned here guarantee you'll outperform the market, they'll almost definitely help you avoid costly mistakes, and you'll achieve greater wealth than you would've otherwise.

The article Starting to Invest in 2016? Here's What You Need to Know originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.