SolarCity: Show Me the Money

Amazon.comhas a "check-in" period every few years as Wall Street tries to find out if the company can generate real cash flow. It appears the market may be doing the same thing with SolarCity lately, as shares have crumbled more than 60% from all-time highs in mid-2015.

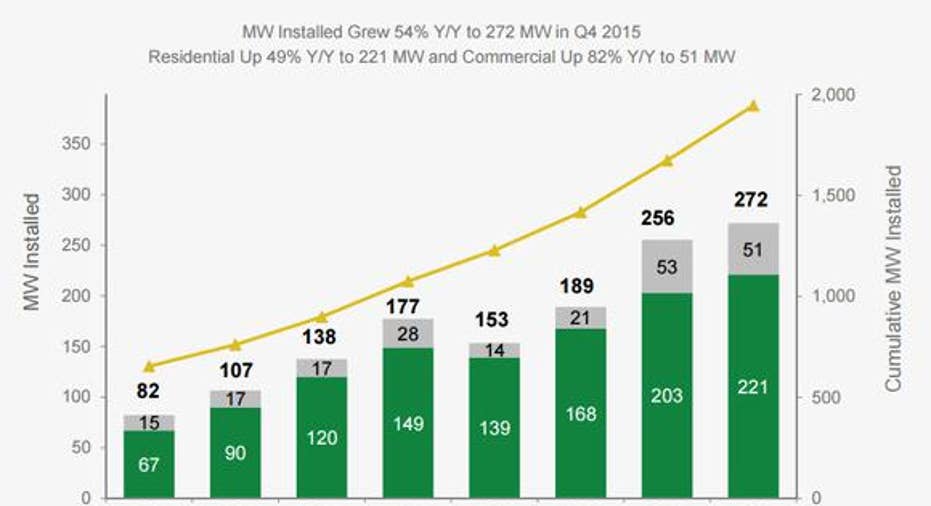

In its fourth-quarter 2015 earnings release late last month, the company reported record MWs, which rose at a healthy pace of 73% to 870 MW. The market wasn't excited by underperformance in commercial installations, mainly from pushed-back big projects and missed construction deadlines. Also, lower-than-expected Q1 guidance weighed on shares.

Image source: SolarCity presentation.

SolarCity's growth engine and ability to generate cash flow were on the minds of both analysts and management during the company's fourth-quarter earnings call. Let's examine the key takeaways for investors to focus on and their implications going forward.

Show me the moneyAlthough the market wasn't happy with the company's recent outlook for 180 MW in Q1 2016, the knock on SolarCity has been the inability to show any real profits since goingpublic. As Fools, we want growth; we just don't wish to pay an outrageous price for it. That's what makes me so upbeat about the most recent earnings report. CEO Lyndon Rive seemed to agree when he said: "The primary focus of the company is on cash generation, with growth our secondary focus. Though we are projecting a lower rate of growth in 2016 than in years past, our guidance still implies over 40% annual growth in 2016."

The company is growing fast, with expected top-line growth of 40% in 2016 alone. With the business focused on showing real profits, it reveals two important things to investors: (1) The company can rein in spending and grow organically, and (2) investors can see profits on their invested capital. A company that grows revenue rapidly without generating free cash flow and returning capital to shareholders is likely to end very badly for all stakeholders (that is, the company, customers, and investors).

If management can execute on its goal of becoming cash flow-positive in the next few quarters, it should send the "all-clear" sign to Wall Street and investors that the company is back on track. The company is growing impressively on the top line. It won't be the end of the world to slow things down and show that the company can generate real profitability. It's better for all stakeholders in the long term.

What it means for SolarCity in the long termIt's important to remember that SolarCity is one of the dominant players in the solar industry and continues to grow at an impressive rate. The company controls 35% of U.S. residential solar, 28% of U.S. distributed solar, and 12% of total U.S. solar capacity installed in 2015. Many early growth stage companies have these hiccups.

It will take time for SolarCity to fully regain investors' trust. However, I do expect the solar leader to bounce back from this unfortunate downdraft in share prices. With the stock now marked down over 60% from the all-time high set last year, this could be a good time for long-term investors to buy shares.

As the U.S. population continues to grow and distributed solar energy gains traction, solar installation should continue to grow. Regardless of slower-than-expected commercial installation, SolarCity is strategically positioned to benefit from these long-term tailwinds.

The article SolarCity: Show Me the Money originally appeared on Fool.com.

Luke Neely owns shares of Amazon.com. The Motley Fool owns shares of and recommends Amazon.com and SolarCity. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.