Social Security: 1 Terrible Reason to File for Benefits at 67

Image source: Getty Images.

Starting with those born in 1960 and later, the full retirement age (FRA) for Social Security benefits will be 67. Waiting until your FRA to claim certainly has its benefits.

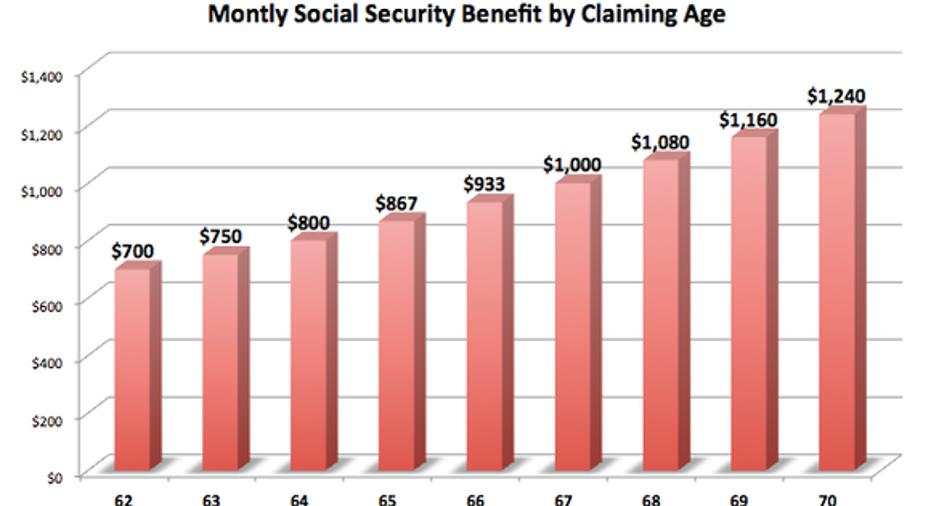

For example, let's assume you earned you the right to a $1,000 monthly Social Security benefit at FRA.Depending on when you file for benefits, the size can fluctuate a great deal. Assuming you are in the cohort born on or after 1960, here's what those fluctuations look like.

Data source: Social Security Administration

On the surface, it might seem like a no-brainer to wait as long as possible to secure the highest payout you can get. But while we can sit here and crunch the numbers all day, I believe that there's a huge disconnect between what makes sense on paper and how things play out in real life.

If you're waiting until 67 to claim Social Security benefits just to secure more money -- especially if your basic needs will be met if you file earlier -- I think it's highly probable that you're making a short-sighted decision.

Two kinds of abundance

In life, there are two important types of abundance: an abundance of wealth and an abundance of time. Culturally, we are encouraged to spend much of our energy securing the former, while giving the latter very little thought, especially during prime working years.

But if we look at the research behind what actually makes people happy -- or simply investigate our own lives for evidence -- we would quickly come to the conclusion that money contributes to happiness only insomuch as it secures our most basic needs: food, clothing, shelter, etc.

After that, however, it is through intentional activities -- like devoting ourselves to meaningful goals, taking care of our bodies and souls, practicing healthy behaviors, and nurturing relationships -- that happiness comes.The key is this: All of these "intentional activities" take time.

Here's how Cal-Riverside professor and researcher Sonja Lyubomirsky has visualized it, according to her research presented in her book The How of Happiness.

Data source: The How of Happiness, Sonja Lyubomirksy.

While it's possible to both earn money and devote yourself to something meaningful at the same time, that's simply not the case for everyone. The only way to guarantee you'll have the time for this is to clear your schedule -- retire and file for Social Security benefits.

It makes sense, but it's still hard...

Here at The Motley Fool, we talk a lot about not panic-selling during a market meltdown. When stocks stay the same or generally move up, everyone believes that they can easily "be greedy when others are fearful."

But once you see your account lose $10,000 -- or $100,000 -- in a few trading days, reality hits. You can't focus on anything else; you're constantly checking your portfolio for signs of a recovery. It gets so bad that the only way that many find to relieve the emotional stress is to hit the "sell" button. We simply aren't equipped to ignore the moves without proper preparation.

In much the same way, I'm sure many of you will look at the reasoning behind this research, and think, "that makes a lot of sense." But when push comes to shove, it's hard to pass up guaranteed increases in income. Those annual bumps are hard, quantifiable numbers that you can rely on. Your emotional state isn't nearly as easy to measure or count on.

But that's where relying on the research comes in. We know that we can hedonically adapt to both a higher and lower level of consumption. It makes far more sense to adapt down -- say, by cutting back on spending by 10% now to retire ASAP -- and focus on time affluence to provide your with satisfaction. Otherwise, if you wait until 67 to file for benefits, you'll be adapting "up" and are likely to either (1) count on more "stuff" to provide contentment -- which is a losing battle -- or (2) realize that you could've called it quits and started the next phase of your life much sooner.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies..

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.