Smith & Wesson Holding Corp in 5 Charts

Smith & Wesson Holding Corp. (NASDAQ: SWHC) will soon rebrand itself as American Outdoor Brands, a name change that reflects the gunsmith's shift in focus to the broader and much larger rugged outdoors market. Smith & Wesson remains the No. 1 firearms brand in the U.S., and its outdoors and accessories business currently is just a very small component of its operations, but the following five charts can help investors understand why the gunslinger is branching out.

Guns are as popular as they've ever been, which is why Smith & Wesson Holding sees this as a perfect time to downplay the business. Image source: M&R Glasgow, via Flickr.

Armed to the teeth

There have been few times in recent memory when firearms ownership has been so popular. The percentage of U.S. households with a gun in them has remained fairly constant since the 1990s at around 45% while the actual number of households has risen from 99 million in 1995 to over 124 million in 2015. This means the number of households with guns in them would have grown from 44 million to 55 million today.

The number of people buying guns is growing by leaps and bounds too. The FBI reports the number of gun-buyer investigations it's conducted has grown over the past 20 years from around 10 million to almost 25 million today. The National Shooting Sports Foundation, however, adjusts those numbers to reflect agencies investigating individuals for concealed-carry applications, as well as those that actively check all their concealed-carry permit holder databases. While that reduces the numbers and more closely reflects actual sales, it still shows a steady rise in gun sales:

NICS is National Instant Criminal Background Check System.Image source: Smith & Wesson Holding.

Two smoking barrels

That has translated into very good numbers these past few years for Smith & Wesson, which has posted significantly higher gun sales and profits. Over the past decade, firearms sales have soared, growing from $221 million in 2007 to $387 million in just the first six months of its current fiscal year. Full-year revenues from all sources are expected to grow 29% to $930 million:

Image source: Smith & Wesson Holding.

That's also translated into substantially higher profits. Net income was $8.7 million in 2006, but clocked in at $94 million in fiscal 2016. And just since 2013, it expects per-share profits will have doubled to $2.47:

Image source: Smith & Wesson Holding.

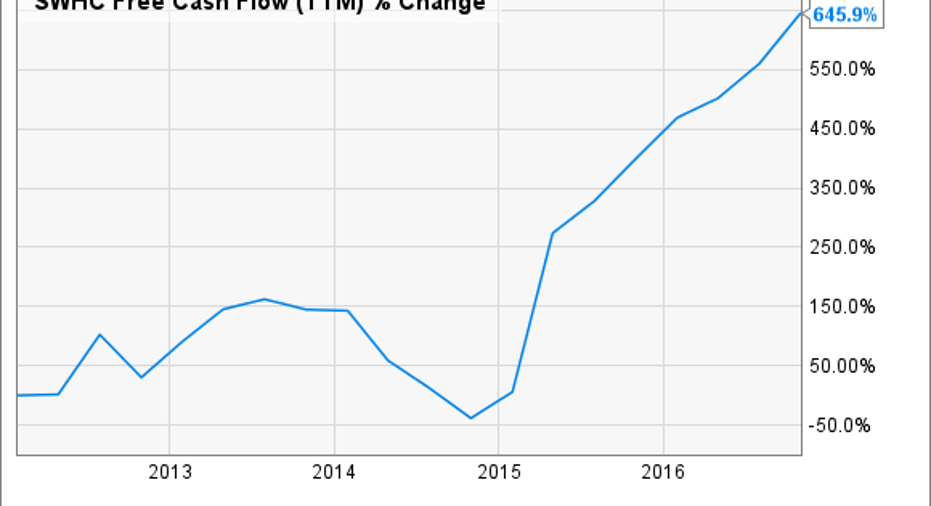

Cash-printing machine

Smith & Wesson has been able to consistently produce substantial amounts of free cash flow over the years, coming in at $168 million in 2016, some 86% higher than just two years prior. Although its capital expenditures may rise and fall over time, the gunslinger's free cash flow, the cash left over after paying for investments in the business, has risen consistently as well:

SWHC Free Cash Flow (TTM) data by YCharts.

Loaded for bear (markets)

All of this sounds like a case for Smith & Wesson to, well, stick to its guns and continue pursuing a firearms-centric business. The gunmaker still plans to be the premier American firearms company -- and will continue to market and sell its guns under the Smith & Wesson brand. However, gun sales can run hot and cold and though the industry may be less subject to panic buying today than it has been in the past, that also means sales will likely normalize, diminishing the torrid rate of growth the company has seen recently. The following chart shows some of the newly acquired brands to help diversify the business away from firearms.

Image source: Smith & Wesson Holding.

At an estimated $60 billion, the rugged outdoors market Smith & Wesson is buying its way into is four times larger than the firearms market, and subject to much less volatility. Boom times such as Smith & Wesson is currently experiencing is certainly enjoyable, but the bust that inevitably follows is not.

A diversification into a separate (though supportive) industry will smooth out those hills and valleys, and make the company's revenue streams more reliable. There are undoubtedly risks inherent in the plan, but it's understandable and commendable that Smith & Wesson has such a long-term outlook.

10 stocks we like better than Smith and Wesson Holding When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Smith and Wesson Holding wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of Nov. 7, 2016

Rich Duprey has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.