Shares of These Two Independent Refiners Got Hit Hard in January

What happened?

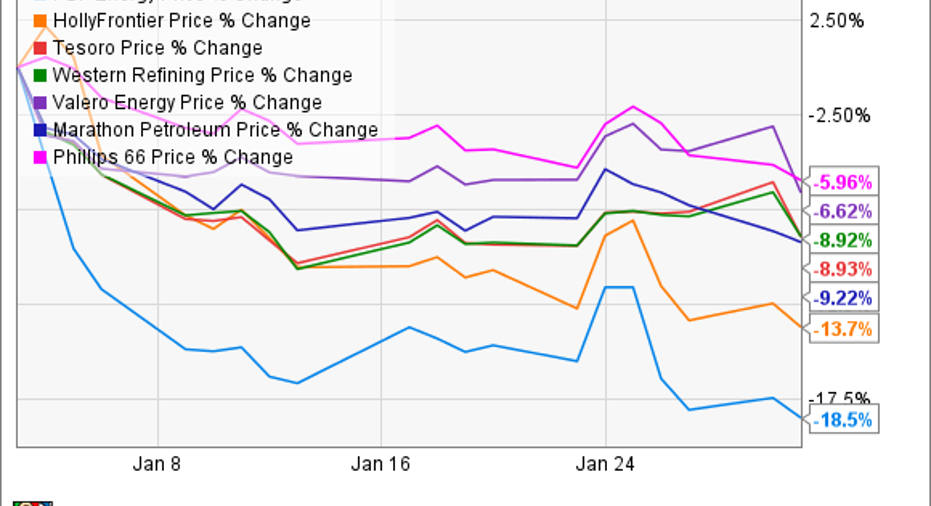

While the refining industry continues to struggle in a down part of the market as a whole, two companies in particular were hit hard in January: PBF Energy (NYSE: PBF) and HollyFrontier (NYSE: HFC). Shares of PBF and HollyFrontier were down 18.5% and 13.7%, respectively in January.

For PBF, the big move downward was mostly related to a stock downgrade. For HollyFrontier, though, it's a bit more of a head-scratcher as the company's stock was actually upgraded last month.

Image source: Getty Images.

So what?

One thing to remember is that all U.S. independent refiners are in a bit of a funk lately. According to a recent report from McKinsey, the crack spread in 2016 for U.S. Gulf Coast refiners declined $5.70 per barrel from the prior year to around $3.00 per barrel. PBF has limited exposure to the U.S. Gulf Coast and HollyFrontier has no presence there, but this is just more of an indication of the tough times refiners are facing lately.

There are a couple factors playing into this trend for crack spreads and refining margins. One is rising crude prices, which increase feed-stock costs. At the same time, though, refineries in the U.S. have been running at high rates for several quarters in a row with little turnaround or maintenance work. That translates to a large supply of refined petroleum products and has kept product prices from rising with the price of crude.

Another big factor that has been an issue for refiners as of late has been the costs to comply to the U.S. EPA's renewable fuels standard. Since PBF and HollyFrontier don't have their own ethanol production or ethanol blending assets, they have to buy ethanol credits on an exchange market known as RINs. This market has been rife with speculation and fraud, and as a result the costs for these RINs have put a major dent in refiners. This particular issue has hit independent refiners much harder than the integrated companies as of late.

Take, for example, Valero Energy (NYSE: VLO). The company is one of the nations largest ethanol producers and oil refiners, but even with significant ethanol credits in house, the company still had to pay about $750 million in RIN purchases and compliance costs. Considering how low margin the refining business already is, you can see why so many independent refiners had such a rough January.

The combination of these two factors is likely to explain why PBF's shares were downgraded back in January, but it does make you wonder why HollyFrontier's stock was upgraded. Well, one big separating factor as of late is HollyFrontier's recent acquisition of Suncor Energy's Petro-Canada lubricant facility in Ontario.

Not only are lubricant facilities typically a higher margin business than fuels refining, but the price at which HollyFrontier bought this asset should ensure pretty high rates of return. It also helps that lubricant and petrochemical manufacturing doesn't fall under the same EPA regulations. While we can't say with complete certainty that this is why HollyFrontier is being viewed a little more positively than PBF Energy right now, you have to imagine that it played a part.

Now what?

The refining business is expected to undergo a lot of changes with the new administration in office. Throughout the campaign, now president Trump constantly talked about the need to de-regulate. Also, Trump's special advisor for regulatory reform just happens to be the majority shareholder in an oil refining company. So if there are going to be some peeling back of regulations, things like the EPAs Renewable Fuels Standard is likely at the top of the list.

That, plus potential tax reform, would go a long way in improving the results of these companies. As long term investors, though, we cannot make decisions on the possibility that these things will happen. Until the ink is actually dry on any reform or change in tax law, these things shouldn't be a part of your thesis.

With so much up in the air with these companies, it is likely best to sit this one out for a bit. Sure, HollyFrontier has completed its acquisition, but a quarter or two of financial results will give us a better idea if this is a stock worth buying or not.

10 stocks we like better than HollyFrontierWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and HollyFrontier wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Tyler Crowe has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.