Safe Stocks Yielding 5% (or More) Do Exist -- Here Are 5 of Them

Image by Markgraf-Ave via Pixabay.

With interest rates still hovering near multi-decade lows, many investors who need to generate income from their investments have been forced to put money to work in the stock market. However, with the S&P 500 currently offering up a paltry dividend yield of roughly 2%, investors looking for a higher cash return have been often been forced to invest in riskier stocks.

In an effort to help those investors out, we reached out to our team of Motley Fool contributors and asked them toshare a safe stock that also offers investors a high dividend yield. Read on to see if their stock suggestions can help.

Given the recent downturn in the oil and gas markets, the energy sector is most certainly a fertile hunting ground for high-yielding stocks. While the sector is generally a high-risk place to be right now, I would argue that if you stick with the strongest players in the industry, your capital is likely to be quite safe.

One high-yielding stock in the space that I like and own is Spectra Energy , which currently yields north of 5%. Spectra Energy isone of the largest natural gas pipeline operators in North America, so unlike many other energy companies, Spectra makes its money by moving natural gas from one place to another, not from the price of the commodity itself. This means the price of the gas itself doesn't have much of an effect on the company's financials, as 99% of the company's profits are based on fees alone. As long as Americans need to consume natural gas, there will be a demand for Spectra Energy's pipelines, which helps ensure that the company's profits will continue to flow even when the energy markets go crazy.

Aside from being an income story, there's also reason to believe that Spectra Energy can continue to grow from here. The company currently boasts a project pipeline worth more than $35 billion, nearly twice the company's current $8 billion market capitalization. As those projects come online, its revenue and profit should continue to grow, and the company has already made plans to pass those profits back to its investors in the form of a rising dividend. The company has committed to increase its dividend by $0.14 per year between now and 2017, which represents a solid 9% growth rate and is mighty fast for a company that currently yields 5.55%. Given the high yield and fast growth, I think the odds are quite good that buying Spectra Energy's stock today will provide investors with a solid income stream alongside capital appreciation.

Matt Frankel:Plenty of safe, high dividends abound in REITs. By nature, REITs legally must pay out at least 90% of their income to shareholders,andthey aren't taxed at a corporate level. As a result, it's fairly common to see REITs pay 5% or more with a high level of safety.

One strong example isIron Mountain. It specializes in facilities to securely store documents and records, which it does for more than 150,000 businesses. Storage facilities are a unique type of property -- they have relatively low maintenance and turnover costs, and the tenant retention rate is high.

Iron Mountain has already produced 26 consecutive years of revenue growth, and it recently laid out its vision for 2020 in a presentation. Over the next five years, the company plans to increase its presence in emerging markets, increase its return on invested capital to 14%, grow revenue by more than 20%, and lower its leverage ratio.

Already a generous dividend payer with a 6.75% yield, Iron Mountain anticipates increasing its dividend to $2.18 per share by 2018, a 14% increase from 2015's payout. And, if the company's acquisition of competitor Recall closes in early 2016 as anticipated, the increased revenue and synergies that come with it could boost the 2020 numbers even further.

Adam Galas: High-yield income investors searching for a generous, safe, and growing yield should take a look atBrookfield Renewable Energy Partners because the distribution profile is among the best I've seen among dividend stocks.

The forward yield is 6.6%, compared with the S&P 500's2%, yet it's safeguarded by a distribution coverage ratio of 1.1, meaning the payout is well supported by its cashflow. Better yet, 92% of that cash flow, derived from 7.3 gigawatt of hydro and wind generation capacity on four continents, is ensured by inflation-adjusted contracts with an average remaining length of 17years.

So the payout is both large and secure, but the final piece of any distribution profile is long-term growth potential, and here, too, Brookfield Renewable Energy Partners shines. Management is guiding for long-term annual distribution growth of around 7%, which it believes will result in total investor returns of 12%-15%CAGR.

Those expectations are well supported by historical market data, which shows that a good rule of thumb for predicting total returns is yield plus long-term dividendgrowth.

How is Brookfield Renewable Energy Partners planning on delivering on its growth promise? Well, for starters, it continues to grow its asset base of renewable power projects around the world. With an estimated annual 120 gigawatt of hydro, solar, and wind projects expected to come online through 2020, the potential growth runway for this strategy is trulyenormous.

Brookfield Renewable Energy has 4.4 gigawatt of additional capacity it's either working on now or evaluating for purchase or investment. This would represent a 60% increase in generating capacity and drive strong growth in FFO per unit, which is what pays the quarterlydistribution.

Management expects the current growth pipeline to increase annual adjusted funds from operation 56% by2020. Assuming the current 7% CAGR payout growth rate, this would mean that any money invested today could be earning a 9.2%yield on cost in 2020 yet still be protected by a highly sustainable distribution coverageratioof 1.23.

Jason Hall: The oil and gas industry is probably the last place one would expect to find a "safe" dividend stock, but midstream behemoth Kinder Morgan Inc. meets that description.

Kinder Morgan is one of the largest energy companies in the U.S., only smaller than behemoths ExxonMobil and Chevron by market capitalization:

XOM Market Cap data by YCharts

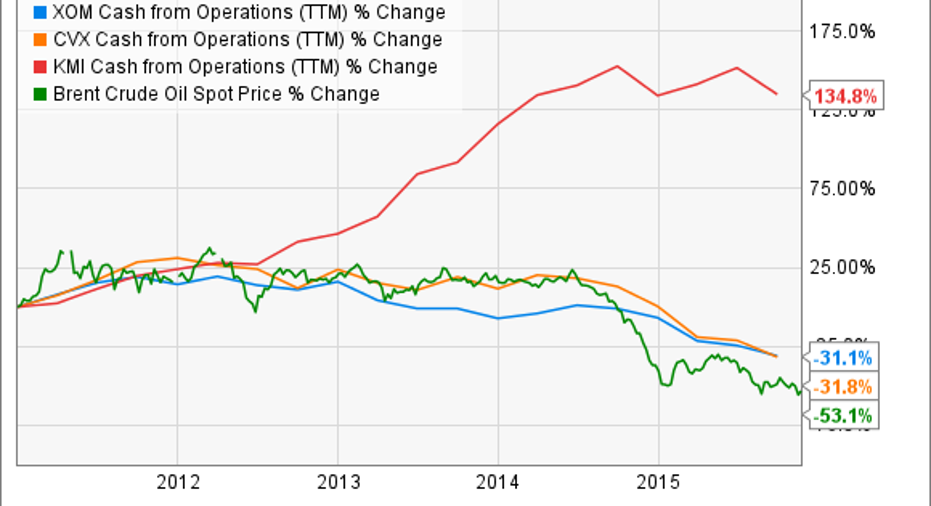

The difference is ExxonMobil and Chevron's oil and gas drilling operations are heavily affected by oil and gas prices, while Kinder Morgan makes a living operating the infrastructure that connects oil and gas production to processing, refining, manufacturing, and consumers.

This means the vast majority of Kinder Morgan's revenues (and profits) are from fee-based services, not how much oil or natural gas is selling for. That's meant steady and growing operating cash flows from Kinder Morgan, while its integrated peers have been squeezed in the decline:

XOM Cash from Operations (TTM) data by YCharts

But "safe" isn't the same thing as "risk-free," and Kinder Morgan's stock is down over the past year. But that's partly a reaction to a merger of the company's related assets, and to fears of a prolonged oil price decline that won't really hurt Kinder Morgan.

Long story short: There is always short-term risk with stock prices, but over the long term, Kinder Morgan's massive infrastructure "toll road" will continue generating consistent revenues and cash flows, supporting a dividend that's yielding 8% at recent prices. Even slow organic revenue growth and expansion would be icing on top of that yield.

Jordan Wathen: The words "high yield" and "safe" rarely appear in the same sentence, but I tend to thinkGolub Capital BDC's 7.5% dividend yield is one of the best in its industry.

Golub makes its money by lending to companies and private equity firms to buy out other companies. It's the largest player in the middle market, enabling it to see more deal flow and be pickier when it comes to deciding which deals it should finance and which deals it should simply walk away from. As a debt specialist, Golub Capital's clients know that they can work with the firm in confidence. Golub doesn't want to compete for buyouts; it wants to lend to the people who do.

Its focus on lower-risk credits could provide additional opportunity for upside. As its peers post steeper loan losses and need to raise capital, stronger companies like Golub may get the opportunity to pick up assets at distressed prices. This is why I think Golub Capital BDC is a high-yielding stock you can own through thick and thin.

The article Safe Stocks Yielding 5% (or More) Do Exist -- Here Are 5 of Them originally appeared on Fool.com.

Adam Galas has no position in any stocks mentioned. Brian Feroldi owns shares of Kinder Morgan and Spectra Energy. Brian Feroldi has the following options: long January 2016 $32.5 calls on Kinder Morgan, short January 2016 $32.5 puts on Kinder Morgan, long January 2016 $40 calls on Kinder Morgan, short January 2016 $40 puts on Kinder Morgan, long January 2017 $35 calls on Kinder Morgan, and short January 2017 $35 puts on Kinder Morgan. Jason Hall owns shares of Kinder Morgan. Jordan Wathen has no position in any stocks mentioned. Matthew Frankel has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Kinder Morgan and Spectra Energy. The Motley Fool owns shares of ExxonMobil. The Motley Fool recommends Chevron. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.