Rumors Swirl Around Biogen Today

Image source: Stockmonkeys.com via Flickr.

Fresh on the heels of reporting success in a late-stage study of a drug for spinal muscular atrophy, or SMA, Biogen Inc. (NASDAQ: BIIB) shares rocketed higher this afternoon amid merger rumors. While no specific companies have said publicly that they're trying to acquire Biogen, The Wall Street Journal reports that both Allergan plc(NYSE: AGN) and Merck & Co (NYSE: MRK) are kicking the company's tires. Could a mega-deal be in the works?

First, some background

Biogen is the market-share-leading manufacturer of treatments used to to control symptoms in multiple sclerosis patients. MS is a central nervous system disease that's caused by damage to the myelin sheath surrounding nerve fibers. As that damage progresses, symptoms of MS, such as fatigue and pain, worsen.

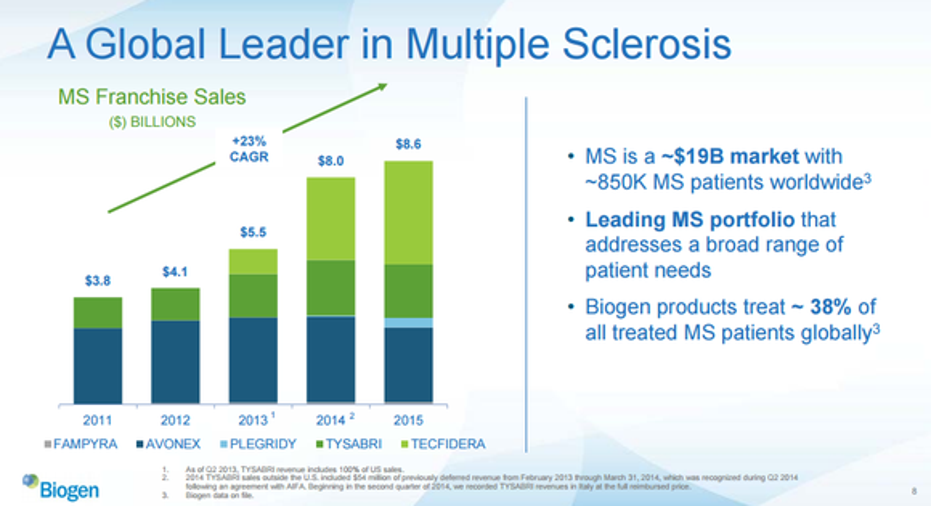

The market for MS therapies is valued at about $19 billion per year, and Biogen controls about 38% market share across a slate of top-selling medications. The company's best sellers include oral MS drug Tecfidera and injection-based drugs Avonex, Plegridy, and Tysabri. All four of those drugs are billion-dollar blockbuster medications.

Image source: Biogen Inc.

Recently, Biogen reported second-quarter results and announced that longtime CEO George Scangos will step down. Sales in the quarter grew 12% to $2.9 billion versus last year, and cost-cutting allowed earnings per share, or EPS, to increase 23% to $5.21.

The company's solid second-quarter results come in the wake of a disappointing failure of a next-generation MS drug under development. The drug, anti-lingo, was being evaluated as the first MS therapy able to target MS symptoms by repairing damage to the myelin sheath. Unfortunately, the drug was surprisingly ineffective in trials, casting significant doubt on its future.

Scangos' decision to leave Biogen may or may not have been influenced by the high-profile stumble of anti-lingo, but even if it was, it's still hard to deny the success Scangos has enjoyed during his tenure. Since taking over the helm in 2010, Biogen's sales and profit have grown leaps and bounds.

In light of the emerging rumors of an acquisition, Scangos' decision to leave is even more intriguing. Scangos detailed plans earlier this year to spin off two fast-growing hemophilia drugs as a separate business to unlock shareholder value. Those two drugs, Eloctate and Alprolix, generated a combined $205 million in sales last quarter, up from $128 million in the same quarter a year ago. Scangos' plans to spin off the hemophilia franchise, though, were recently pushed back to early 2017.

Perhaps Scangos' decision to leave is the result of interest in the board to unlock more value by selling the entire company, rather than selling off specific drugs. Pushing out the spinoff of the hemophilia drugs may add conviction to that thinking, because doing so gives potential acquirers of Biogen additional time to consider what they'd like to do with the drugs.

Sizing up suitors

With a market cap of nearly $70 billion, Biogen is an industry Goliath, and that means only the deepest-pocketed of its competitors might be in a position to buy the company outright.

Merck & Co. is clearly big enough to digest such a transaction, but it's more intriguing to me that Allergan could be in the hunt.

Previously, Allergan had planned to merge with Pfizer Inc. in the biggest M&A deal in healthcare history, but that deal was sidelined earlier this year when the Treasury Department closed tax inversion loopholes that made the merger less appealing to Pfizer.

The dismantling of the merger left Allergan investors wondering how Allergan would overcome a mountain of debt accumulated from past acquisitions, and what steps management would take to grow sales in the future.

The FTC recently answered the first question when it cleared the sale of Allergan's generics business to Teva Pharmaceutical for$33.4 billionin cash and 100.3 million shares of Teva stock worth$5.4 billion. Allergan announced it closed on that deal today, and thus the cash infusion seemingly gives it room to consider an acquisition of this size.

Over at Merck & Co, sales have stagnated because of patent expiration, and that's likely got management searching eagerly for ways to kick-start growth. In the second quarter, Merck & Co.'s sales inched up by only 0.5% to $9.8 billion.

Merck & Co's sales slowdown is tied in part to a drop-off in demand for Remicade, an autoimmune disease drug with $339 million in Q2 sales. The launch of a Remicade biosimilar that works similarly, but that's not an identical copy of Remicade, caused Merck & Co.'s Remicade revenue to slip 26% versus a year ago.

Since Remicade is creating a big headwind Merck & Co. would like to overcome, it wouldn't be too surprising to learn that it's putting its$1.2 billion in quarterly net income and $26 billion in cash and investments to work with a deal.

Weighing its options

Biogen's board hasn't yet responded to the rumors, and investors should never buy a stock because of M&A chatter. Still, there's plenty of reason to own Biogen stock on its own.Biogen expects to deliver non-GAAP EPS of at least $19.70 per share this year, and industry watchers think EPS could reach $20.95 next year. At current prices, that means investors can buy this stock for less than 16 times forward earnings. That may not be as cheap as some other large-cap biotechs, but it's not an unreasonable price to pay for a growing company like this.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early, in-the-know investors! To be one of them, just click here.

Todd Campbell has no position in any stocks mentioned.Todd owns E.B. Capital Markets, LLC. E.B. Capital's clients may have positions in the companies mentioned. Like this article? Follow him onTwitter, where he goes by the handle@ebcapital, to see more articles like this.The Motley Fool owns shares of and recommends Biogen. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.