Roper Technologies, Inc.: Management Delivers in a Tough Year

It's been a tricky year operationally for Roper Technologies, Inc. (NYSE: ROP). A combination of weaker-than-expected oil and gas capital spending trends, weakening industrial production growth, and delays in a toll road project in Saudi Arabia have reduced earnings expectations. There is little management can do about these issues, but where it can make a difference, it has executed well. The latest third-quarter results revealed some pretty strong margin performance and cash flow generation alongside an interesting acquisition. Let's take a closer look at an eventful quarter.

Roper Technologies, Inc. Q3 earnings: The raw numbers

A look at the headline numbers from the third quarter:

- Revenue growth of 7% in the quarter is in line with management's previous forecast for 7% to 9% growth in the second half.

- Organic revenue growth of 2% is also in line with previous forecast for 2% to 4% growth in the second half.

- Adjusted diluted EPS of $1.65 beat management's forecast range of $1.59 to $1.63.

Following the negative surprises in the second quarter (toll road project delays and oil and gas deterioration), it was good to see performance largely on track.However, the fourth-quarter and full-year guidance contains a larger than usual range. In addition, earnings expectations have been lowered for the full year:

- Fourth-quarter adjusted diluted EPS forecast in the range of $1.77 to $1.89.

- Full-year adjusted diluted EPS forecast in the range of $6.48 to $6.60, compared to previous guidance of $6.57 to $6.71.

- Free cash flow conversion expected to be around 140% of net income.

- Full-year revenue and earnings before interest, tax, depreciation, and amortization (EBITDA) expected to grow in the 5% to 6% range.

There are two reasons for the broad range in diluted EPS.First, the timing of the ramp-up on the project to convert nine bridges and tunnels to all-electronic tolling for the New York Metropolitan Transportation Authority -- management expects to finish three by January and then the rest in its fiscal 2017.Second, the industrial technology and energy systems and controls segments are typically stronger in the fourth quarter, but given the weakness in both segments in 2016, management isn't expecting any uplift this year -- hence the guidance cut.

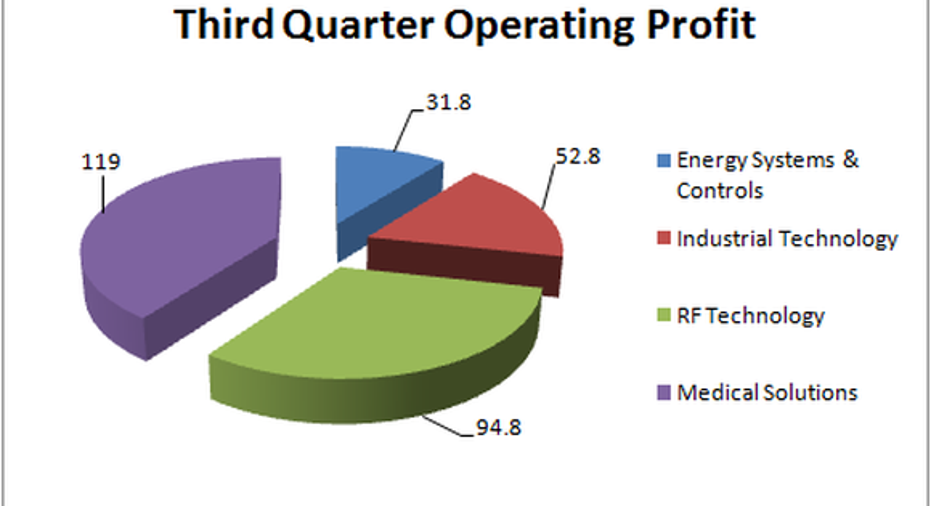

Data source: Roper Technologies. Figures in millions of dollars. Chart by author.

Analysis of Q3 earnings

There are three key points of note regarding the results.

First, as you can see below, the two most important segments (RF technology and software and medical and scientific imaging) are growing organic revenue in the kind of mid-single-digit range management expected them to at the start of the year. Moreover, management is doing a pretty good job of holding margin up in the weakest segments (industrial technology and energy systems and controls).

For example, CEO Brian Jellison pointed out on the earnings call that "the EBITDA margin in '14 was 32% of those combined businesses and here this year it's 31%. So despite a significant fall-off in revenue, the margins have been able to be maintained."

Data source: Roper Technologies. 100 basis points = 1%.

Acquisitions to the rescue

Second, Roper has long been a company known for growing via acquisition. Essentially, management aims to buy high-margin, asset-light businesses operating in niche markets and with highly cash-generative properties. As you can see in the table above (note the difference between reported revenue growth and organic revenue growth), acquisitions played a key role in the third quarter.

In addition, management announced the intent to acquire ConstructConnect, a provider of data, collaboration,and workflow solutions to the commercial construction industry, for $632 million. Management expects it to contribute $150 million in revenue in 2017, and $50 million in EBITDA. Based on these figures, ConstructConnect has an EBITDA margin of 33% (Roper's was around 34.6% in the third quarter) and management expects margin to expand over time.

Image source: Getty Images.

Margin and cash flow

Third, on the earnings call management highlighted good execution with regard to margin and cash flow. For example, EBITA margin has expanded from 32.5% in the third quarter of 2014 to 33.7% in this year's third quarter.Meanwhile, year-to-date free cash flow is up 11% to $731 million compared to the same period last year, significantly helped by a reduction in working capital as a percentage of sales to 1.9% from 4.2% and 5.8% in the previous years' third quarters.

Looking ahead

Investors will be hoping for the normal seasonal pickup in the industrial- and energy-focused segments -- if so, there could be upside to earnings expectations -- while hoping the New York tolling project proceeds as planned. In addition, there is the ConstructConnect acquisition to look forward to. A difficult year, but management is doing what it can to extract value for investors.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early-in-the-know investors! To be one of them, just click here.

Lee Samaha has no position in any stocks mentioned. The Motley Fool recommends Roper Technologies. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.