Risk Off: S&P, Nasdaq Erase Weekly Gains as Global Jitters Flare

Wall Street’s optimism quickly faded in the back half of the week as jitters over a looming U.K. vote, the June Federal Reserve meeting, and global growth concerns forced two of three major U.S. averages to erase weekly gains.

At the close of trade Friday, the Dow Jones Industrial Average dropped 119 points, or 0.67% to 17855. Meanwhile, the S&P 500 declined 19 points, or 0.92% to 2096, and the Nasdaq Composite shed 64 points, or 1.29% to 4894.

On a week-to-date basis, the Dow was the only one of the three averages in positive territory, gaining 0.33%. The S&P snapped a three-week win streak as it shed 0.14%, while the Nasdaq saw its first down week in four as it lost 0.97%.

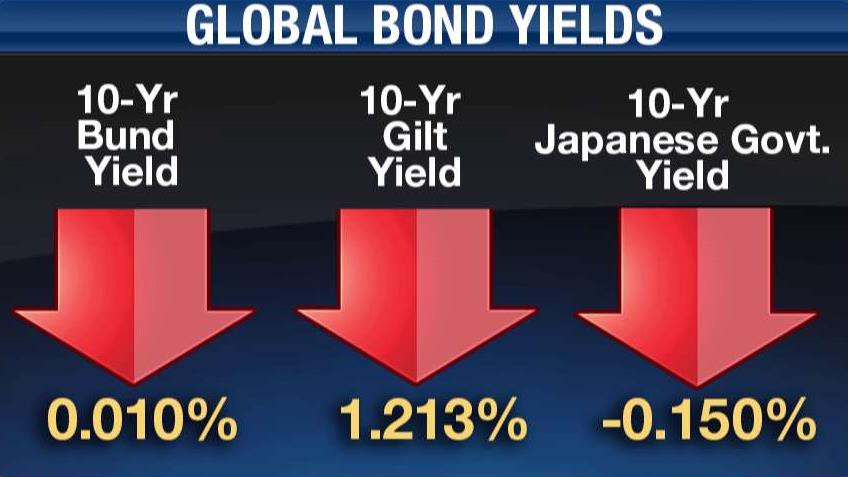

As investors fled equities, they bought up assets traditionally seen as safe havens including gold and government bonds. For the week, gold prices jumped 2.69% to $33.30 a troy ounce, while global bond yields, which move in the opposite direction of prices, plunged. The U.S. 10-year yield settled at its lowest level since May 2013, while the yield on the 10-year German Bund sank to a record low of 0.01% and the Japanese 10-year yield pushed further into negative territory.

Last week, data showed $2.6 billion in outflows from global equity markets, while the bond market saw $7.9 billion in inflows and $2.6 billion into high-yield, a more risky part of the bond market.

As a result, the financial sector fared the worst through the week, posting declines of 1.5%, followed by the consumer discretionary and health care sectors, which dropped 1.08% and 0.57% respectively. The week’s sector gainers were led by telecom, energy, and consumer staples.

The move to riskier assets is a concern for global central banks struggling to find ways to prevent their economies from falling into recession as they move interest rates into negative territory.

“[Those policies] drive consumer behavior into riskier assets that may or may not be appropriate for them,†Jennifer Vail, U.S. Bank Wealth Management head of fixed income, said. “That and bank earnings. If banks are struggling to charge for deposits, that’s going to hit bank earnings.â€

Combined with uncertainty about U.S. rate hikes and a slowing global-growth environment, what has investors spooked is a looming vote by British citizens over whether their nation should leave the European Union. That referendum comes in fewer than two weeks on June 23, and fresh polls indicate the favorability of leaving the EU is growing.

“There’s a real fear a Brexit vote would create volatility and it’s becoming a self-fulfilling prophecy,†Brad McMillan, chief investment officer for Commonwealth Financial Network said.

A poll commissioned by the Independent and released two hours before the market close in the U.S., showed of 2,000 people polled, 55% favored a so-called Brexit vote. But McMillan said in his view, the odds of that coming to fruition are low, and he sees market volatility easing by the end of the month.

“Does it make economic sense [for the U.K. to leave]? Personally, I think it doesn’t…this will be more of a Y2K event even if it happens,†he said. “Brexit is a risk factor holding the market down, and if that goes away, you’ll see a big headwind disappear.â€

What’s proved to be a tailwind of sorts for the market is the Fed’s two-day policy-setting meeting, which takes place next Tuesday and Wednesday. Wall Street has essentially priced out any chance of the central bank moving short-term interest rates higher at the conclusion of that meeting. Fed funds futures, a tool used to predict market expectations for changes in U.S. monetary policy, showed odds of a rate rise at just 2%. An unexpectedly weak May jobs report and subsequently weak consumer data helped push those odds down over the last six trading days.

Investors next week will be looking for signs of strength in the U.S. economy, which could give the central bank more leeway to raise rates in July. Highlighting the economic-data calendar are expected releases of May retail sales and consumer price inflation figures, as well as import and export prices, regional manufacturing surveys, and housing starts.

“The May retail sales report is the most important indicator, followed by the May CPI report…we expect payback for April’s outsized gain and would not be surprised by downward revisions,†economists at Deutsche Bank wrote in a note. “Retail control, which is the core of the report, is expected to be up slightly following the largest one-month gain in over two years.â€