Record Earnings for Home Depot Inc as Profitability Jumps

Image source: The Motley Fool.

Home Depot (NYSE: HD) posted earnings results this week that included double-digit profit gains powered by a steady rebound in the housing market. The retailer boosted its earnings outlook for the second straight quarter, too -- while affirming its full-year sales growth forecast.

Here's how the big-picture results stacked up against the prior year:

Source: Home Depot's financial filings.

What happened this quarter?

Sales growth chugged right along at the pace that management had expected despite a slowdown in customer traffic gains. Profits, meanwhile, surged higher as Home Depot again demonstrated the power of its big-box retailing model.

Highlights of the quarter included:

- Comparable-store sales rose 5%, marking a drop from the prior quarter's 7% spike. However, Home Depot continued to outpace nearly all national retailing peers -- including department stores and apparel specialists like Macy's and Nordstrom, which this week posted negative comps, implying Home Depot is faring better than most at defending against the threat of online competition.

- Comps gains were powered by a mix of customer traffic growth (+2.3%) and higher average spending (+2.4). Each of these figures decelerated for the second straight quarter, yet still drove HD's highest quarterly sales result on record.

- Gross profit margin held steady at 34% of sales.

- Operating expenses grew at a much slower pace than revenue, which translated into solidly higher operating margin.

- Net income improved by 9% to $2.4 billion, but share repurchases goosed that growth into a 14% gain in earnings per share.

- Return on invested capital rose to a stellar 29% over the past 12 months, compared to 25% in the preceding period.

What management had to say

Executives highlighted the fact that Home Depot set a new financial record over the past few months. "We had a solid quarter, achieving the highest quarterly sales and net earnings results in company history as housing continues to be a tailwind for our business," CEO Craig Menear said in a press release. "This was made possible by our hard working associates in their continued dedication to our customers."

Looking forward

Menear and his team left their full-year sales growth outlook unchanged and still expect comps to improve by 5% -- up from the 4% that they had projected at the start of the year. The profit target was hiked for the second straight quarter, though. Home Depot began the year seeing $6.15 per share before raising the forecast to $6.27 per share in Q1 and to $6.31 per share now.

Beyond that, the retailer still has plenty of room to boost sales as the company attacks market niches like maintenance and repair operations along with surging demand by professional contractors. Its e-commerce initiatives, like next-day delivery of bulk goods, should kick in solid sales growth too.

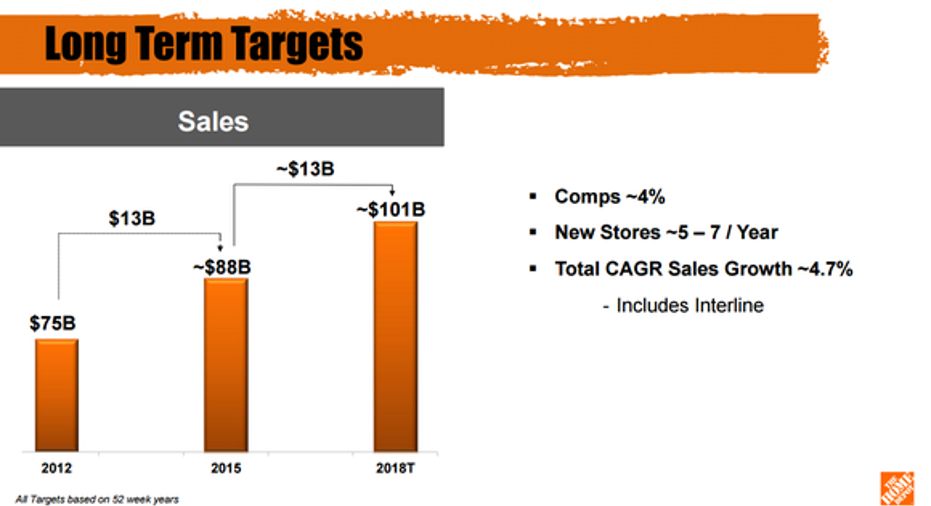

CAGR = compound annual growth rate. Image source: Home Depot investor presentation.

Home Depot has the wind at its back with industry growth, as well. Despite strong gains over the last five years, spending on home improvement is running well below the long-term average for the economy. Meanwhile, home prices haven't yet fully recovered from the market drop that began in 2007.

These trends give management confidence that they can achieve solid growth in revenue, earnings, and profitability at least into 2018 when executives see Home Depot passing the $100 billion annual sales mark.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Demitrios Kalogeropoulos owns shares of Home Depot. The Motley Fool recommends Home Depot and Nordstrom. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.