Phillips 66 Bought Back 14 Million Shares in 2016. Should Investors Be Happy?

Phillips 66 (NYSE: PSX) prides itself as a disciplined allocator of capital. For example, this year's capital budget is lower than it was in previous years because "fewer projects meet our return thresholds in the current business environment," according to CEO Greg Garland. That said, while the refining giant is cutting back on growth spending, one area where it doesn't have any intention of cutting back on is the rate that it repurchases shares. Here's a look at why investors should be thrilled with that decision.

How Phillips 66 allocates capital

Phillips 66 started last year with more than $3 billion of cash on the balance sheet. It would go on to generate $3 billion of operating cash flow and complete $2.3 billion of asset dropdown transactions with its aster limited partnership,Phillips 66 Partners (NYSE: PSXP), though the company received a combination of cash and units in those deals. Finally, the company tapped the debt markets, raising a net $1.3 billion after refinancing some legacy debt.

Image source: Getty Images.

Phillips 66 would go on to use every dollar that came in and then some, ending the year with $2.7 billion of cash on the balance sheet. The company spent the largest portion of those inflows on capex, investing $2.8 billion in capital projects, including more than $400 million in spending at Phillips 66 Partners. The company would also pay nearly $1.3 billion in dividends, which was up from $1.2 billion in 2015. Furthermore, the company spent more than $1 billion to buy back roughly 14 million shares, though that was down from $1.5 billion of repurchases in 2015.

Making an impact

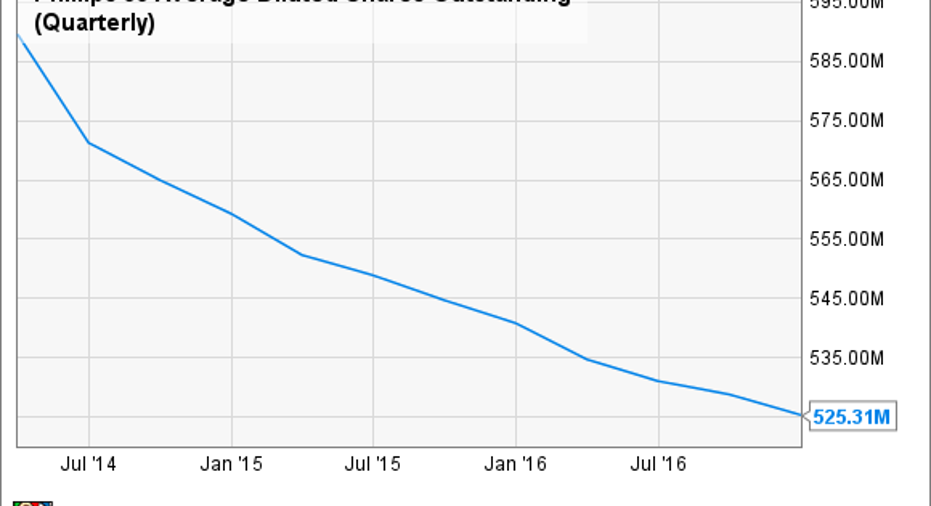

While the amount repurchased was down last year, it still had an impact, helping to continue the trend of meaningfully reducing the share count:

PSX Average Diluted Shares Outstanding (Quarterly) data by YCharts.

In fact, since gaining its independence in 2012, the company has reduced its share count by 16%. That has benefited investors in two ways. First, it is providing a little extra boost to the per-share results. For example, last quarter the company earned $0.31 per share as a result of having 526.3 million shares outstanding. However, if the company didn't buy back any shares last year, earnings would have been 3.2% less, or $0.30 per share. Another direct impact of the share repurchases is that the company needs less cash to meet its current dividend outlay. For example, after spending $329 million per quarter to pay dividend at the increased rate in the second and third quarters, the company only used $328 million in cash to pay the fourth-quarter dividend as a result of the share repurchases. That would make it a little easier for the company to increase the dividend in the future.

Keep on keeping on

Phillips 66 expects to continue allocating capital to reward its shareholders in 2017. On the company's fourth-quarter conference call, CEO Greg Garland stated that "in 2017, we expect to increase our dividend again and to spend $1 billion to $2 billion on share repurchases." Those share repurchases could be even more meaningful this year given that the company's stock price is down nearly 9% since the start of the year due to the current challenges in the refining industry.

For perspective, if the company spent the entire $2 billion on share repurchases today, it could reduce its share count by 25 million, which would decrease its total outstanding shares by nearly 5%. As a result, earnings per share would increase by a similar amount even if the underlying results didn't budge.

Investor takeaway

Unlike many share-repurchase programs that just offset dilution, Phillips 66's stock buybacks are having a meaningful impact on share count. That impact should continue in 2017 given the amount the company plans to spend on repurchases and the fact that its stock price has been under pressure due to some market challenges. Needless to say, this is a buyback that should make investors happy.

10 stocks we like better than Phillips 66When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Phillips 66 wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Matt DiLallo owns shares of Phillips 66. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.