PayPal's Revenue Growth Continues Unabated

Still image from video demonstrating the ease of use of PayPal subsidiary Xoom's remittance app. Image source: PayPal Holdings Inc.

If there's a single takeaway in the third-quarter 2016 earnings report from digital-payments facilitatorPayPal Holdings Inc. (NASDAQ: PYPL) that came out Oct. 20, it's that PayPal isn't having much trouble sustaining a revenue growth rate in the high teens. We'll delve in a moment into the metrics driving top-line growth, as well as management's expectations for the next three years. But first, let's take in the view from 30,000 feet.

PayPal: The raw numbers

| Metric | Q3 2016 Actual | Q3 2015 Actual | Growth (YOY) |

|---|---|---|---|

| Revenue | $2.67 billion | $2.26 billion | 18.1% |

| Net income attributable to PayPal | $323 million | $301 million | 7.3% |

| Diluted EPS | $0.27 | $0.25 | 8% |

Data source: PayPal Holdings Inc. 8K-filing, Oct. 20, 2016.

What happened with PayPal this quarter?

- The 18% revenue increase was characteristic of previous quarters of double-digit improvement, which PayPal has achieved regularly since going public in July 2015.

- Total payments volume (TPV), a measure of the total dollar volume of payments facilitated on PayPal's platform, rose 25% over the prior-year quarter, to $87 billion.

- Active customer accounts rose 11% to 192 million. The number of average transactions per active account increased 13%, to 30 transactions per account over a trailing-12-month period.

- Mobile payments volume surged 56% to $26 billion and accounted for nearly 30% of overall TPV.

- Customer interest in social payments app Venmo continued to blossom. The app, which, among other functions, allows friends to easily split restaurant checks, continued to post torrid growth. Venmo's TPV of $4.9 billion during the quarter translates to a year-over-year growth rate of 131%.

- Operating margin decreased 160 basis points to 13% in Q3 2016. PayPal's take rate (total revenue divided by total payments volume) has been declining in the past few quarters as Venmo's peer-to-peer transaction volume, which is not yet fully monetized, has increased. In addition, the company's Braintree subsidiary is enjoying higher volume, although its revenue is dependent on credit card transactions, which tend to be slightly less profitable than the company's overall transaction margin.

- Lower margins inject a dose of reality into an otherwise heady report. However, management tends to see this as a favorable trade-off in the interests of aggressively advancing the organization's top line.

- PayPal issued positive if minor adjustments to its full-year 2016 outlook. The company raised its expected revenue range by $30 million, to a new band of between $10.78 billion and $10.85 billion. Earnings-per-share guidance for 2016 was also lifted, from between $1.11 to $1.14 per diluted share to a new estimate of between $1.13 and $1.15 per diluted share.

- In its earnings release, PayPal declared its enthusiasm over numerous agreements signed during the quarter, most notably transaction partnerships inked with Visa (NYSE: V) and MasterCard (NYSE: MA). Yet on management's conference call with analysts, executives were careful to note that digital wallet partnerships with card issuers will take time to implement, and they signaled that the company wouldn't see a material revenue boost in 2017 from the Visa and MasterCard deals.

- PayPal announced that it will make its remittances app Xoom available to PayPal customers, thus opening the ability of PayPal users to send money to 10 new markets, as well accessing Xoom services in over 50 countries.

What management had to say

PayPal's management believes the transaction giant has several avenues to growth for the foreseeable future. This outlook is due both to the company's focus on expanding its customer base and the sheer size of the market it operates within. CEO Dan Schulman summed it up this way on the company's earnings conference call:

Source: Seeking Alpha conference call transcript dated Oct. 20, 2016.

Moving forward

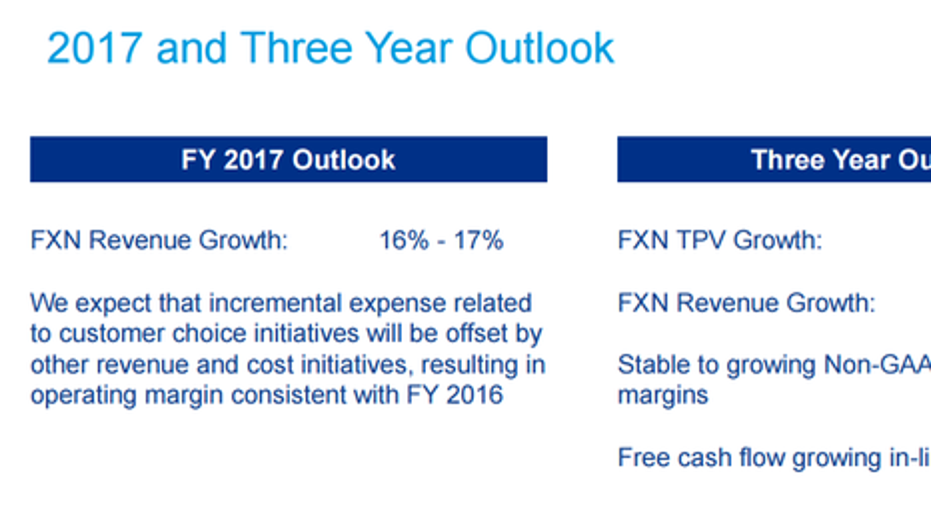

PayPal wants to communicate to shareholders that its impressive growth won't abate anytime soon. Alongside third-quarter earnings, management shared a three-year outlook (through 2019), outlining broad expectations. Note that "FXN" stands for currency-neutral -- that is, numbers presented before currency effects are factored in:

Image source: PayPal investor presentation, dated October 20, 2016.

This outlook essentially promises to keep current growth rates intact. PayPal also sees free cash flow expanding at a constant rate with revenue. The company has been generating exceptional cash flow as of late: In Q3, PayPal recorded $618 million in free cash flow, which equaled 23% of revenue.

In other words, PayPal converted nearly a quarter of every revenue dollar into cash after capital expenditures were paid for. With this kind of efficiency, the company should have ample funds to reinvest in the business, potentially sustaining its enviable growth rate beyond the next three years.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Asit Sharma has no position in any stocks mentioned. The Motley Fool owns shares of and recommends MasterCard, PayPal Holdings, and Visa. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.