Paycom Software Inc Has Room to Run

Paycom Software (NYSE: PAYC) targets C-suite executives and HR managers in the U.S. with its all-in-one human capital management (HCM) software solution, a convenient alternative to cobbling together products from multiple vendors. Instead of running one system to manage payroll and another to manage time entry and tracking, and still another to assist with tasks such as recruiting, training, and performance reviews, Paycom customers can log on to one integrated system -- running on a single cloud-based database -- that handles it all, including compliance with government regulations.

This lets companies focus on their own business instead of the ever-changing complexities of the tax code or various labor laws. With that as a backdrop, let's dive into why Paycom has the look of a long-term winner.

Image source: Paycom Software.

A profitable company with gangbusters growth

The total addressable market for the U.S. HCM industry will be $20 billion by 2021, according to Markets and Markets. With its $2.8 billion market cap, Paycom is a small fish in that big pond, with plenty of room to grow. And nearly any way you want to measure it, Paycom's current rate of growth is mighty impressive.

Over the last two full fiscal years (2014 and 2015), revenue, net income, and free cash flow have been on an absolute tear:

- Revenue grew from $107 million to $225 million -- a 45% compound annual growth rate.

- Net income grew from $0.6 million to $21 million. Starting from such a low number renders a CAGR calculation fairly meaningless (but for the record, it's 491%).

- After turning free-cash-flow-positive in 2013, the company more than tripled free cash flow from $8 million in 2014 to $26.5 million in 2015.

And the company's strong performance continued throughout 2016. In its most recent earnings report, for the third quarter, which was released Nov. 1:

- Third-quarter revenue was up 40% year-over-year to $77.3 million.

- Adjusted EBITDA was up 68% to $18.2 million.

- Management increased its full-year 2016 revenue guidance to a range of $326.5 million to $328.5 million, the midpoint of which represents 46% year-over-year growth.

- Full-year adjusted EBITDA guidance was also raised to a range of $88 million to $90 million, which represents 27% year-over-year growth at the midpoint.

- Management increased its long-term adjusted EBITDA margin target to a range of 30% to 33%, commenting that this will still allow the company to pursue robust growth while making substantial R&D investments.

Satisfying customers

The HCM industry is crowded. You're probably familiar with the larger competitors, including ADP, Paychex, Oracle, and SAP. But plenty of smaller, nimbler companies, such as Workday, have entered the field as well. With so many players offering overlapping solutions, price is of course a big factor. But it's not the only factor.

The idea of an all-in-one offering is especially attractive to the smaller-sized businesses that Paycom targets (generally, between 50 and 2,000 employees), since traditionally those businesses rely on multiple vendors to create their own patchwork solution, or attempt a portion of it themselves. With most of its competitors focused on the larger end of the market, Paycom also prides itself on providing superior service to companies that -- being on the smaller side -- wouldn't receive as much attention from industry giants.

So far, this approach is paying off big time. From 2011 to 2015, the company's number of clients -- currently 15,000 and counting -- increased at a 41% compound annual growth rate.

Paycom also claims it leads the industry in customer satisfaction, evidence of which can be seen in the company's fantastic retention rates. For the past three full fiscal years, the company's retention rate (percentage of revenue retained from existing clients) has held steady at 91%. Just as impressive: Recurring revenue for the third quarter increased 40% to $75.9 million, making up 98% of total revenues. With numbers like that, every new client the company signs increases not only the current quarter's sales numbers, but -- at least in theory -- all future quarters as well.

The biggest risk: Paycom's rich valuation

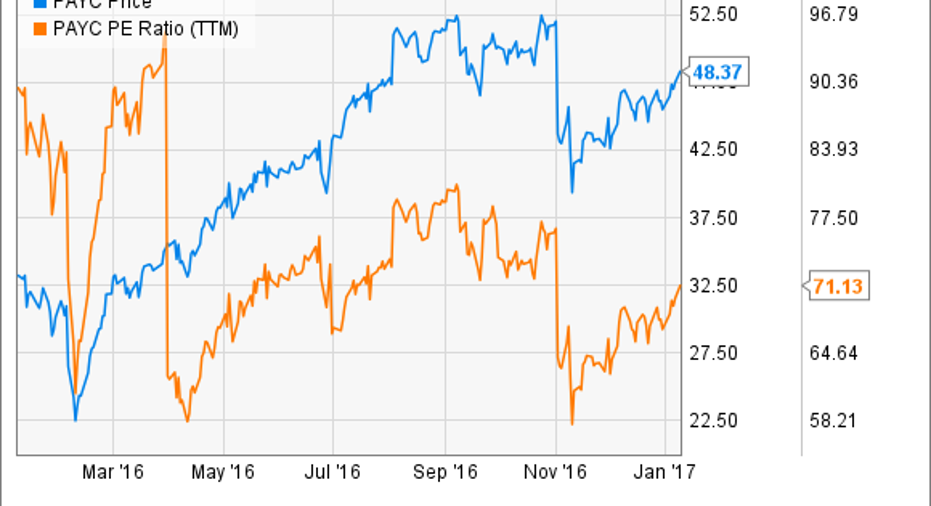

Make no mistake. Paycom's stock is expensive -- currently trading above a price-to-earnings ratio of 70 -- and is already pricing in many years of strong growth ahead. That's a little more palatable when you look toward the future, with the stock trading at around 46 times next year's earnings estimates. As long as Paycom maintains its torrid rate of growth, its valuation should come into a more reasonable range over the next couple of years. But at today's prices, even a whiff of disappointment can cause serious volatility.

In fact, last quarter, revenue and EPS both beat analyst estimates, but the stock dropped like a stone anyway. The best I can figure is that the company's previous two quarters featured incredible year-over-year growth rates of 63% and 51%, fueled largely by new billings from Affordable Care Act regulations. With that tailwind gone, perhaps third-quarter revenue growth of "only" 40% -- coupled with guidance for fourth-quarter revenue growth of 33% -- looked like a letdown by comparison.

One other potential overhang is the pending repeal of the ACA. The company has said that 5% of its revenue would be at risk if the ACA were to disappear overnight. But if the ACA is replaced by something else that also requires regulatory compliance, businesses would continue to require Paycom's services to navigate this transition, lessening the overall impact.

The stock has already run up more than 20% from its post-earnings low of $40 or so. Those looking to add a promising growth story to their portfolios may want to put Paycom on their watch list. Or, if you can stomach the inevitable large swings that come with the territory, even today's prices may turn out to be a decent entry point in the long run.

10 stocks we like better than Paycom Software When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now and Paycom Software wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Andy Gould owns shares of Paycom Software. Andy Gould has the following options: short February 2017 $40 puts on Paycom Software. The Motley Fool owns shares of and recommends Paycom Software and Workday. The Motley Fool owns shares of Oracle. The Motley Fool recommends Automatic Data Processing. The Motley Fool has a disclosure policy.