Newmont Mining Had a Great 2016. Will It Lose Its Luster in 2017?

With prices rising as much as 21% last August, gold looked like it was bouncing back last year from the slide that it has endured since 2013. Donald Trump's election put an end to that, though -- from the election to the end of December, the price of gold fell nearly 11%.

In the midst of this volatility, however, shares of Newmont Mining (NYSE: NEM), a global leader among gold stocks, climbed more than 84%. Let's dig into the company's performance in 2016, and see what we can expect in 2017.

Image source: Getty Images.

The highlights

To say that Newmont Mining was busy last year would be something of an understatement. For one, the company began gold production at two new locations: Merian and Long Canyon. Located in Suriname, Merian -- of which construction was completed on time and 20% below budget -- began commercial operations in October. Management expects annual average production between 400,000 and 500,000 gold ounces with all-in sustaining costs (AISC) between $650 and $750 per gold ounce during the first five years of operation.

Adding to its portfolio of mines in Nevada, Newmont began commercial production of gold at Long Canyon in November. Similar to Merian, Newmont finished construction at Long Canyon two months ahead of schedule and 18% below budget.

Merian in Suriname. Image source: Newmont Mining.

Management expects the first phase of the project (phase 2 studies are under way)to produce between 100,000 and 150,000 ounces of gold over an expected life of eight years and at an AISC between $500 and $600 per gold ounce.

While bringing new operations online, Newmont was also busy strengthening its portfolio by divesting the Batu Hijau copper and gold mine in Indonesia for a total consideration of $1.3 billion. According to Gary Goldberg, the company's president and CEO, the proceeds from the sale will be used "to continue self-funding our highest-margin projects, retiring debt, and paying competitive dividends."

Another of Newmont's highlights from 2016 was the attention it paid to its dividend. Having distributed $0.025 per share since June 2014, Newmont finally raised it in 2016 -- doubling it to $0.05 per share for the fourth quarter.

An eye on 2017

With a busy 2016 in the rearview mirror, Newmont has several potential growth catalysts in the coming year. The company expects to announce, in the first half of the year, its decisions on whether or not to fund two projects located at the Ahafo Mill in Ghana: Ahafo Mill Expansion and Subika Underground. On the company's Q3 earnings call, Goldberg explained that the Ahafo Mill Expansion would "leverage existing infrastructure to build capacity and improve costs" and the Subika Underground would "produce ore grades that are three times higher than the current surface mine grades." Furthermore, if approved, the two projects wouldadd between 225,000 ounces and 300,000ounces of gold annually with first production in 2018.

In addition to Ghana, Newmont is turning its attention to Australia, where it expects to achieve first gold production -- in mid-2017 -- following the completion of its Tanami Expansion Project. For the past three years, Tanami has averaged annual gold production of 368,000 ounces with AISC of $975 per gold ounce. Management estimates that the Tanami Expansion will result in annual gold production between 425,000 and 475,000 ounces on average after its first five full years of operations.

A golden valuation?

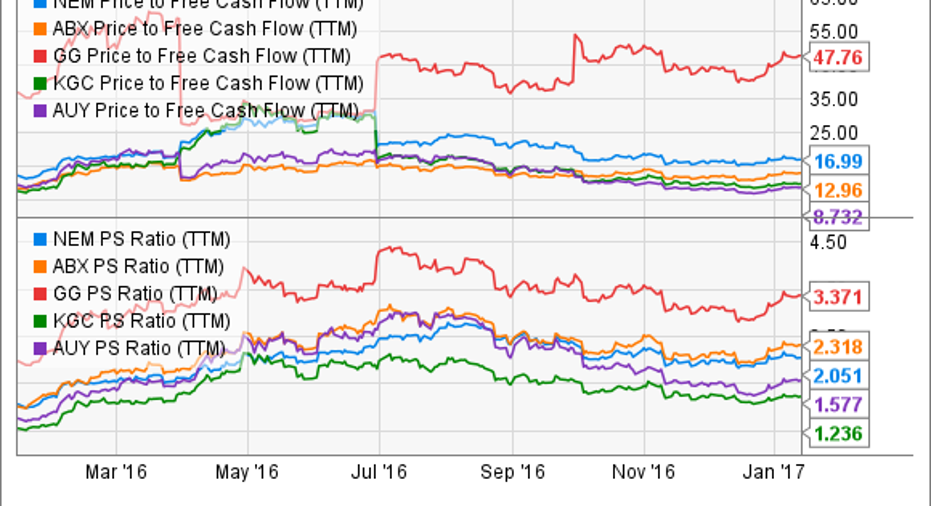

We've looked at what's behind Newmont and what's ahead, so let's turn our attention now to its stock. One thing to remember when evaluating mining companies is that assigning a value to an asset, like a mine, is far from cut and dry; consequently, companies may take large writedowns on their assets, resulting in skewed earnings figures. One thing that can't be massaged, though, is cash flow, so foregoing the traditional price-to-earnings ratio,let's consider the stock in terms of its free cash flow on a trailing-12-month basis.

Over the past year, the stock has traded as low as 11.5 times free cash flow and as high as 31.0 times free cash flow. Currently, shares are trading at about 17 times free cash flow, suggesting that shares are priced aggresively. Not cheap, but not egregiously expensive.

It seems insufficient to consider only one valuation metric, so let's also look at it's price-to-sales ratio on a trailing-12-month basis. Trading at about 2.1 times sales, shares are higher than the midpoint of its high and low for the year -- but still look reasonable.

NEM Price to Free Cash Flow (TTM) data by YCharts.

To provide more context for the stock's valuation, let's consider it alongside its peers:Barrick Gold,Goldcorp, Kinross Gold, andYamana Gold. In terms of free cash flow, Newmont's valuation doesn't raise any red flags. And it certainly seems reasonably priced in terms of sales.

NEM Price to Free Cash Flow (TTM) data by YCharts.

Overall,considering where shares are trading today, the stock seems fairly priced.

The takeaway

Shares of Newmont Mining soared in 2016, but there's no guarantee that it will continue flying higher through 2017. In fact, it seems that Wall Street has gotten this one right by avoiding irrational expectations, or punishing it unfairly. Deftly streamlining its portfolio through divestment and execution of projects in its pipeline, Newmont Mining represents a reasonable consideration for investors looking to gain exposure to the gold industry.

10 stocks we like better than Newmont Mining When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Newmont Mining wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Scott Levine has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.