Melt-Up Fears Mount as Stocks Continue to Shatter Records

For the past five years, crisis-scarred investors have worried time and again about a negative economic or geopolitical event that would send U.S. stocks reeling just like in 2008.

With virtually none of those fears -- from a breakup of the eurozone to a double-dip recession in the U.S. -- panning out, some are now raising the specter of a very different concern: red-hot stock prices could now be overcooking themselves.

First floated earlier this year, talk of a melt-up that could force the Federal Reserve’s hand and trigger a painful correction is growing louder in some corners.

“It is certainly starting to look like a melt-up in stock prices so far this year,” Ed Yardeni, president of Yardeni Research, wrote in a note to clients late last week. “The problem with melt-ups is that they tend to be followed by meltdowns.”

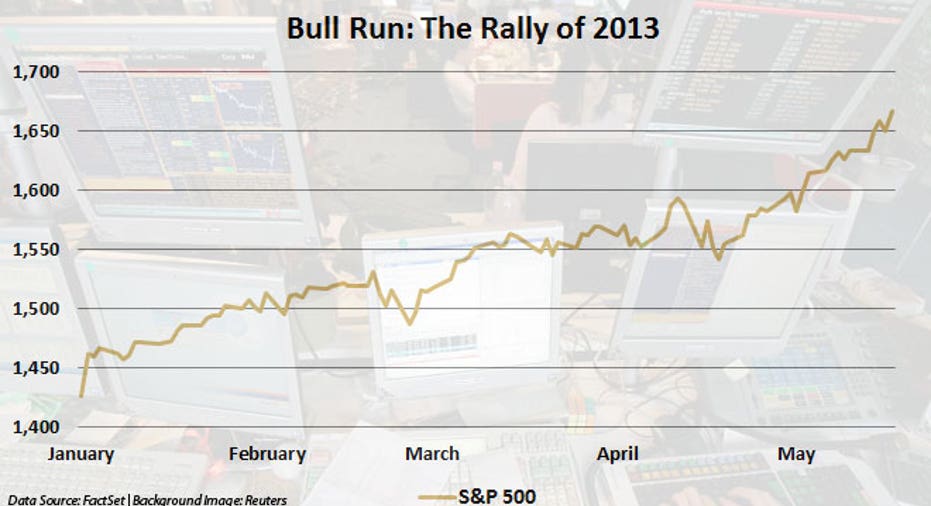

Fueled by the Fed’s controversial bond-buying program and improvements in the economy, U.S. stocks have achieved liftoff in 2013, with the S&P 500 soaring 17% and blowing past many year-end price targets long before Memorial Day.

Off to the Races

The Dow Industrials soared 236 points last week, including a 121-point rally on Friday that gave the index its 21st record close this year alone.

Retreats, let alone selloffs, have been few and far between.

According to Dow Jones, the S&P 500 has closed up 61 of 96 trading days so far in 2013, creating a lofty success rate of 63.5%. That rate is far above the average of 52.1% since 1928 and would be the highest on record for an entire year, according to Walter Murphy, managing partner of Walter Murphy Global Advisors.

“Perhaps now that investors are no longer fearful that the end is near,” Yardeni said, “all the liquidity pumped into the financial markets by the major central banks over the past four years to avert the Endgame scenario is about to cause the Mother of All Melt-Ups.”

What Bad News?

While the bulls may applaud equities’ “resiliency,” some skeptics of the current rally are growing concerned about the markets’ ability to rally on what seems to be bearish news.

For example, the blue chips retreated just 0.28% on Thursday even after a quartet of new economic indicators revealed shrinking U.S. housing starts, a sharp drop in consumer prices, a surprise contraction in regional manufacturing activity and a big jump in jobless claims.

It’s possible market participants didn’t see any cause for concern from the data. It's also possible the bad news was read as a positive because it lessens the chances of the Fed shutting down its quantitative-easing program anytime soon.

Negative economic headlines flash across the screens “and yet the market bids up. That’s just not a normal scenario,” said Brian Sozzi, CEO of Belus Capital Advisors. “Something doesn’t feel right. It just doesn’t add up.”

Chasing Performance

Due to the nature of the business, even skeptics are forced to put their disbelief aside and throw cash into the rallying stock market, adding more momentum to the move higher.

“It’s actually hard to relax in a melt-up because the faster that stocks go vertical, the more we have to worry about picking the top and getting out. If we get out too early, that can harm our careers,” said Yardeni.

“After many investors spent the past three years worrying about a meltdown, now they fear a melt-up."

Yardeni recalled a portfolio manager he knew who was fired in 1999 because he turned bearish on Cisco Systems (NASDAQ:CSCO) a year too early -- but still ahead of the bursting of the dotcom bubble.

Despite his suspicions about the market rally, Sozzi recently raised his year-end S&P 500 price target to 1650 from 1560.

“We’re almost all chasing performance at this time. If you underperform, you lose clients. You have to be involved in the game right now,” said Sozzi, who may raise his price target again soon.

Valuations Haven’t Exploded

While it’s clear the markets have been on a tear, it’s difficult to see the signs of “irrational exuberance” that were evident during the dotcom bubble.

In many ways, market metrics seem to be normalizing from the depressed levels triggered during the worst financial crisis since the Great Depression.

The forward price-to-earnings ratio of the S&P 500 climbed to 14.4 last week, up from just 12.1 in mid-November. While that represents a meaningful expansion, it’s barely above 13.7, which Yardeni said is the mean of this closely-watched barometer since September 1978 when records began.

Dan Greenhaus, chief global strategist at BTIG, said he sees little to indicate a “particularly egregious” rise in valuations.

“People may be wrong but they’re modest. We’re having a bit of a melt-up, but the projections going forward have not melted up,” he said. “We’ve just spent four years getting accustomed to lower-than-expected valuations.”

This may help explain why many Fed watchers still believe the central bank will continue its pace of $85 billion worth of bond purchase per month despite the rising market.

Sozzi said he believes forward P/E ratios would have to grow to the 18-20 range before the Fed took action to taper QE.

“What we’re seeing in the stock market is not translating to the real economy,” he said.

Yardeni said he believes stock prices may “continue to soar this summer,” although he warned of a possible “nasty correction this fall,” which is an historically-difficult season on Wall Street (see: September 2008).

“After many investors spent the past three years worrying about a meltdown, now they fear a melt-up. You have to love our business,” he said.