Main Street Capital Corporation in Stock in 3 Charts

Main Street Capital remains an excellent case study as one of the top-performing companies in its industry. Since inception, it has wildly outperformed its peers, and it all boils down to three simple things.

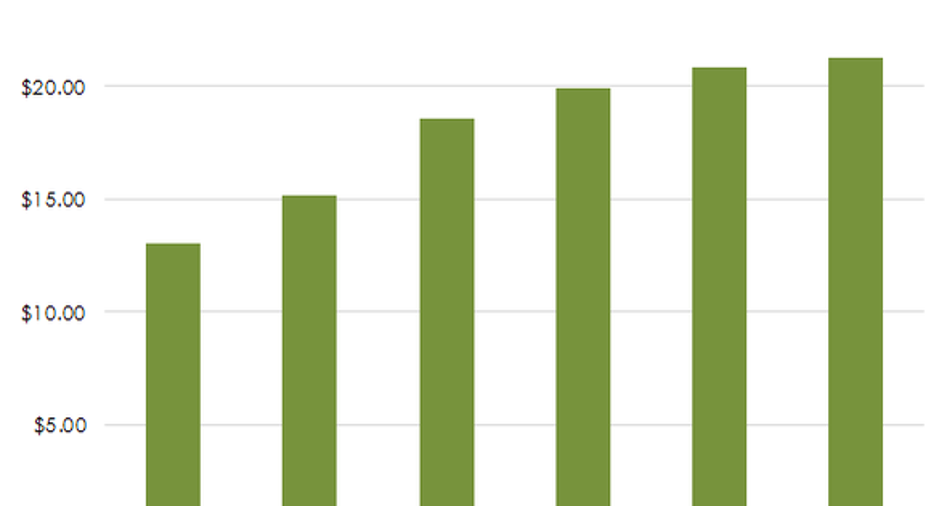

1. Consistent growth in book valueAs a business development company, Main Street Capital chooses to distribute more than 90% of its annual taxable income to avoid corporate-level taxes, similar to how real estate investment trusts work. As a result, it cannot retain substantial earnings to grow per-share book value.

Thus, the only two needle-moving methods for growing book value per share are to:

- Make investments that grow in value over time, and

- issue new shares at prices above book value.

By doing these two things, Main Street Capital has consistently grown its book value per share from $13.06 in 2010 to $21.24 at the end of 2015.

2. Winners outpace losersMain Street Capital makes debt and equity investments in small businesses. Over time, the debt portfolio will naturally erode as interest income is paid out in dividends, and losses take their natural toll to book value. The equity portfolio is thus its greatest source of upside. BDCs aim to recover losses in their debt portfolios by generating gains on their equity portfolios.

Main Street Capital's equity portfolio has allowed it to paper over its debt investment losses over history. The chart below shows its net realized gains or losses on a per share basis since 2010. Note that since 2010, it has generated gains in more years than it has generated losses, and the gains have exceeded these losses.

Gains on the investment portfolio help Main Street Capital afford its semi-annual special dividends, which have recently tallied to $0.55 per share in 2015. Though these have become somewhat "regular" for Main Street shareholders, it's important to recognize that these special dividends will ebb and flow with Main Street's ability to generate net realized gains by selling its portfolio companies at a profit.

3. FrugalityBusiness development companies have been criticized for being managed in ways to maximize compensation for their managers vs. provide outsize returns for their stockholders. Most spend 30% to 40% of their total investment income on compensation in one form or another. Main Street Capital, however, is very frugal, generally spending less than 16% of its total investment income on compensation.

From banks to BDCs, and from private equity funds to public mutual funds, it's a simple fact that a dollar spent on compensation is a dollar that doesn't make it to the shareholders' pockets. Over time, companies that are simply average operationally can outperform by being above average in holding down their expenses.

Main Street's frugality means that even if it turns out to be an average underwriter and operator, its low costs will make it a star in its industry. Unless its underwritingdeteriorates, or its expenses jump significantly, it should continue to command anabove-average valuation.

The article Main Street Capital Corporation in Stock in 3 Charts originally appeared on Fool.com.

Jordan Wathen has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.