KNOT Offshore Partners Solid 2015 Earnings Signals Likely Smooth Sailing in 2016

Source: KNOT Offshore Partners

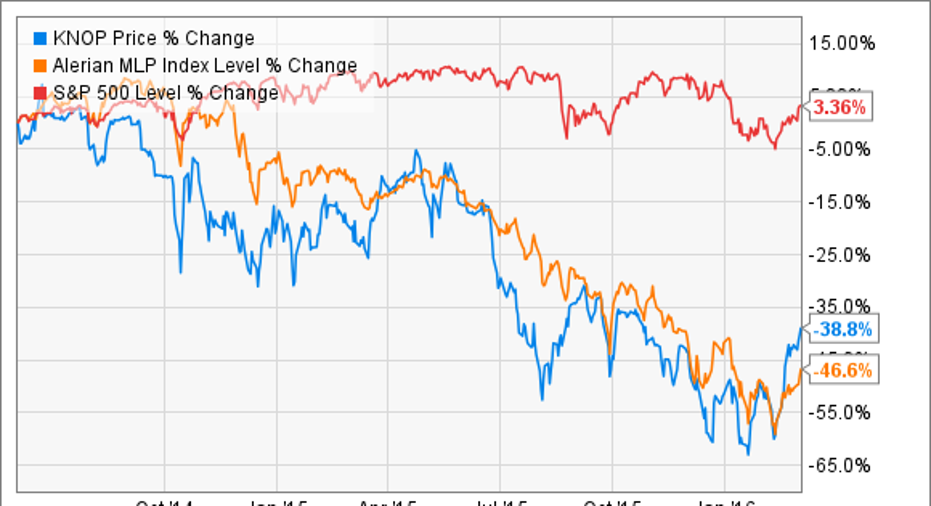

Wall Streethasn't been kind tomidstream MLPs such as KNOT Offshore Partners since the oil crash began around 20 months ago. Based on its performance over the last year, as well as its12+% yield, you'd think that the MLP's business model had dubious growth prospects and a highly risky payout.

Yet 2015's results tell a very different tale. Here's why KNOT Offshore's solidresults last year proves the market is most likely wrong about this shuttle tanker MLP and why 2016 is likely to prove another solid year for dividend lovers.

Solid growth defies oil crash

| Metric | 2014 | 2015 | Change |

| Revenue | $112.8 million | $155.0 million | 37.4% |

| EBITDA | $84.6 million | $123.2million | 45.6% |

| Distributable Cash Flow (DCF) | $46.8 million | $66.9 million | 42.9% |

| Annual Distribution per Unit | $1.85 | $2.06 | 11.4% |

| Distribution Coverage Ratio (DCR) | 1.16 | 1.18 | 1.7% |

Source: Q4 earnings presentation, Yahoo Finance

As you can see KNOT Offshore Partners had a very good 2015. This was courtesy of its ongoing fleet expansion, such as its $115 million October 15th acquisition of the Ingrid Knutsen, which brings its tankercount to 10. In addition, KNOT Offshore's utilization rate remained a stellar 99.9% in the fourth quarterdue to its focus on long-term, fixed-fee contracts for each of itsshipswith large integrated oil giants such as Statoil and Royal Dutch Shell .

In fact, as of the end of 2015 its average remaining contract length stands at 5.6 years, which gives management strong cash flow visibility with which to plan its forward distributions.

That being said the two contract extensions completed in Q4, one with BG Group, now owned by Shell, and the other with Statoil, were only for two years. These shorter-term contracts are likely due to the oil industry's concerns over limited crude oil price visibility over the next few years.

On the plus side the Statoil extension included both a two year option that could allow it to remain in effect through 2019 and was for the same daily charter rate. It also included an annual 1% rate increase, showing that KNOT Offshore's shuttle tankers represent a niche market for which solid demand is likely to keep day rates from tumbling along with oil prices.

Payout profile remains largely unaffected by crude collapse

- Yield: 12.2%

- 2015 DCR: 1.18

- 5 Year analyst annual distribution growth forecast: 1.7%

Wall Street is currently valuing KNOT Offshore Partners as if it had very little growth prospects and an unsustainable distribution. Yet as you can see, the MLP covered it's full 2015 year payout by a wide margin. Also the fourth quarter's coverage ratio was slightly higher than both 2015's and 2014's full year ratios.

Given KNOT Offshore's highly stable cash flow, well secured by long-term, fixed-fee contracts with some of the world's most stable oil companies, what explains the sky-high yield and extremely low valuation? The answer probably lies with analysts' extremely bearish growth forecasts which I believe to be based on the short-term risks to the MLP's growth plans.

Risks to watch going forwardThe midstream MLP business model is based on a partnership paying out the vast majority of distributable cash flow to investors and financing growth through cheap debt and equity.

In KNOT Offshore's case that growth is likely to come from the options it has to purchase five additional shuttle tankers from its sponsor. This potential 50% increase in fleet size would greatly increase its DCF and, if the capital to buy these ships is cheap enough, generate sufficient growth in DCF per unit.

However, with KNOT Offshore's unit price having crashed so severely, this creates a conundrum in the short-term. That'sbecause selling new equity at today's low prices means that such acquisitions would likely not be profitable because they could dilute existing investors so much that DCF per unit actually decreases.

Thus KNOT Offshore's only growth avenue is to buy those tankers by taking on additional debt. However, with$672 million in total debt already outstandingthe MLP's leverage ratio (debt/EBITDA)currently standsat 6.0.While that ratio is far lower than theshipping industry's average of9.0 KNOT Offshoreprobably shouldn't use all debtto acquire all five drop down candidates.

That's because, while thecompany has been able to access debt at relatively cheap leves in the past, the costof additional debt, sufficientto acquire all five potential drop down candidates, may prove too high to make the deals profitable. This indicates that the MLP is best holding off on further tanker purchases until energy prices recover and the market is willing to provide cheaper growth capital.

Bottom lineDon't get me wrong KNOT Offshore Partners isn't without some risks. Its MLP business model means that it remains highly dependent on ongoing access to cheap debt and equity funding. Until oil prices recover enoughthat Wall Street increases KNOT Offshores' equity valuation, the MLP likely won't be able to grow its fleet or its payout.

That being said, I think that Wall Streetis over estimating theshort to medium-term risk to KNOT Offshore's distribution. This creates a potentiallyattractive long-term opportunity that might be just the thing to supercharge long-term dividend investors' diversified portfolios in 2016.

The article KNOT Offshore Partners Solid 2015 Earnings Signals Likely Smooth Sailing in 2016 originally appeared on Fool.com.

Adam Galas has no position in any stocks mentioned. The Motley Fool recommends Statoil (ADR). Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.