Is United Technologies on Track to Deliver Long-Term Value?

The investment case for buying stock in United Technologies Corporation (NYSE: UTX) in 2017 isn't really based on its near-term earnings potential, but rather the successful execution of its ongoing plans to transition the company toward long-term growth. So, let's take a look at the fourth-quarter earnings and conference call in order to benchmark progression toward achieving its aims.

Four key metrics to follow

The key indicators -- one from each segment --were identified and discussed in a previous article. They are as follows:

- Regain market share with Otis elevators in China.

- Successfully and cost-effectively ramp up production of Pratt & Whitney's Geared Turbo Fan (GTF) engine.

- Continue to offset declines in higher-margin legacy aerospace original equipment (OE) sales with cost cuts and increased sales of products on new aircraft programs.

- By management's admission, the climate, controls & security (CCS) segment needs to increase growth and gain market share, and it has an opportunity to do so given the raft of new products it has available.

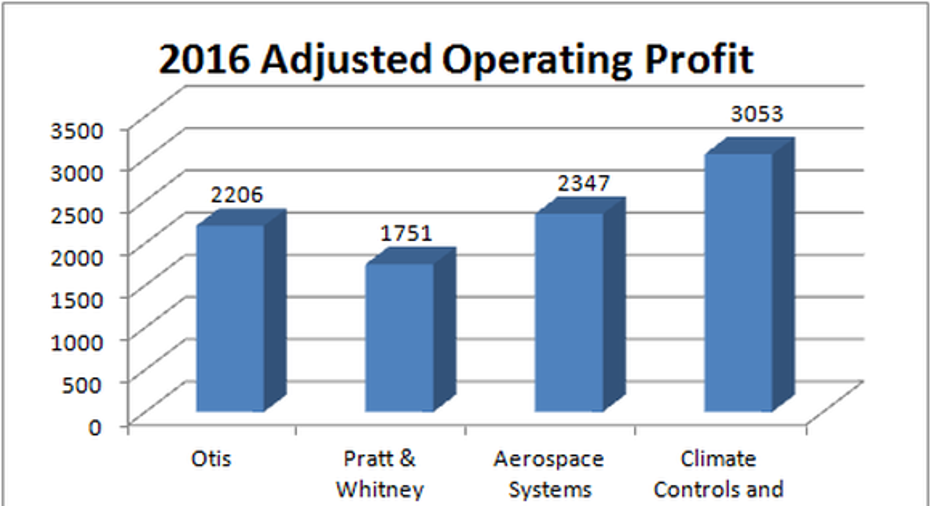

For context, here's 2016 segment adjusted operating profit.

Data source: United Technologies Corporation presentations. Chart by author

Otis elevators

The aim is to lowerpricing in order to increase equipment market share in China and so drive future higher-margin service revenue growth. Unfortunately, the China market is highly competitive, and slowing economic growth put pressure on pricing for Otis in 2016.

However, CFO Akhil Johri had some positive news on China in the fourth quarter: "We've seen 4% to 5% growth in our unit orders and we know that the market is declined by about 5%." Moreover, pricing declines appear to be abating, with pricing down6%-7% in the fourth-quarter compared to reductions in the "9% range that we've seen before." For reference, management expects pricing declines of 5%-6% on Otis new equipment business in China in 2017.

But don't think the immediate benefits will be seen in Otis in Chinajust yet. For example, CEO Greg Hayes outlined the importance of density, in other words, the number of elevators to service within a given area, estimating that Otis has 175,000 under current maintenance contracts. However, a figure above 250,000 is seen as necessary before a "profitability increase" occurs -- something Hayes sees as "probably five years" away.

All told, if the fourth quarter proves a useful guide, then Otis is achieving its aim of growing market share, and pricing pressure -- although still significant -- appears to be abating in line with plans.

Pratt & Whitney plans to produce 350-400 geared turbo fan engines in 2017. Image source: United Technologies.

Pratt & Whitney Geared Turbo Fan production

Pratt & Whitney failed to hit its production target in 2016, and it faced technical and supply chain issues that caused delays, forcingBombardier and Airbus to alter their delivery schedules. Meanwhile, Jeff Immelt, CEO of key rival General Electric Company (NYSE: GE), claims to be "gaining share with LEAP in the narrow-body segment." GE is a joint partner with France's Safran in CFM International, a company whose LEAP engine competes with Pratt's GTF on the Airbus A320neo.

Johri outlined that 62 GTFs were produced in the fourth quarter, a figure aligned with "what we need in the first quarter, and January so far has been trending OK as well." He went on to declare he felt "very good" about the target to produce 350 to 400 GTFs in 2017. Meanwhile, Hayes pointed out that the issues on the GTF aren't related to the gear system, and fixes are in place for the combustor and oil seal issues.

Ultimately, Johri confirmed his expectation that negative engine margin (losses taken as new engine sales increase before profitable aftermarket sales start to offset them) would peak at $1 billion in 2018.

All told, Pratt & Whitney appears to be on track with GTF production, but investors will want to see execution on the outstanding technical difficulties, particularly as GE is executing well with its LEAP engine.

United Technologies's Carrier air conditioning systems. Image source: United Technologies.

CCS & Aerospace systems

Climate, controls & security equipment orders were up 2% in the fourth quarter (6% including services), with Johri pointing out this was the first time in 2016 that they were in positive territory. However, it's too early to call this an improvement in CCS, and the optics won't get any clearer in the near term,because the first quarter is expected to deliver the lowest organic growth figure for CCS in 2017 -- with growth ultimately picking up in the second half.

Full-year aerospace systems operating profit was "in-line with expectations," but declines in legacy products and military sales continue to more than offset growth on products on new aircraft programs. The segment will continue facing headwinds in 2017, but the 4% operating profit growth in the fourth quarter suggests management will achieve its aim of growing adjusted operating profits by $50 million to $100 million for the segment in 2017.

Looking ahead

All told, it was a pretty solid execution, and United Technologieslooks to be on track with its long-term objectives. Otis and CCS are expected to see growth increase in the second half, but investors need to keep an eye on GTF production at Pratt & Whitney and military volumes in aerospace systems.

United Technologies isn't a stock with an obvious or immediate upside potential, but if the company executes its plans, I think long-term appreciation is likely.

10 stocks we like better than United TechnologiesWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now...and United Technologies wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017.

Lee Samaha has a long position in United Technologies.The Motley Fool owns shares of General Electric. The Motley Fool has a disclosure policy.