Is Transocean About to Make a Big Splash in the Offshore Rig Industry?

It might not look like it based on Transocean's (NYSE: RIG) most recent earnings reports, but the company is making some very large strides to improve its position in the rig market. While once seen as a company with an extremely old, ineffective fleet, Transocean now looks younger, leaner, and ready to position itself for the upturn in the offshore market.

In fact, Transocean is so confident in its current position that it thinks it can do something that has been almost completely unheard of in recent years: According to executives in its fourth-quarter earnings call, it's ready to make an acquisition. Here are some notable quotes from the call that illustrate what management is thinking.

Image source: Getty Images.

Taking the lion's share of the market

There hasn't been a lot of new work for rigs out there. So even the shortest, cheapest contract can be helpful in putting some cash in the coffers. According to Transocean CEO Jeremy Thigpen, the company has actually been doing a rather remarkable job of capturing what little work that is available:

It may not be showing up much in the bottom line of Transocean's results, but keeping rigs working at even the most modest profits will go a long way for any rig company, especially since we have yet to hit the bottom of the market.

Changing the game

As the offshore rig industry goes through this deep downturn, one of the silver linings is that it is forcing companies to think of better ways to operate. One thing that Transocean is looking to do is coordinate more with its suppliers and equipment manufacturers to lower operational downtime and maintenance costs. According to Thigpen, the company is trying a novel approach:

Transocean isn't the only company taking this kind of approach to equipment performance. In 2016, Diamond Offshore (NYSE: DO) signed an agreement with General Electric (NYSE: GE) where it sold its blowout preventers back to GE and, in exchange, will lease them from GE. The idea here is that the OEM will have a better understanding of the equipment itself and will be more in tune with the maintenance needs. It also puts skin in the game for the OEM, as it is only paid for when the equipment is in use.

This seems to be a trend taking hold across the industry, so don't be surprised if we see more offshore rig owners move toward these equipment leasing options in the future.

The turning point

Probably the thing that investors care about more than anything else is when we can expect the market to turn for offshore operators. Based on Thigpen's statements, 2017 isn't going to be the year. Integrated oil and gas companies (thinkExxonMobiland Chevron) represent the bulk of offshore development money, and those players don't have much of their budget dedicated to offshore work and reserve replacement. But Thigpen's more optimistic about 2018:

Still turning over the fleet

Transocean has been the most aggressive company in terms of scrapping older rigs that probably won't have much use in the future. The demands from operators today mean only the highest-specification rigs get work. As much work Transocean has done in right-sizing its fleet, Thigpen admits there is still lots of progress left to be made by the industry as a whole:

Transocean's most recent rig report showed it had nine older rigs that are only deepwater and midwater capable.These are the most likely candidates to be recycled. Some are still under contract, though, so don't expect them to be sent to the scrap yard before their contracts are up.

Time to buy?

This was probably the most interesting quote from the whole earnings call. Thanks to Transocean's efforts to right size the fleet, delay delivery of some rigs under construction, and maintain a strong balance sheet, Thigpen actually sees a ripe opportunity to make some acquisitions:

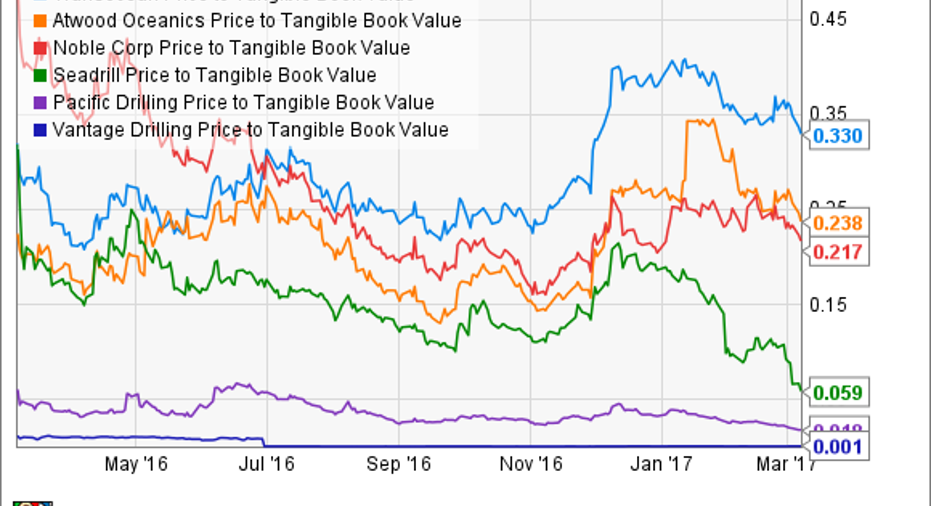

Thigpen went on to say that there two ways Transocean can deal with this. Either it can use cash to take over a shipyard delivery that was supposed to go to another player, or it could use its equity to absorb a competitor. Using equity today isn't ideal -- shares are trading for the absurdly cheap valuation of 0.31 times tangible book value -- but even that low share price is better than some of its peers.

RIG Price to Tangible Book Value data by YCharts.

If the company is going to make those kinds of deals, though, CFO Mark Mey thinks the company will need to act fast to get the best deal possible.

Transocean has pretty much been the only company as of late to discuss the possibility of making an acquisition right now, which shows what kind of strength it has in the market in general. If this isn't a sign that the company is one of the best-positioned to bounce back in the offshore drilling industry, I'm not sure what is.

10 stocks we like better than TransoceanWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Transocean wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Tyler Crowe owns shares of General Electric and Seadrill. The Motley Fool owns shares of and recommends Atwood Oceanics. The Motley Fool owns shares of General Electric. The Motley Fool has a disclosure policy.