Is Rockwell Automation a Buy for 2017?

As I write, Rockwell Automation (NYSE: ROK) stock is up by a third on a year-to-date basis, but the question investors will be asking is whether the run can continue in 2017.

In this vein, let's look at management's commentary and outlook from the recent fourth-quarter results and investor conference. Here's what you need to know before making an investment decision.

IMAGE SOURCE: ROCKWELL AUTOMATION WEBSITE.

Guidance

Following a 3.9% decline in organic sales growth in 2016, management forecasts a return to growth in 2017. In addition, acquisitions are expected to add 1.5% to reported sales growth, with currency taking away 0.5%.

The end result isan outlook forsales growth of around 2%, but there won't be much operational leverage into notably higher EPS, because Rockwell faces some margin headwinds. Segment margin headwinds -- restoration of incentive compensation, unfavorable currency exchange rates, and increases in operating pension expense -- and a slightly higher tax rate are holding back EPS growth.

| Metric | Guidance for 2017 | Notes |

|---|---|---|

| Organic sales growth |

0% to 4% |

2% midpoint |

|

Segment operating margin |

20% |

Lower by 20 bp |

|

Adjusted effective tax rate |

24% |

Higher by 40 bp |

|

Adjusted EPS |

$5.85 to $6.25 |

(1.3%) to 5.4% |

|

Free cash flowas % of adjusted income |

100% |

Down 7% |

DATA SOURCE: ROCKWELL AUTOMATION PRESENTATIONS. TABLE BY AUTHOR. BP IS BASIS POINTS, WHERE 100 BP EQUALS 1%.

Forward valuation

Turning to valuation, the adjusted EPS range puts Rockwell Automation on a forward P/E range of 23.4 to 21.9 times earnings. Meanwhile, it looks as though it will generate 4.5% of its enterprise value (market cap plus net debt) in free cash flow in 2017.

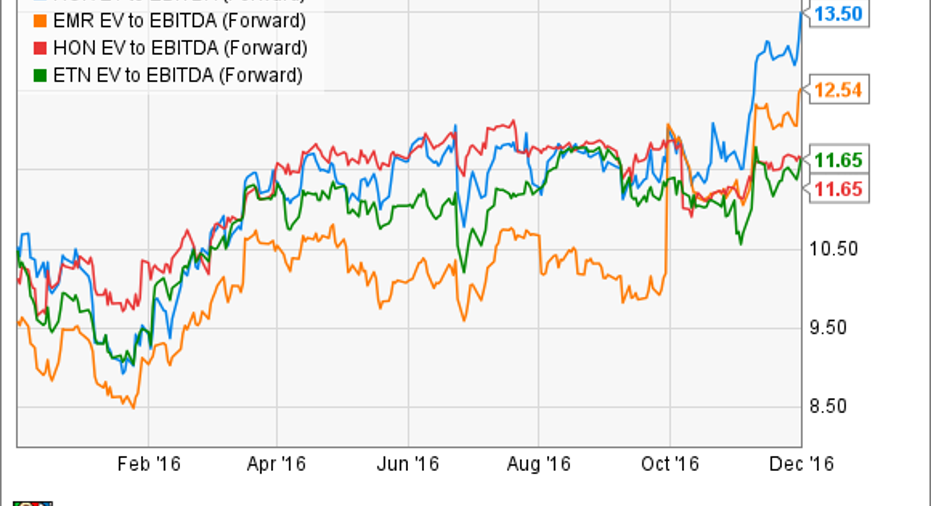

Finally, thanks to a large increase in the share price, Rockwell is no longer cheap on an absolute or peer group basis.

ROK EV to EBITDA (Forward) data by YCharts

Investors have bought into cyclical stocks such as Rockwell and Emerson Electric (NYSE: EMR) in the hope that a Donald Trump presidency will lead to a pickup in the U.S. industrial economy. In addition, as the speculation on Emerson Electric's making a bid for Rockwell has subsided, the latest market rumors suggest that France's Schneider Electric SE (NASDAQOTH: SBGSF) might be interested in a bid.

Growth drivers

In common with Emerson Electric, much of Rockwell's revenue depends on more economically sensitive capital spending rather than operational expenditures. So with Rockwell's valuation seemingly being bolstered by belief in a cyclical pick-up and some bid speculation, it's worth taking a look at potential earnings upside drivers and the assumptions made in management's guidance.

Rockwell's stock is pretty attractive in terms of long-term prospects -- not least from its Industrial Internet of Things (IIOT) exposure and positioning as a strategic U.S. asset -- so let's focus on three near- to mid-term considerations:

- Industrial production outlook in 2017.

- Assumptions in guidance with capital spending in oil and gas and heavy industries.

- Asia-Pacific growth.

CFO Ted Crandall believes Rockwell's business "tracks best with levels of industrial production" and referenced forecasts for industrial production to grow 1% in 2017 following a 0.2% reduction in 2016. For reference, FedEx Corporation expects U.S. industrial production to grow 1.7%, compared with a 0.9% decline in 2016.

Image source: TRADINGECONOMICS.COM.

Oil and gas and Asia-Pacific spending

CEO Blake Moret expects "continued growth in the consumer and auto verticals and with heavy industries about flat year over year," while Crandall outlined that oil and gas and mining largely "pulled down heavy industry verticals' in 2016. Clearly, management expects some stabilization in oil and gas spending in 2017.

Turning to Asia-Pacific, in the fourth quarter Rockwell generated 5.4% organic sales growth in the region -- markedly above the overall 4% decline -- with China up in the low single digits. On the earnings call, Moret argued that China's need to improve to Western levels of productivity would drive adoption of Rockwell's solutions in the future. In other words, demand could be structural and therefore less dependent on cyclical factors.

ROCKWELL AUTOMATION HELPS COMPANIES IMPROVE PRODUCTIVITY. IMAGE SOURCE: ROCKWELL AUTOMATION WEBSITE.

Is Rockwell a buy?

Given the steep rise this year and the current valuation, it's hard to argue that the stock is cheap. On the other hand, there's an obvious long-term attraction of an industrial software company focused on increasing productivity through IIOT-relevant solutions.

Ultimately, the decision probably boils down to your level of confidence in industrial production growth next year, as well as a stabilization in oil and gas spending -- something Rockwell's outlook is contingent upon. In my opinion, there are probably cheaper ways to play these themes than Rockwell, and investors might look out for a better entry point.

10 stocks we like better than Rockwell Automation When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Rockwell Automation wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of Nov. 7, 2016

Lee Samaha has no position in any stocks mentioned. The Motley Fool recommends Emerson Electric. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.