Is Healthcare Going to Bankrupt the Average American Retiree?

Source: Flickr user pictures of money.

Sky-high drug prices have been in the news lately, but it's not just drug prices that pose a risk to retiree savings. Health-insurance and long-term care costs are increasing, too, and that has more Americans worrying about their financial security in retirement than ever before.

A big problem gets biggerAccording to the Centers for Medicare and Medicaid Services (CMS) office of the actuary, total spending on healthcare in America grew by 5.3% last year -- the fastest increase in five years.The 5.3% increase comes on the heels of a 3.7% increase in 2013, and a 2.9% increase in 2012.

Overall, the lift in spending brought total spending on healthcare by Americans north of $3 trillion for the first time. That means that the average American was on the hook for $9,523 in healthcare expenses in 2014.

Doubt setting inThe rising cost of healthcare is particularly worrisome to retirees. Baby boomers are turning 65 at a pace of 10,000 people per day, and longer more-active lifestyles means that more of these boomers are going to require healthcare than at any time in our history.

According to a retirement study conducted earlier this year by the Employee Benefit Research Institute (EBRI), less than 40% of America's retirees are very confident that they have enough money to cover their medical expenses, and 21% of Americans are either not too confident, or not at all confident, in their ability to pay for their medical expenses in retirement.

Retirees are even more concerned about the prospect of having to pay for long-term care. Only a quarter of retirees are very confident that they have enough money to cover long-term care expenses, while 38% are either not too confident, or not confident at all.

What's behind the problem?In some ways, the increase in spending last year isn't unexpected. After all, more people are signing up for health insurance because of health reform, and those newly insured Americans are using more healthcare services.

While short-term increases in healthcare spending associated with expanding access to preventative care may provide long-term healthcare savings by reducing expensive chronic conditions, those savings aren't a given. Even if they do occur, it could still be years before Americans see that benefit impact their wallets. In the meantime, Americans are left figuring out how to pay for medical bills that are growing more quickly than their incomes.

According to the Kaiser Family Foundation, the average premium for the second lowest-cost silver medal health insurance plan offered on the Affordable Care Act exchanges will cost 10% more in 2016 than it did in 2015. The increase in health insurance premiums is even greater in certain areas of the country. For example, residents of Montana will see premiums on their plans soar by 32%, and Tennesseans will pay 38% more for those plans than they did this year.

Premium increases, however, are only part of the problem. Costs for next-generation medicine for common diseases, including cancer and heart disease, are jumping, too. According to the Memorial Sloan Kettering Cancer Center, four out of the five cancer drugs approved by the FDA in 2014 hit the market with monthly price tags north of $12,000, andthe FDA approval of two new $14,000-per-year cholesterol-busting drugs this past summer could add billions of dollars annually to the cost of heart-disease prevention.

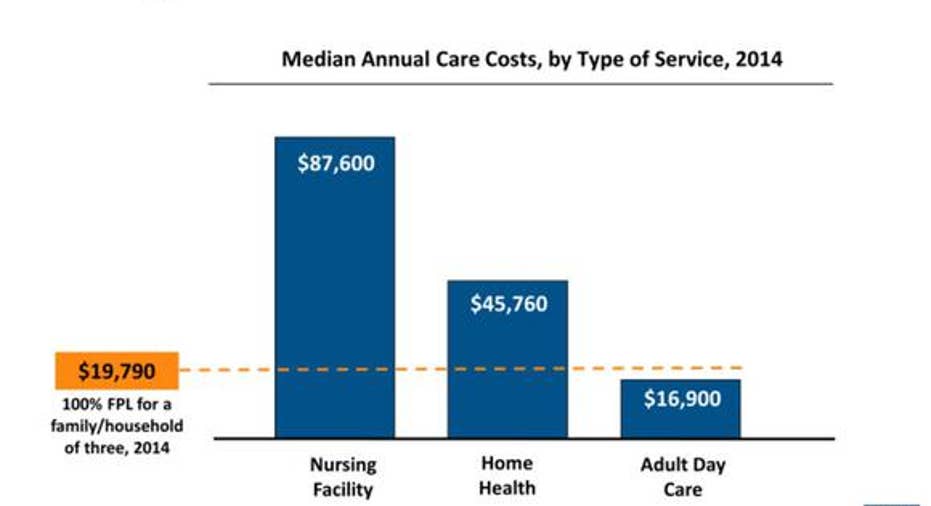

Those threats are substantial, but sky-high long-term care costs could pose an even bigger problem for retirees. Kaiser estimates 70% of Americans currently age 65 or older will use long-term care,and at an average cost of $87,600 annually for nursing facility care last year, it's not hard to understand why Americans doubt that they'll be able to foot the bill for long-term support and services.

Minimizing the risk posed by healthcare costsAlthough many insurance programs use drug reimbursement "tiers" that can increase the out-of-pocket cost to patients, and health insurance premiums are heading higher, healthcare insurance remains the best way to keep healthcare costs from zapping retirement savings.

If you already receive Medicare, you may be able to further minimize the risk of rising healthcare costs by buying supplemental insurance that can significantly reduce out-of-pocket costs. If you end up diagnosed with cancer, or another life-threatening and expensive condition, the extra premiums paid for more comprehensive insurance could go a long way toward protecting your nest egg.

Similarly, while long-term care insurance isn't cheap, people who can afford it may come out ahead in the end if they end up needing care at a long-term care facility, especially because Medicare only provides very limited coverage for those services.

If you're not retired yet, and you're still working, the best way to help insure your financial security may be to be proactive about your retirement planning. Developing a plan that includes expectations of your annual income needs, and the amount that you'll need to invest each year to reach that goal, is critical.

Once you've come up with your target savings goal, make sure you take advantage of tax-advantaged retirement accounts. Many Americans fail to max out their annual contribution to their 401(k) and IRAs. If you're one of them, consider committing to maxing them out in 2016.

Americans can contribute $18,000 to a 401(k) plan next year, and the maximum contribution to an IRA is $5,500 in 2016. If you're over 50, the IRS allows you to make catch-up contributions, too. In 2016, people can contribute an additional $6,000 to their 401(k) plans and an additional $1,000 to their traditional or Roth IRA plans if they're over 50.

Being adequately insured and investing enough for retirement won't guarantee that you can pay for all your healthcare costs in retirement. Doing so, however, remains the best way to make sure your retirement savings don't disappear too quickly when illness or injury strikes in your golden years.

The article Is Healthcare Going to Bankrupt the Average American Retiree? originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.