Is Cisco Systems' Dividend Sustainable?

Image source: Cisco Systems.

Networking giant Cisco Systems has been a bit of an underperformer over the past year. The stock has fallen about 9% compared with the S&P 500, which has dropped 2%. Although the stock has struggled, the business performance has been better.

Over the 12 months ended in late January, when Cisco last reported earnings, the company has been able to grow revenue a little over 3% and take much more of that growth to the bottom line. Earnings per share grew nearly 22% over the same period. Return on equity came in at an impressive 17.3%.

The company's five-year performance hasn't been too shabby, either. Revenue and EPS have grown an annualized 4.2% and 5.6%, respectively. The stock has more or less mimicked the S&P 500's returns, increasing 50% over the past five years. It's not knock-it-out-of-the-ballpark performance, but the slow and steady progress has allowed the company to increase its annualized dividend from $0.12 per share in 2011 to $1.04 today.

An increasing dividend coupled with a falling stock price has resulted in a stock that is paying a 3.9% dividend yield as of this writing. While this may be impressive, it is also worrisome at first glance. As the dividend yield creeps up to 4%, it would be prudent to analyze if Cisco's payout is sustainable.

Payout ratios

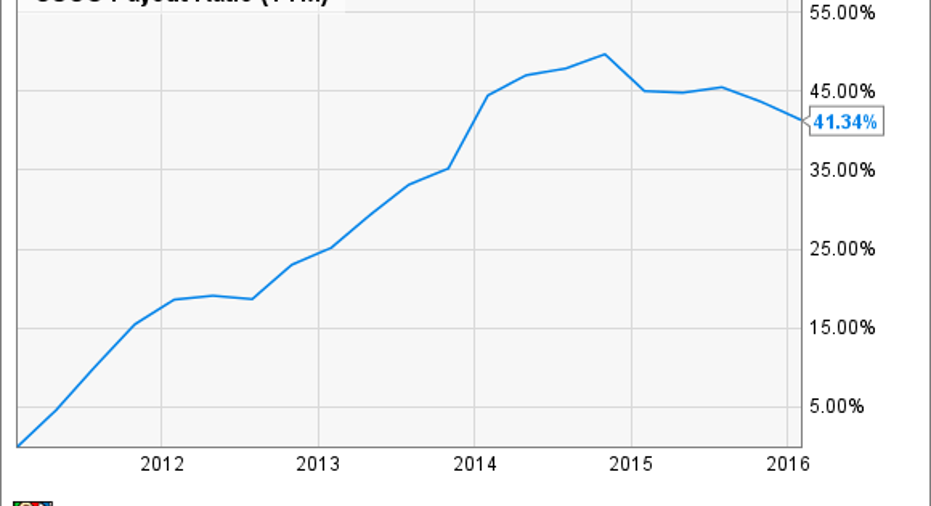

The simplest way to measure if a dividend is in danger of being cut is to compare the payout amount to the amount of money the company made. As the dividend payout ratio increases, the less money the business retains to fund operations or invest in itself.

CSCO Payout Ratio (TTM) data by YCharts

Since Cisco implemented a dividend in 2011, the proportion of its earnings paid out to shareholders steadily increased before slightly declining again this last year. Despite the increase, a dividend payout ratio of 41% is still reasonable for a company like Cisco. Technology peer Intel , for example, has a payout ratio of 44%.

One flaw with the dividend payout ratio is that the metric compares dividends to earnings. Earnings can have a lot of noise that doesn't directly affect the true earnings power of the company. This noise includes depreciation, share-based compensation, and one-time charges. When comparing dividends paid to free cash flow, Cisco's payout ratio decreases to 34%, well in line with some of its peers.

|

Company |

Free Cash Flow (TTM) |

Dividends Paid (TTM) |

Dividend-to-FCF Ratio |

|---|---|---|---|

|

Apple |

$55.17 billion |

$11.89 billion |

21.6% |

|

Microsoft |

$23.65 billion |

$10.68 billion |

45.2% |

|

Cisco |

$12.61 billion |

$4.27 billion |

33.9% |

|

Intel |

$11.89 billion |

$4.65 billion |

39.1% |

Source: YCharts.

Balance sheet

A strong balance sheet can also help a company navigate through choppy waters and a strong cash position with manageable debt levels should safeguard investors from a dividend cut.

As of the end of its most recent quarter, Cisco's cash balance exceeded $60 billion. Current liabilities, which are payments expected to be paid out within the next year, were only $23 billion. When looking at both short-term and long-term obligations, Cisco has done a tremendous job maintaining a strong financial position.

| Metric |

2011 |

2012 |

2013 |

2014 |

2015 |

Most recent |

|---|---|---|---|---|---|---|

|

Quick ratio |

3.09 |

3.29 |

2.80 |

3.18 |

3.04 |

3.23 |

|

Long-term debt-to-equity |

34.4% |

31.8% |

21.9% |

35.9% |

35.9% |

35.5% |

Source: author's calculations using company data.

The quick ratio basically tells investors that the company has over 3 times the liquid assets to cover its current obligations to outside parties. With only a third of its capital structure in debt and a strong quick ratio, signs suggest that Cisco has a strong enough balance sheet to weather most storms.

Bottom line

In this low-rate environment where investment income is difficult to come by, Cisco Systems may be an attractive opportunity for investors. The company has consistently increased its dividend while delivering solid business performance. The balance sheet is strong, with a cash balance that leaves room for the company to not only explore growth opportunities but also increase future payouts.

The article Is Cisco Systems' Dividend Sustainable? originally appeared on Fool.com.

Palbir Nijjar owns shares of AAPL. The Motley Fool owns shares of and recommends AAPL. The Motley Fool owns shares of MSFT and has the following options: long January 2018 $90 calls on AAPL and short January 2018 $95 calls on AAPL. The Motley Fool recommends CSCO and INTC. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.