IRS Tax Brackets 2017: What You Need to Know

If you want to figure out what you'll owe in taxes next year, then you need to know the tax brackets that the IRS puts out every year. Long before most people even start thinking about filing their taxes for 2016, the 2017 tax brackets become available for those who want to do advance planning on their taxes for the coming year. Below, we'll show you the IRS tax brackets for 2017 so that you can use them in your tax planning.

Image source: Getty Images.

2017 tax brackets for singles

Single filers are those who are not married and don't qualify for preferential treatment as heads of household or qualifying surviving spouses. Their brackets are below.

Source: IRS.

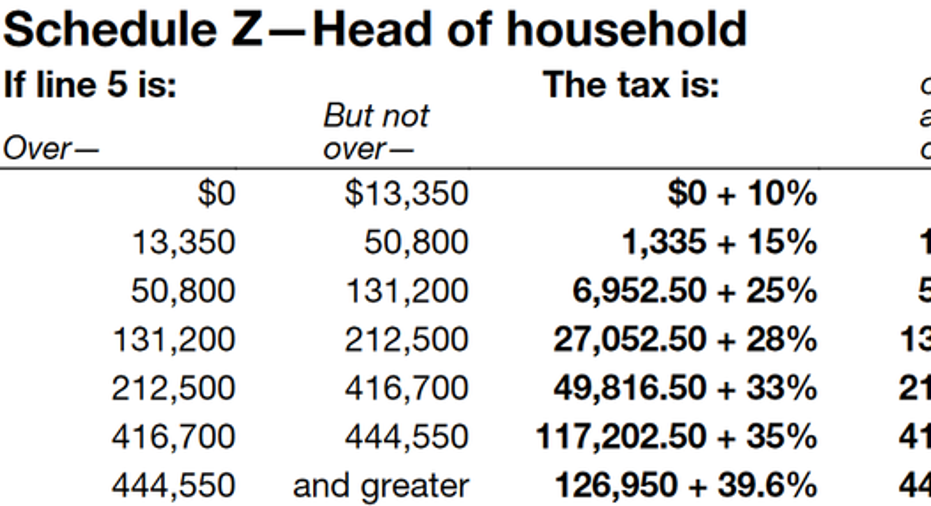

2017 tax brackets for heads of household

The head of household status is available to those who are unmarried and support a child, parent, or other relative who meets certain conditions. Among those conditions are that qualifying persons have to live with you more than half the year, and in many cases, you must be able to claim them as dependents. As you can see below, the brackets are wider than they are for single filers.

Source: IRS.

2017 tax brackets for married joint filers

Most married couples file joint returns. The brackets below apply to them, as well as to qualifying surviving spouses.

Source: IRS.

2017 tax brackets for married separate filers

Married couples have the option of filing separately. It's unusual because most couples pay more tax filing separately, but in some cases, it makes sense. The brackets are below.

Source: IRS.

How to use tax brackets to calculate your tax

These tax brackets are a good starting point to figure out your tax liability for 2017. However, keep in mind that the brackets are based on taxable income, which is not the same as your gross income. Taxable income is what the brackets refer to above as "Line 5," and it includes not only all your income, but also the deductions that you're eligible to take, like the standard deduction, personal exemptions, deductible retirement account contributions, or a host of other provisions available to those who take itemized deductions. It's that net figure that you plug into these brackets to determine your tax.

As an example, say you're single and have taxable income of $40,000. Looking at the brackets, $40,000 falls between $37,950 and $91,900. So go to that line in the relevant table and read it from left to right. You'll take $5,226.50 and then add 25% of income exceeding $37,950. Your income above $37,950 is $2,050 ($40,000 - $37,950), and 25% of that is $512.50. Therefore your tax owed will be $5,226.50 plus $512.50, or $5,739. Note that even though your $40,000 income puts you in the 25% bracket, the percentage of your income that you actually pay in tax is much lower, at just over 14% ($5,739 / $40,000).

Of course, these tax brackets only give you half the story when it comes to your 2017 taxes, because you don't yet know your taxable income. However, if you have a stable income that's reliable and not in doubt, then you'll be able to take an educated guess about your income over the course of the year. Using these tax brackets to estimate your tax liability for 2017 will get you a step ahead of most taxpayers going into the coming year.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.