IRS Form 1099-R: What Every Retirement Saver Should Know

Saving for retirement can take your entire career, but when it comes time to retire, you want to make sure your savings work as hard as they can for you. With tax-favored accounts like IRAs, 401(k)s, and other employer-sponsored retirement plans, the tax-deferred growth they offer can dramatically boost your savings. But when it comes time to take withdrawals, you'll have to deal with the tax consequences, and Form 1099-R will help you understand the tax treatment of the money you take from your retirement accounts.

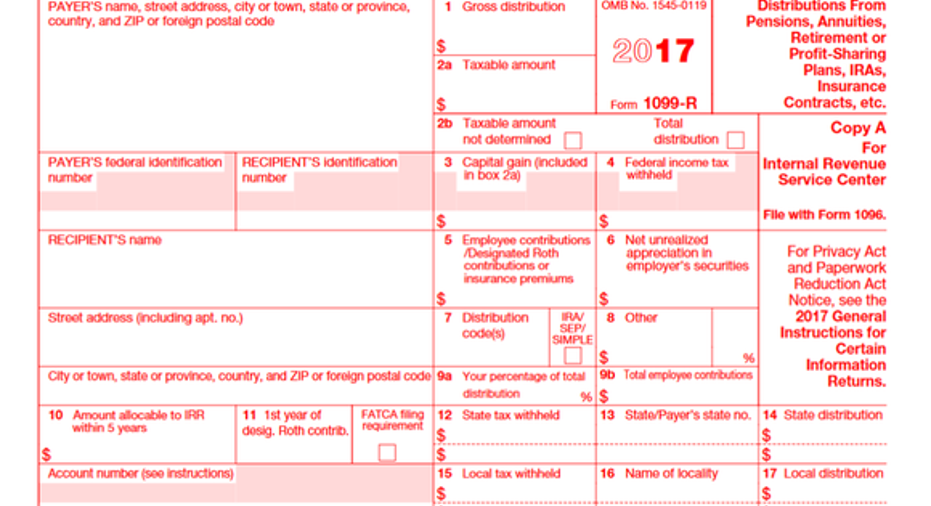

Image source: IRS.

Will I receive IRS Form 1099-R this year?

Financial institutions that hold IRAs and other tax-favored retirement accounts must file Form 1099-R if they made distributions of $10 or more during the year. The provision also applies to traditional pensions, annuities, insurance contracts, and other related payments.

You'll also get a 1099-R if you do a direct rollover of your retirement plan to another eligible tax-favored account, such as an IRA or another retirement plan. As we'll see below, that doesn't mean that you'll owe tax on the amount moved, but you'll still need to include the reported distribution on your tax return in the appropriate spaces. Also, for direct transfers that don't involve your ever receiving custody of the funds, you shouldn't get a 1099-R, as the IRS doesn't require a report on direct transfers.

How do I use the information on Form 1099-R?

The two most important numbers on Form 1099-R are in boxes 1 and 2a. Box 1 includes the total amount of money that the financial institution distributed from your retirement account. Box 2a indicates how much of that distribution was actually taxable. While you'll report the Box 1 figure on your tax return, the number that gets added into your gross income is the Box 2a figure. In some cases, if the payer can't figure out how much of your distribution is taxable, then Box 2a will be blank, and Box 2b will have a checkmark next to "taxable amount not determined."

In addition, if you had money withheld from your retirement account distribution to cover taxes, you'll need to make sure that you account for that to avoid paying tax twice. Box 4 indicates how much you had withheld to go toward federal income taxes, while Box 12 includes any state income tax withholding, and Box 15 shows withholding for any applicable local tax.

The other boxes largely cover special situations. Box 3 includes any distributions treated as capital gains, which are more common with annuity distributions than with retirement accounts. Box 5 includes any contributions that are eligible for tax-free withdrawal, such as Roth contributions. Box 6 covers the situation in which your retirement plan holds company stock that is eligible for special gains treatment.

The Box 7 distribution code can be helpful in determining whether a withdrawal is taxable or not, as well as whether it is subject to a potential 10% penalty for participants who are under age 59 1/2. Codes will indicate whether a distribution is normal, early, or due to death or disability of the participants, as well as adding more specific information about the reason for the distribution. You can find codes in the instructions for Form 1099-R at the IRS website.

What to watch out for with Form 1099-R

The biggest thing to remember is that the IRS will also get a copy of your Form 1099-R directly from the financial institution that handles your retirement account. You will therefore need to make sure you report your distributions properly, or else the discrepancy will potentially trigger an IRS audit.

Form 1099-R is a key part of understanding the taxation of retirement account distributions. After saving throughout your entire career, making sure that your withdrawals from your retirement savings get taxed properly is essential to protect your financial security in your golden years.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

The Motley Fool has a disclosure policy.