Improving This Would Really Help Bank of America

If there's one thing that would supercharge Bank of America's (NYSE: BAC) ongoing recovery from the financial crisis, it's a higher debt rating. Not only would a higher rating reflect the bank's progress over the past eight years, but it would also lower its cost of funds and thereby boost its earnings.

While there are three major ratings agencies, you only need to look at one of them to get a sense for Bank of America's opportunity for improvement. To this end, Moody's gives Bank of America's long-term debt a rating of Baa1. That rates the $2.2 trillion bank below many of its staunchest competitors.

|

Bank |

Long-Term Senior Debt Ratings from Moody's |

|---|---|

|

U.S. Bancorp |

A1 |

|

Wells Fargo |

A2 |

|

BB&T |

A2 |

|

JPMorgan Chase |

A3 |

|

PNC Financial |

A3 |

|

Bank of America |

Baa1 |

Data source: U.S. Bancorp.

A bank's debt ratings matter because they dictate the interest rate at which a bank can borrow money, with a higher rating translating into a lower cost of funds.

Last year, for example, Bank of America borrowed nearly $230 billion on a long-term basis at an average annual rate of 2.44%. Wells Fargo, which has a higher debt rating, had roughly the same amount of long-term debt as Bank of America did, but its interest rate was only 1.6%. Translated into dollars and cents, this means that Wells Fargo spends $2 billion less a year to borrow the same amount of money as Bank of America does.

The good news is that the North Carolina-based bank is headed in the right direction. At the end of January, Moody's changed its outlook on Bank of America from stable to positive, citing its improved profitability in particular:

Moody's went on to cite Bank of America's goal to reduce expenses by an additional $3 billion by the end of 2018, as well as the benefit that rising rates will have on its top line. "A realization of the bank's latest cost targets, combined with an increase in net interest income from higher interest rates, if achieved and sustained, should improve the bank's operating leverage and raise its profitability on a sustainable basis, strengthening the bank's credit profile," the ratings agency said in a recent assessment of Bank of America.

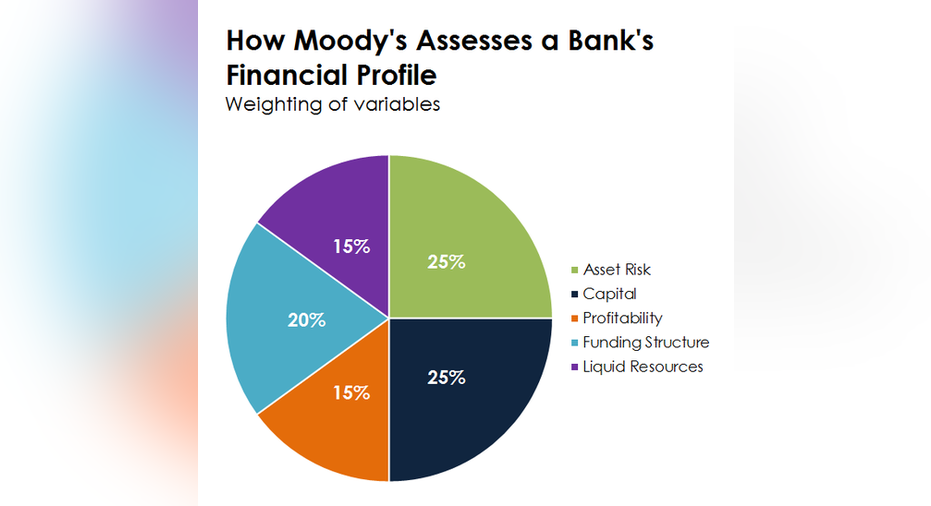

This assessment tracks Moody's ratings methodology for banks, which is dictated by macroeconomic factors, a bank's unique financial profile, and qualitative adjustments. Within a bank's financial profile, moreover, Moody's balances five factors based on specific weightings: asset risk (25%), capital (25%), profitability (15%), funding structure (20%), and liquid resources (15%).

Data source: Moody's. Chart by author.

Given that Bank of America holds an abundance of excess capital and liquidity, as I've discussed in the past, it makes sense that Moody's (and presumably the other ratings agencies) has zeroed in on the bank's profitability as the main hurdle between it and higher ratings.

This is an auspicious sign for Bank of America given that its profitability is improving, becoming more predictable, and should continue to grow in the years ahead. It earned more money last year, for instance, than in any other year in its history, with the exception of 2006.

The result for current and prospective investors in Bank of America is that its continued recovery will not only impact the bank's bottom line directly, through higher revenues and lower expenses, but also indirectly, as higher debt ratings in the future should eventually reflect this improvement and thereby translate into lower borrowing costs.

10 stocks we like better than Bank of AmericaWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Bank of America wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of April 3, 2017

John Maxfield owns shares of Bank of America. The Motley Fool owns shares of and recommends Moody's. The Motley Fool has a disclosure policy.