How Tesla Can Fix Its Flawed Solar Business

Tesla's (NASDAQ: TSLA) acquisition of SolarCity was touted as a way to vertically integrate the EV company into a one-stop renewable energy provider for customers. Walk in a Tesla retail store, and you can walk out with an electric car run on electricity from your roof that was stored all day in your Powerwall.

The reality of solar in 2017 is that SolarCity's business model is dying. The lease/power purchase agreement (PPA) that made SolarCity so popular in the first place is being replaced by loan and cash sales, which are better served by smaller installers. Sales are becoming harder as the low-hanging fruit has already been nabbed by a highly competitive industry. The old SolarCity isn't what it used to be.

What's interesting are the new solar products that SolarCity started working on, and Tesla is finishing. The solar manufacturing plant that's supposed to build high-efficiency solar panels in Buffalo, New York, and the new solar roof product, which will eventually pair with the Powerwall to create a holistic energy solution are a path forward for Tesla. But the installation and sales wings of the solar business have become a weight Tesla should no longer be willing to hold.

Tesla's solar roof is a big product coming in 2017. Image source: Tesla.

Tesla should cut thousands of jobs

This sounds dramatic, but don't worry, there's still lots of work for people to do installing Tesla solar systems. However, maybe it doesn't make sense for them to do that work under Tesla's umbrella.

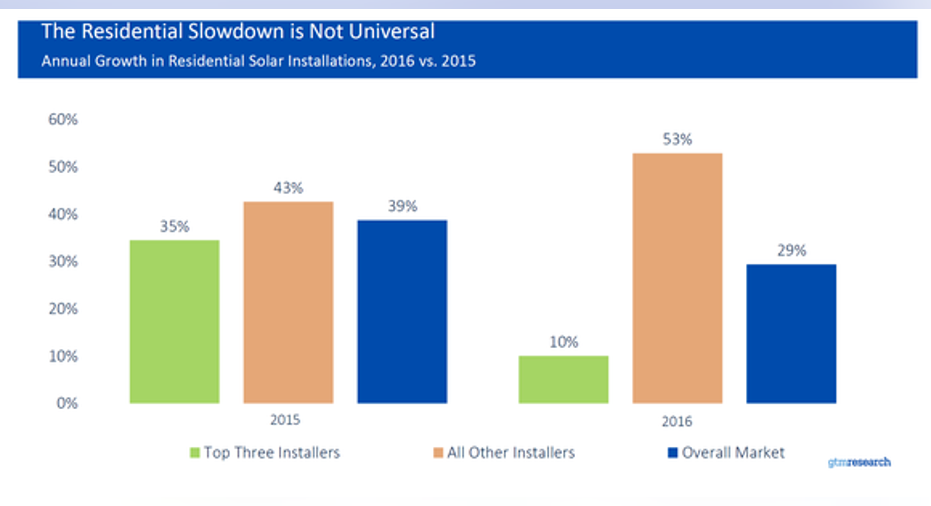

When SolarCity built out its solar business, it put most of its work into building out a sales force that could sell solar systems and an installation force that could put them up. The large, national solar model was working and did until the end of 2015. But, according to GTM Research, the top three solar installers in the country grew at just 10% in 2016 while all other installers grew 53%. Tesla/SolarCity's decline is even more pronounced with deployments falling from 253 MW in Q4 2015 to 201 MW in Q4 2016.

Image source: GTM Research.

This isn't necessarily a problem because Tesla would like to automate the sales process, or move it into Tesla's stores. So, it makes sense for fewer for Tesla workers to be selling door-to-door the way SolarCity did.

On the installation side, Tesla could offload work to hundreds of contracting partners the do the actual installation work rather than having the team in-house. Owning the installation side of the business means Tesla is taking on the operating costs of hiring workers and buying installation equipment, and it has to constantly keep those workers busy. If this work was contracted out, it would lower risk and potentially lower costs as contractors compete for business.

This wouldn't be a novel approach. Most of the construction business works on this contractor model, whether it's building a home or replacing a roof or a kitchen. And with small solar installers taking market share from Tesla, it would be wise for it to lower its operating risk.

The Powerwall could be the center of a new solar strategy at Tesla. Image source: Tesla.

Create a pre-engineered solution that can scale

If Tesla moved to a business model that contracted out work, it would need to create an easy-to-install solution for contractors. And that is already on the waywith the development of the Powerwall and the solar panels made in-house. Soon, Tesla will be more vertically integrated than any other full service solar company (including energy storage) so the company could offer a suite of solutions few companies could even dream of matching.

Gigafactory 2, the Buffalo solar plant, will soon be making solar panels, and Tesla now owns the racking company for solar systems. These products could be pre-engineered into a solution that would be sold to smaller contractors. Even the Powerwall would fit into this model, and Tesla could provide services to be the brains behind making the Powerwall economically viable.

The Solar Roof could be another extension of this model, a product that could be sold through contractors without having to train in-house installers on the product.

Creating a pre-engineered solution for contractors could create a highly scalable business for Tesla, which would potentially lead to a bigger solar footprint overall, which is Musk's goal, after all.

Ditch the solar lease

If Tesla is serious about turning the solar business into a cash-flow business, it should eliminate the lease, or power purchase agreement. This would be turning its back on the financing model that made SolarCity popular, but the lease is losing market share rapidly, and it's not a product Tesla wants to have on its balance sheet anyway.

Lease financing has become unattractive over time because SolarCity's borrowing costs were rising. Without low borrowing costs the lease has no advantage over a loan and with loan rates on the decline there no reason to keep the lease in the portfolio.

If Tesla moved to a contractor model for installations, it could offload the financing of solar systems to third-party banks, who are already entering the market, and count on cash up front with each sale. This way, management and investors could judge the solar business on its margins and cash-flow generation rather than a questionable metric like retained value.

Tesla would be better with a more focused solar business

If Elon Musk wants to create a successful solar business long term, he should de-risk the business by getting out of installation and high-intensity sales. Instead, focusing the company on making great products and providing the services contractors need to sell them would be a move in the right direction. Investors would likely cheer the move.

10 stocks we like better than TeslaWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now...and Tesla wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017.

Travis Hoium has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Tesla. The Motley Fool has a disclosure policy.