How Risky Is InvenSense Inc. Stock?

Image Source: Getty.

The past two years haven't been kind to InvenSense (NYSE: INVN), which makes motion sensors for smartphones, tablets, wearables, and other devices. Back in Aug. 2014, the stock peaked at $25 on surging sales and expectations that its sensors would be installed in the Apple (NASDAQ: AAPL) Watch.

But Apple eventually chose STMicroelectronics' (NYSE: STM) motion sensors for the Apple Watch, and slumping smartphone and tablet sales caused InvenSense's growth to hit a brick wall. As a result, the stock plunged to about $8 per share over the past two years. But after that steep drop, which brings the stock near its IPO price of $7.50 per share, can the fallen supplier be considered a contrarian buy? Let's examine InvenSense's growth, valuations, cash flow, and competition to decide.

Image source: InvenSense.

How fast is InvenSense growing?

InvenSense's revenue rose 12% to$418.4 million last year, compared to 47% growth in fiscal 2015. Last year, 40% ofInvenSense's revenue came from Apple, while 16% came from Samsung. This means that Apple's ongoing decline of iPhone and iPad shipments are taking a huge bite out of InvenSense's top line.

InvenSense's revenue fell 43% annually last quarter, compared to a 20% decline in the previous quarter and 59% growth in the prior-year quarter. Sales of new smartphones, like the iPhone 7, are expected to boost its sales in the second half of the year, but not by much. Analysts still expect InvenSense's full-year revenue to fall 24% thisyear.

InvenSense's non-GAAP earnings rose 6.5% to $0.49 per share in 2015, but that figure is expected to plummet 76% this year. Increased competition from STMicro, which is much bigger and has its own foundry, could force InvenSense to slash prices to stay competitive.

Valuations and cash flow

To make matters worse, InvenSense's massive decline still hasn't made the stock cheap. It trades at 27 times forward earnings, which is much higher than STMicro's forward price-to-earnings ratio of 18. Moreover, STMicro is actually expected to grow its earnings by 11% this year, while InvenSense is headed toward a full-year decline.

InvenSense currently trades with a five-year price-to-earnings-growth (PEG) ratio of 3.3, while STMicro has a PEG ratio of 0.7. Since a PEG ratio under 1 is considered "undervalued," InvenSense looks pricey relative to its earnings growth potential, while STMicro looks cheap. InvenSense also trades with a price-to-sales ratio of 2, which is double STMicro's P/S ratio of 1.

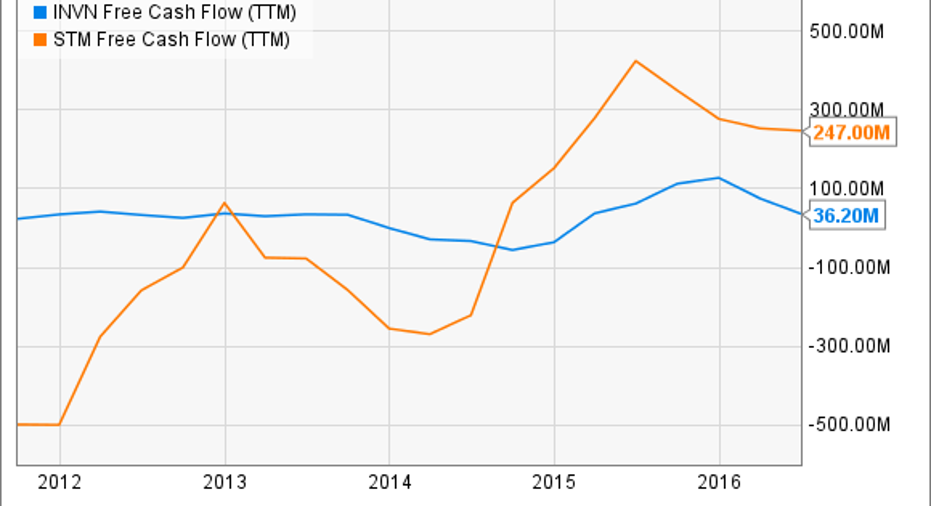

InvenSense is burning through a lot of cash. Its cash and equivalents fell 44% sequentially to $23 million last quarter. STMicro's cash pile, by comparison, stayed nearly flat sequentially at $1.68 billion last quarter. Therefore, it isn't surprising that STMicro has generated much stronger cash flows than InvenSense over the past five years. That's why STMicro pays a forward annual yield of 3.1%, while InvenSense has never paid a dividend.

Data source:YCharts.

Competitive threats and potential catalysts

The biggest threat to InvenSense is STMicro. The chipmaker already pulled the Apple Watch away from InvenSense, and might do the same in iPhones and iPads in the future if it offers comparable sensors at lower prices. As fierce competition puts further pressure on smartphone margins, plenty of other OEMs could do the same.

InvenSense's main response to these threats is to diversify into new markets like virtual and augmented reality headsets, drones, cars, Internet of Things devices, and industrial machines. Unfortunately, STMicro is alsoexpanding into many of the same markets. FurthermoreBosch is becoming a major player in VR headsets. The company's six- and nine-axis sensors are already used inFacebook'sOculus Rift andRazer's HDK 2 VR headsets. InvenSense's six-axis sensor canbe found inside HTC's Vive, which is pricier than both headsets.

InvenSense is too risky to touch

InvenSense's plunging sales and earnings, weak cash flow, unattractive valuations, lack of competitive advantages, and its dependence on Apple make the stock too risky for investors. Investors who are looking for a stable play on gyroscopes and accelerometers should simply stick with STMicro instead.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Leo Sun has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Apple, Facebook, and InvenSense. The Motley Fool has the following options: long January 2018 $90 calls on Apple and short January 2018 $95 calls on Apple. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.