How Is Illinois Tool Works Stock Positioned for 2016?

During its recent investor and analyst day, reiterated its performance goals for 2017. Its management has set its targets as the fruition of a five-year enterprise strategy plan intended to increase margin and revenue growth. Let's look at the analyst day presentation in the context of making a decision to buy the stock or not.

The company's enterprise plan means the stock offers self-help growth opportunities -- not a bad quality in a sluggish economy -- but ultimately its fortunes are still tied to the industrial economy. The question is whether the former is enough to offset any difficulties with the latter in 2016.

The negative case notes the weakness in segments exposed to weak areas of the global economy. It's obviously not a coincidence and speaks to the headwinds the company faces in executing its plans. For example, a review of its recent results highlights margin and organic growth deterioration in three of its seven segments -- Test & Measurement and Electronics, Welding, and Polymers & Fluids. This is relevant for two reasons.

First, all three are areas of weakness in the global economy, indicating that the company simply can't evade economic pressures. Results elsewhere confirm this trend. For example, (NYSE: MMM) recently reported revenue weakness in its industrial and electronics and energy segments even while margins expanded across the board. In common with Illinois Tool Works, 3M reported stronger results in noncyclical areas such as healthcare, while its strongest segment was its consumer-facing segment.

Second, a look at segmental margin expansion since 2012, when the plan started, outlines Illinois Tool Works' increasing reliance on growth in its Automotive, Construction, and Food Equipment sections -- all representing relatively strong areas of the global economy.

SOURCE: ILLINOIS TOOL WORKS PRESENTATIONS. 100 BASIS POINTS EQUAL 1%.

In short, the more cyclically exposed areas, such as, say, Test & Measurement and Electronics and Welding, have found margin expansion a lot harder to generate -- a sign that the economy is playing a large role in guiding the company's prospects.

On the other hand, there are three key reasons to be positive on thestock.First, management affirmed these key 2017 targets:

- 23% operating margin

- 20%-plus after-tax return on invested capital

- 200-basis-point revenue growth above global GDP

- 12% to 14% total shareholder returns.

In response to fears about its exposure to global growth, management outlined its "business resilience" in modelling its estimate that even 1% growth in global GDP would still produce 8% to 10% total shareholder returns in the long term.

Second, management argued that 60% of its revenue comes from consumer-facing businesses, and the general theme of the most recent earnings season was that consumer-facing was good, and business-facing was bad.

Third, a large part of the presentation focused on how the company was still in the middle of transitioning its business toward growth. For example, by the end of 2015 the company expects 60% of segment revenueto be what it calls "ready to grow," with the remaining 40% labeled as "preparing for growth." Following continuing implementation of its strategy, the "ready to grow" portion of revenue is expected to increase to 85% by the end of 2016. In other words, Illinois Tool Works still has substantial growth to come from its internal initiatives.

On balance, Illinois Tool Works is an attractive proposition, but rather like 3M Company, it's hard to see a compelling case for value unless you have a lot of confidence that the company will hit its targets. Turning to Illinois Tool Works' near-term earnings and valuation, management gave guidance for EPS in the range of $5.35 to $5.55 for 2016, representing a nearly 7% increase from guidance for $5.05 to $5.15 in 2015 (midpoint to midpoint).

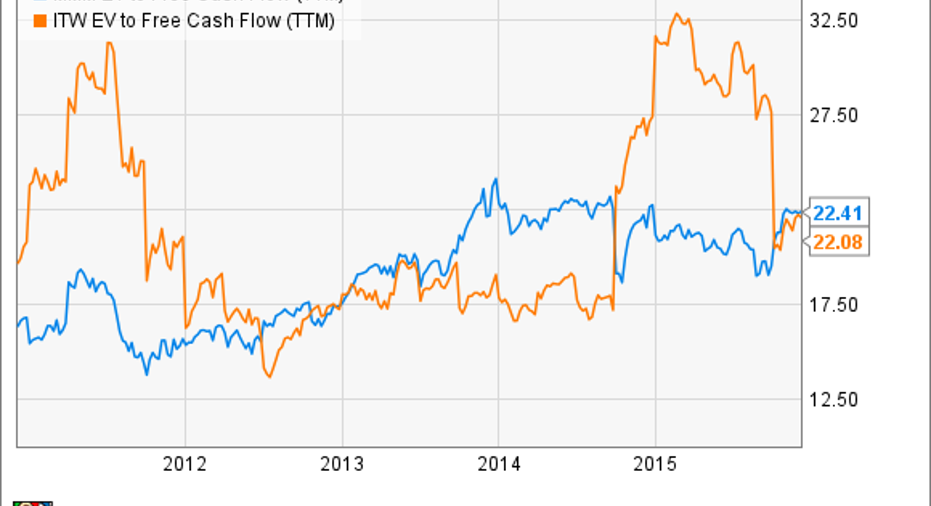

Assuming the company hits its target of converting 100% of net income into free cash flow means around $5.45 in free cash flow for 2016, which puts the stock on a forward enterprise value (market cap plus debt)-to-free cash flow multiple of around 19.5. At a current price of around $92, the stocklooks fairly valued on an EV-to-free cash flow basis:

MMM EV to Free Cash Flow (TTM) data by YCharts.

All told, the presentation strengthened the case for buying Illinois Tool Works. The company remains in transition mode, but the stock still doesn't look to be a good value on a risk/reward basis.

The article How Is Illinois Tool Works Stock Positioned for 2016? originally appeared on Fool.com.

Lee Samaha has no position in any stocks mentioned. The Motley Fool recommends Illinois Tool Works. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.