Home Depot Inc.'s 3 Biggest Growth Opportunities

Home Depot(NYSE: HD) added an impressive $13 billion to its annual sales base in the three years spanning 2013 to 2015. But the retailer isn't standing still on that result.

The home improvement giant aims to accomplish the same feat over the next three years, which would push it to over $100 billion of yearly revenue by the end of 2018. And it plans to do this while adding an insignificant number of stores to its base. Instead, it's focusing on a few major growth opportunities.

1. A rising tide for home improvement spending

The outlook for overall economic growth has slowed a bit over the last year, but the key factors supporting home improvement spending are as strong as ever. The industry has roughly doubled from the low it hit in the wake of the financial crisis, yet spending remains far below the $900 billion annual peak set in early 2006. At about 3.6% of GDP now, it is also well below the long-run average of 4.5%.

Annual spending on home improvement is still far below its 2006 peak. Image source: Federal Reserve Economic Data.

Other economic metrics also point to years of above-average growth ahead. Home prices are climbing but remain below peak levels they hit a decade ago, and the rate of new household formation is projected to be higher than the long-term average over the next three years. It's no wonder why rival Lowe's (NYSE: LOW) is forecasting faster growth thanks to a "favorable macroeconomic backdrop."

But if recent history is any guide, Home Depot is likely to grab more than its fair share of this growing industry. It doubled Lowe'sgrowth pace in the most recent quarter while extending its profitability and cash flow leads over its smaller competitor. Additional market share gains, even if they're slight, could translate into solid sales and earnings gains over the next few years.

2. Expanding the addressable market

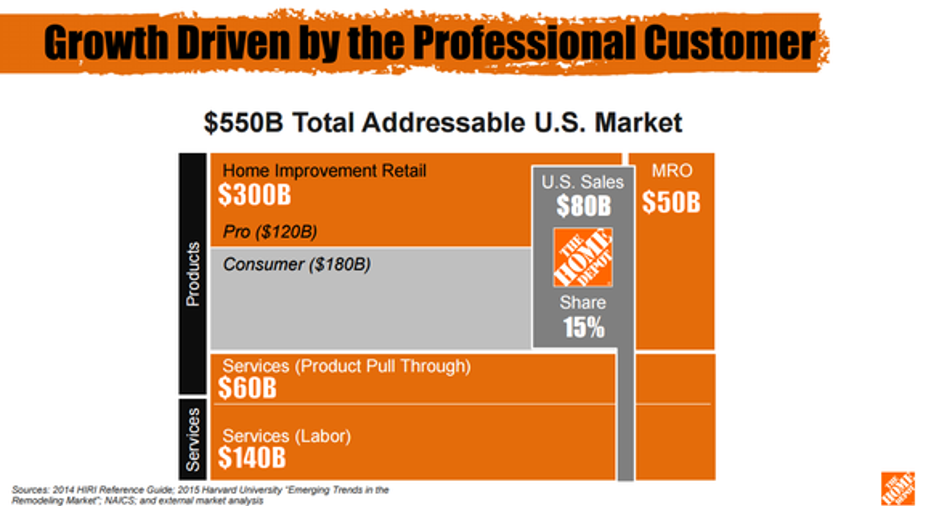

Home Depot dominates the consumer side of the home improvement market, but also sees significant growth opportunities in expanding its reach into the professional side of the business. That's a $120 billion industry right now, or not much smaller than the $180 billion consumer segment.

The retailer is already making major inroads at attracting contractors and small businesses. For example, its fastest-growing sales category is currently purchases above $900, which spiked higher by 8% last quarter.

MRO = Maintenance and retail and operations. Image source: Home Depot investor presentation.

CEO Craig Menear and his executive team plan to get additional sales boosts by pushing into the MRO (maintenance and repair and operations) segment with the help of Home Depot's recent Interline Brands acquisition.

3. Winning the online business

By now, all major brick-and-mortar retailers admit that a strong online presence is critical to the long-term health of their business. Yet Home Depot is doing a better job than most at actually integrating e-commerce into its selling approach. Online revenue spiked by 19% last quarter and now accounts for nearly 6% of sales. Compare that to Target, which calls digital sales "critically important" to the business. E-commerce is worth just 3% of that retailer's revenue.

Home Depot's online strategy involves a smart mix of dedicated fulfillment centers that complement shoppers' ability to order online and pick up products at one of its 2,200 warehouse locations. In fact, over 40% of its e-commerce orders last year ended with a visit to a physical store.

Home Depot aims to push the envelope further by rolling out its buy-online, ship-from-store functionality along with a few pro-specific options like next-day delivery of bulk goods. With continuous innovations like those, it's easy to see how Home Depot can keep its e-commerce sales outgrowing traditional retailing revenue for years.

These opportunities together suggest that not only sales will trek higher (the company targets roughly 4% comps in each of the next three fiscal years), but also that profitability will improve. Home Depot targets hitting a nearly 15% operating margin in 2018 and a 35% return on invested capital. Last year those figures were 13% and 28%, respectively.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Demitrios Kalogeropoulos owns shares of Home Depot. The Motley Fool recommends Home Depot. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.