Here's Why Golar LNG Partners LP Outperformed Its LNG Peers Last Month

Image source: Getty Images.

What happened

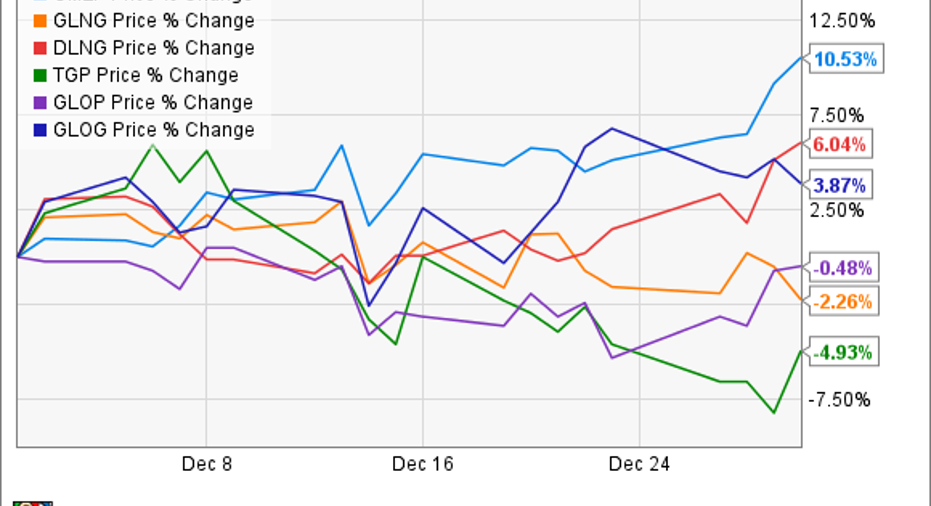

Units of Golar LNG Partners LP(NASDAQ: GMLP) climbed 10.5% in December, far and away the best gains across all the major master limited partnerships and companies involved in maritime transportation of liquefied natural gas:

So what

It was a strong finish to what turned out to be a fantastic year for Golar LNG Partners investors. The MLP's unit price finished 2016 up 83% for the full year and on what looked like pretty good news when it reported third-quarter results at the end of November.

Golar LNG Partners delivered steady cash flow and strong operating results, reporting net income of $56 million and operating income of $71.6 million. Management also announced thatGolar LNG Limited (USA)(NASDAQ: GLNG), its general partner, had agreed to rework its incentive distribution rights -- that is, its share of cash flows based on certain performance criteria -- in order to better position Golar LNG Partners' costs of equity. This move comes at the cost of more common units being issued, as Golar LNG Limited will gain an increased stake in common units in exchange for changes to its incentive distribution rights.

Now what

On the surface, this dilution may sound like a bad deal for investors, but it's probably a net good, since it better aligns Golar LNG Limited's potential returns with those of smaller investors. A significant amount of its potential new common equity stake is tied to Golar LNG Partners being able to achieve certain payout levels to investors over the next two years, which is very much aligned with shareholders -- unless management uses debt or some other non-operational source of cash to increase payouts artificially. But, frankly, that's probably not likely, and would not be in the best long-term interest for either Golar LNG Partners or for Golar LNG Limited.

But even with the strong results and potentially better-aligned incentives, Golar LNG Partners isn't risk-free, as its more than 10% dividend yield should make clear. The biggest risk is a cash flow shortfall later this year, with three of its LNG carrier vessels scheduled to come off contract at the end of this year. If the company has trouble establishing new long-term work for its fleet, there is likely to be plenty of short-term work to be had, but also the risk of idle periods costing huge amounts of cash, as these vessels must still be maintained in between work.

Bottom line: There's a lot of potential long-term upside as LNG demand continues to grow, but don't ignore the very real risk that cash flows would get hammered within a year if the company can't lock in new work. There's plenty of time for management to get it done, but that's also plenty of time for investors to lose a lot of money if the work isn't there. Just look back to 2015, when Golar LNG Partners' share price fell by 58% as evidence of how this could work out if you're not willing to ride things out or patient enough to hold for more than a year.

10 stocks we like better than Golar LNG Partners Partnership When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Golar LNG Partners Partnership wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Jason Hall has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.