Here's Why Bank of America's Stock Has a Lot of Room to Run

Bank of America's stock has climbed consistently over the last few weeks, but it's my opinion that it still has a lot of room to run. You can see this by tracing through its current valuation, improving profitability, and the impact of higher interest rates on both.

It's important to recognize that Bank of America's stock is incredibly cheap right now. I've made this point countless times in the past and continue to believe it's true.

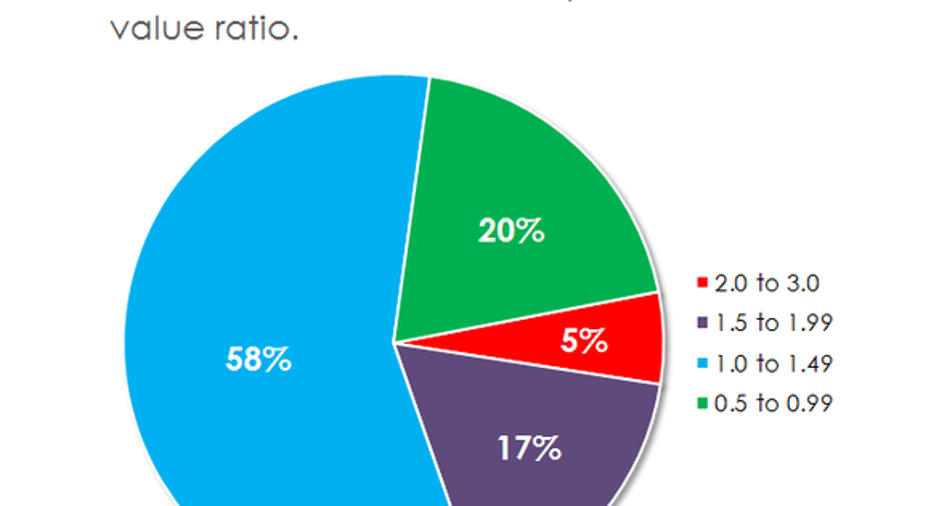

This is evident when you look at Bank of America's price-to-book value ratio. This compares a bank's stock price to its book value per share, and is calculated by dividing the former by the latter. The higher the number, the higher the valuation, and vice versa.

Most bank stocks trade for between one and two times book value. Anything outside of this should attract an investor's attention. Stocks that trade far in excess of two times book value likely don't have much room to run in the short term. But stocks that trade for less than one times book value are in the opposite position.

Data source: YCharts.com. Chart by author.

In Bank of America's case, it trades for a 37% discount to its book value. It's hard to express how inexpensive this is -- as a valuation this low is more commonly associated with a bank that's deeply ensconced in crisis.

The main reason Bank of America's shares are so cheap is because its profitability is abysmal. The bank earned $15.9 billion last year. That equates to a return on assets of 0.74%, which is well below the 1% return on assets threshold that Bank of America has set as its target.

Things were even worse in the first quarter of this year. Thanks largely to lower trading and investment banking revenues, Bank of America generated a return on assets of only 0.5%.

What's important to appreciate, however, is that Bank of America's profit is rapidly improving, despite its setback in the first three months of this year. The year 2015 marked the first time since the financial crisis that it's earned a semi-respectable profit in all four calendar quarters.

Data source: Bank of America. Chart by author.

There's every reason to believe that this could be the beginning of a string of improved quarterly and annual earnings. In the first case, Bank of America is now largely done with the oppressive legal costs it incurred as a result of the crisis. All told, they added up to $65 billion since 2010.

In the second case, Bank of America, like most other banks, is primed to benefit from higher interest rates. It estimates that it will earn $6 billion more in annual net interest income if short- and long-term rates increase simultaneously by 100 basis points, or 1%. And if interest rates revert to 2002 levels, then it could earn as much as $20 billion more a year in after-tax income, holding all else equal.

The point is this: Bank of America's shares still seem to have a lot of room to run. It's anybody's guess when they'll head meaningfully higher, but owning its stock now will allow your portfolio to benefit from this trend if/when it materializes.

The article Here's Why Bank of America's Stock Has a Lot of Room to Run originally appeared on Fool.com.

John Maxfield owns shares of Bank of America. The Motley Fool recommends Bank of America. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.