Heres How to Get the Maximum Social Security Benefit

SOURCE: PIXABAY

I won't keep you in suspense: The maximum Social Security Benefit is $3,576 per month in 2016, but don't get too excited yet. Social Security payments are determined by a combination of your Social Security wages over 35 years and the age you take Social Security (those who wait until age 70 to file receive more benefits). I'll get into the math below, so read on to find out how Social Security estimates your retirement benefit, and for tips on what you can do now to increase your future Social Security payments.

How much will you get?Social Security is meant to be a safety net for retirees and therefore, it typically replaces about 40% of a workers pre-retirement income.

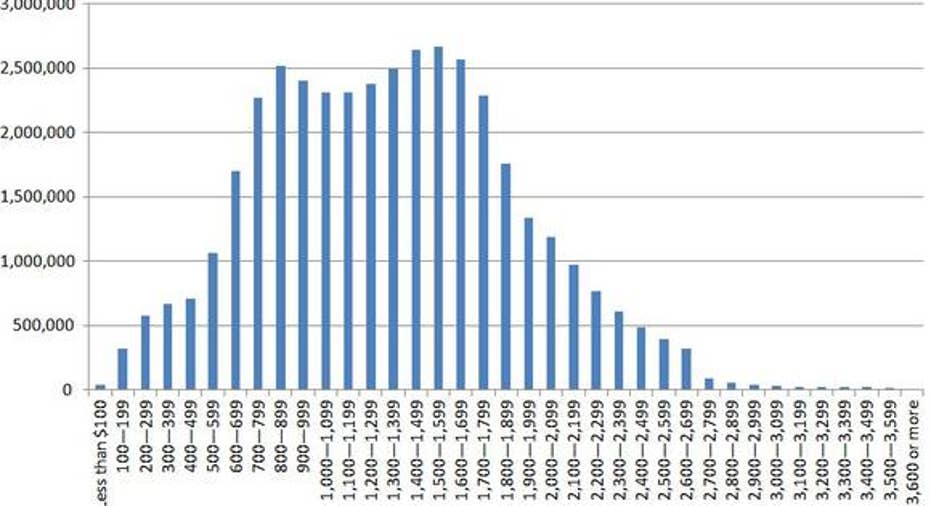

In 2016, the average Social Security benefit paid to retired workers is $1,341 per month. However, the amount of money each retired worker receives in Social Security benefits varies widely. As you can see in the following chart, most people receive between $700 and $1,800 in Social Security income per month.

SOURCE: SOCIAL SECURITY ADMINISTRATION

In order to qualify to receive a Social Security benefit in retirement, you must accumulate 40 credits, which works out to about 10 years of work. Once you qualify, Social Security calculates your maximum benefit using a complex formula.

First, your income history -- up to specific limits -- is adjusted into current dollars. Then, the highest 35 years of adjusted income are totaled and divided by 420, which is the number of months in 35 years. The result is a person's average monthly indexed earnings. Once that's done, multipliers are applied to specific intervals of a person's average monthly indexed earnings to calculate the maximum Social Security benefit at full retirement age.

For example, someone born in or after 1954 would multiply the first $856 in indexed monthly earnings by 90%, any amount between $856 and $5,157 by 32%, and any amount above $5,157 by 15%. The resulting numbers are then added together and rounded down to the nearest dollar to get Social Security's estimated monthly retirement benefit at full retirement age.

SOURCE: FLICKR USER SENIORLIVING.ORG

How to get the biggest benefitObviously, the more income you earn, the bigger benefit you'll receive in retirement. The payroll tax that pays for Social Security is applied to income up to $118,500 in 2016, so if income is below that amount, increasing it may be the best way to net a bigger check in retirement.

If you've already accumulated a 35 year work history, delaying retirement by a couple more years could increase your benefit too. That's because high-income-earning years displace low-income-earning years when Social Security picks the top 35 earning years to run its retirement benefit calculation.

Additionally, delaying enrollment in Social Security can also result in a bigger benefit payment. Full retirement age is currently 66 (67 for people born after 1960), yet many people enroll in Social Security at age 62, the earliest age possible. Obviously, everyone's situation is different, and there can be benefits to taking Social Security early, however, enrolling at 62 can result in a monthly benefit payment that's 25% less than what you'd receive at full retirement age.

Alternatively, enrolling in Social Security at age 70 can substantially increase your Social Security income. For example, if you were born in 1960 or later, and you delay enrolling in Social Security until you reach age 70, then you would receive a Social Security benefit that's 124% of the amount you'd receive at full retirement age. That might not get you to the maximum Social Security benefit, but it could get you close.

The article Heres How to Get the Maximum Social Security Benefit originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.