Here's How to Get Completely Tax-Free Early-Retirement Income

Image source: Getty Images.

If you're reading this, then I congratulate you. To even consider early retirement, you need to know the value of figuring outhow much money you need to be happy,spending less than you earn, and investing the difference. The problem, however, is that once you save up enough money in a tax-advantaged retirement account, you have to wait until you're nearly 60 to start withdrawing that money tax-free.

Well, I have good news for you. If you've learned to live a frugal life, then there's something even better than a Roth IRA, and it's been hiding under our noses all along: a plain old brokerage account -- with absolutely no tax advantages to speak of.

Did you ever notice this before considering early retirement?

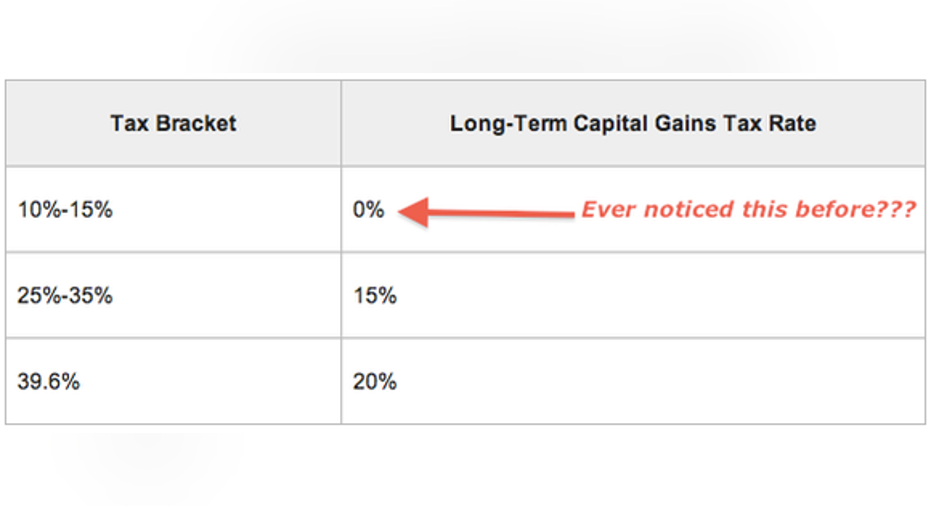

In 2014, I was doing some research on capital gains taxes when I noticed something I'd never seen before:

I was astounded. If -- after adding together all of your sources of income -- your household is in or below the 15% tax bracket, you pay absolutely no taxes on capital gains. "Sure," you might say, "but only the uber-poor are in those tax brackets."

That's not quite true. Here's the adjusted gross income limit that would put you in that tax bracket.

Data source: The Tax Foundation.

Consider how high these levels really are. The median household income in America sits at $55,500. If that household has a married couple filing jointly, they fall below the 15% tax threshold.

What this means for early retirees

Let's consider a couple that's 50 years old. They've been putting money away in their 401(k)s and traditional IRAs for their entire working lives. That has allowed them to build up a substantial nest egg -- say $600,000.

But because they lived a disciplined lifestyle that eschewed things like buying as much house as they could afford, driving brand-new cars, and sending their kids to the most expensive colleges on Earth, they can live comfortably on $40,000 per year now that the kids are gone.

The couple knows that once they are 62, they'll be able to have all of their needs met by a combination of Social Security and their nest egg. They'll also be able to start getting that money from retirement accounts starting at age 59-1/2 years old. They just need to bridge the gap between when they retire and when they can tap those sources of income.

They did this by investing any leftover money they had -- after contributing to their 401(k) and IRA -- in a regular brokerage account. They bought stocks of solid companies with durable competitive advantages and, in many cases, dividends. In some years they'd have to pay taxes on those dividends while they were working, but not in all years.

While the couple was well aware of the 4% rule for safe withdrawals, they were comfortable taking out 8% in the first year, given that they only needed their nest egg to last about a decade, rather than all of retirement. That means over the years they've built up a normal brokerage account worth $500,000.

Once they quit their jobs, they'll get the requisite $40,000 in annual income by collecting dividend payments and selling some stocks -- and they'll never pay taxes on any of it.

Practical applications for you and me

To be frank, some of these figures seem fantastical. I would love to believe that I'll have $600,000 in retirement accounts and another $500,000 in a brokerage account when I'm 50. But I probably won't find myself there -- and that's OK.

I still use this knowledge to my advantage. Every year, after our bills are paid, we contribute to a traditional IRA instead of a Roth. We prefer the tax reduction right now, because we know that any excess cash we might have can simply be put into a regular brokerage account that's as good as a Roth, so long as we keep an eye on how much we're earning and when we sell certain stocks.

If you have the time, this is an easy approach that will give you much more flexibility when early retirement comes knocking at your door.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.