Halliburton Shows Off Its Shale-Drilling Dominance in Q1 Earnings

Halliburton (NYSE: HAL) is well-known for owning a lion's share of the North American shale drilling market, and its most recent earnings release was further proof. While its largest competitor showed single-digit growth in North America, Halliburton realized a 24% gain in revenue.As great as that sounds, there were some consequences to those revenue gains.

Here's a quick rundown of the oil service company's most recent quarterly results and why management decided to shoot for rapid revenue growth in this particular quarter, as well as what this could mean for the rest of 2017.

Image source: Getty Images.

By the numbers

| Metric | Q1 2017 | Q4 2016 | Q1 2016 |

|---|---|---|---|

| Revenue | $4,279 million | $4,021 million | $4,198 million |

| Operating income | $203 million | $53 million | ($3,079 million) |

| EPS | ($0.04) | ($0.17) | ($2.81) |

| Free cash flow | ($232 million) | $871 million | ($379 million) |

Data source: Halliburton earnings release.

Halliburton's results this past quarter were the perfect encapsulation of the major trends we are seeing in the oil and gas market today. The company realizedhigher revenue on a sequential and year-over-year basis. The driving factor for those gains was its North American shale operations. Even though revenue in Halliburton's international business segments declined 8%, it was more than offset by a 24% increase in revenue in North America. Oil prices in the $50-a-barrel range have been enough for several oil producers in the U.S. to head back into the shale patch, but it isn't enough to incentivize international players to go back to work (whether that is because it's more expensive to drill internationally or if shale producers don't care about positive cash flow is up for debate).

Perhaps the most discouraging component of these results, then, was the fact that those revenue gains didn't translate into positive earnings or free cash flow generation. Management, however, did give investors a heads-up last month that earnings were going to be lower this quarter because it anticipated higher-than-usual costs. Most of those higher costs related to bringing lots of its idle drilling and fracking equipment back online to meet growing demand. As we enter the second quarter, we should expect start-up costs to decline as some positive earnings numbers roll in.

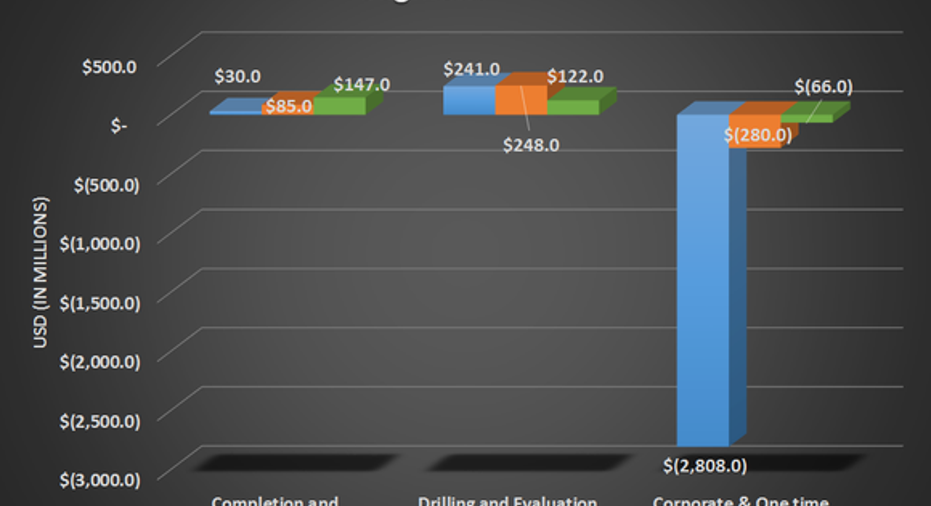

One thing that was a little bizarreis that the company stopped reporting operating income based on its geographic regions in its press release. None of the company's prior releases or conference calls indicated this will happen. So here's a look at how the company's operating income results broke down based on its different operating segments.

Data source: Halliburton earnings results. Chart by author.

As far as cash flows are concerned, the first quarter is typically a quarter where oil services companies have large capital builds for the year. Schlumberger's first-quarter results were similar in that it also took a lot of cash flow charges for the quarter. It's also worth mentioning that Halliburton paid a $335 million settlement charge related to the 2010Macondo well blowout.

What management had to say

After the company's operational update last month, there wasn't much to add to this quarter's press release aside from management highlighting the fast-growing North American shale market. To give an idea of how much the increased costs impacted profitability, though, we can look back at that operational update call where CEO Dave Lesar explained why the company was electing to put much more equipment back to work:

With Halliburton'slargest competitors combining their shale services into a joint venture to compete for market share and improve profitability, it's probably a good thing that the company makes some market-share preserving moves now to lock in customers to contracts rather than wait a little longer in hopes of signing on for higher rate of return contracts.

Investor takeaway

Halliburton is clearly trying to put pressure on its competitors by aiming to protect its market share in the first quarter, and that could actually have some far-reaching effects on the oil market in general. It may take a dent on profitability levels to bring so much equipment online, but it will also make North American shale production that much more economical and delay investment in other oil sources even more. Considering how much Halliburton relies on North America -- and how much its competition relies on markets outside North America -- this should make Halliburton's results look much better over the coming quarters.

10 stocks we like better than HalliburtonWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Halliburton wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of April 3, 2017

Tyler Crowe has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.