Forget Kinder Morgan, Buy These 3 MLPs Instead

Source: Spectra Energy Partners.

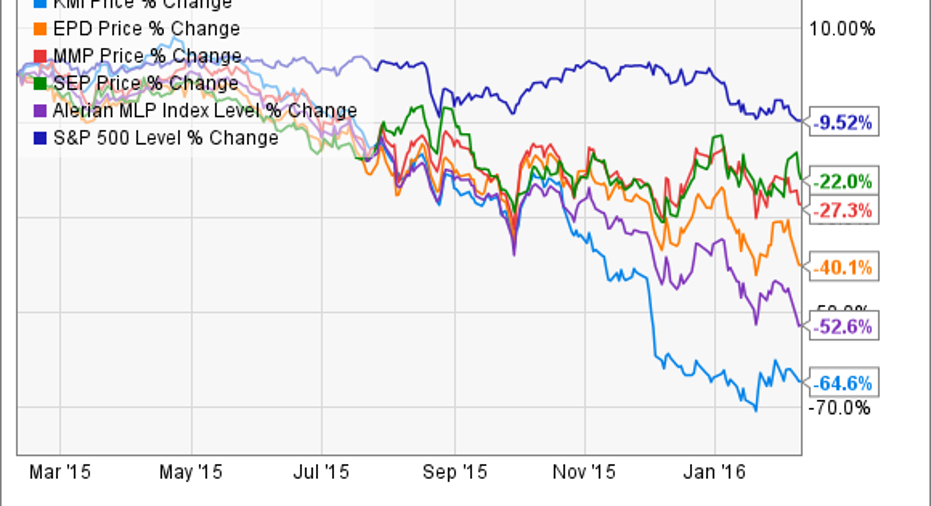

Kinder Morgan's (NYSE: KMI) recent 75% reduction of its dividend has meant a hellish year for dividend investors.

With shares having fallenfar worse than many of its blue chip midstream MLP peers such as Enterprise Products Partners (NYSE: EPD), Magellan Midstream Partners (NYSE: MMP), and Spectra Energy Partners (NYSE: SEP), value-hungry income investors may be considering opening or adding to their positions in America's fallen dividend darling. I think that's a bad idea, and Enterprise Products, Magellan Midstream, and Spectra Energy Partnersare all likely tomake far superior long-term income investments over the next five to 10 years. Here's why.

A rare case of higher quality and higher yield

| Company/MLP | Yield | 2015 Distribution Coverage Ratio | Payout Growth Guidance |

|---|---|---|---|

| Kinder Morgan | 3.4% | 4.2 | NA |

| Enterprise Products Partners | 7.8% | 1.3 | 5.2% in 2016 |

| Magellan Midstream Partners | 5.3% | 1.2 | 10% in 2016 "at least" 8% in 2017 |

| Spectra Energy Partners | 6% | 1.2 | 7.3% CAGR through 2018 |

Sources: earnings results, earnings presentations, guidance presentations.

Note that Kinder's 2015 coverage ratio takes into account the reduced dividend and Magellan's factors in 10% distribution growth that management is currently guiding for.

The point of owning midstream MLPs is for the distributions, and investors need to focus on three aspects of the payout: yield, long-term sustainability, and long-term, realistic growth prospects.

In this case, Kinder Morgan proves itself far inferior in all aspects to its peers, with a far lower yield and uncertain payout growth prospects. Even its enormous coverage ratio, while technically representing $3.6 billion in excess DCF, once the 2016 dividend is factored in, isn't that impressive. This is because, unlike Enterprise, Magellan, and Spectra Energy Partners, Kinder has no way to fund its capital spending nor pay down its enormous debt except with excess DCF, meaning its financial flexibility to do things such as raise the dividend in the short-term is far more limited than its peers.

Also keep in mind that this projected excess DCF is based onpredicted average 2016 oil and gas prices that arealready proving overly optimistic. Should energy prices continue falling or even just remain at current prices, Kinder's excess DCF cushion will fall right along with them.

Superior payout growth guidance backed up by strong backlogs When it comes to long-term distribution growth, it's vital that investors not just take management's word for it but ask themselves, "Does this MLP have a large enough short-term to medium-term project backlog tosustainably grow the payout this quickly?"

Enterprise Products Partners, and Spectra Energy Partnersboth have stable or growing backlogsthat are sufficient to provide a growth catalyst that is likely to keep their payouts growing for many years to come. As for Magellan, while true that itsbacklog has gradually been shrinking in recent years,but the investments it does have coming online over the next few years are profitable enough that it should have no problem still growing its DCF despite low energy costs.

Kinder Morgan, on the other hand, has been forced to slash its once mighty $22 billion backlog by 17% or $3.8 billion in just the past six months.

Management has said that it expects the backlog to continue shrinking as it focuses on onlyits most potentially profitable projects. Don't get me wrong -- this "high-grading" of Kinder's backlog is necessary because when it comes to profitability Kinder is once again woefully inferior compared to its blue chip peers.

Weak balance sheet and poor profitably

| Metric | Kinder Morgan | Enterprise Products Partners | Magellan Midstream Partners | Spectra Energy Partners |

|---|---|---|---|---|

| Debt/EBITDA (leverage) ratio | 5.6 | 4.5 | 2.9 | 3.6 |

| Operating income/interest (interest coverage) ratio | 1.28 | 3.68 | 7.2 | 5.33 |

| Average debt cost | 5.1% | 4.40% | 4.30% | 3.9% |

| Weighted average cost of capital (WACC) | 3.14% | 7.06% | 7.23% | 6.53% |

| Return on invested capital | 2.09% | 8.51% | 19.87% | 7.41% |

Sources: earnings releases, earnings presentations, Morningstar, GuruFocus.

Kinder Morgan's highly leveraged balance sheet, and the risk of a credit downgrade, was the primary cause of its dividend cut and share price crash.

Unfortunately, while management is working on reducing its leverage ratio with new projects coming online in 2016, Kinder expects its leverage ratio at the end of 2016 to be nearly unchanged at 5.5.

This high debt load means thatservicing its debt is more difficult and expensive. Also, it runs the risk that refinancing its existing debt will only grow in the future. This would further increase its cost of capital, which could further harm its ability to grow profitably.

In comparison, Enterprise, Magellan, and Spectra Energy Partners' leverage and interest coverage ratios exhibit clear signs of far more conservative use of debt in the past. This helps to keep their cost of capital low and allows positive return on new investment that is likely to mean continued cash flow and payout growth for the foreseeable future.

Bottom lineKinder Morgan may finally be on the right track when it comes to growing in a world of low energy prices, and by no means should investors that already own Kinder Morgan go looking elsewhere for their dividend checks.

However, when it comes to investing new money, Kinder's lower yield, poorer long-term growth prospects, much weaker balance sheet, and far worse profitability mean that long-term dividend investors might want to look at Enterprise Products Partners, Magellan Midstream, and Spectra Energy Partners over Kinder at this time.

The article Forget Kinder Morgan, Buy These 3 MLPs Instead originally appeared on Fool.com.

Adam Galas has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Kinder Morgan. The Motley Fool recommends Enterprise Products Partners and Magellan Midstream Partners. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.