Forget Debt -- Tesla Motors Should Raise Equity Capital

Tesla's Fremont factory. Image source: Tesla.

Electric-auto maker Tesla Motors is now paving the way and setting investor expectations that it will likely need more capital in the near future. CEO Elon Musk is justifying the possibility to investors by pointing to blockbuster Model 3 demand, and the decision to aggressively accelerate the production plans for the forthcoming $35,000 electric vehicle.

If Tesla hopes to produce 500,000 cars in 2018, just two years away, it's going to need quite a bit of cash to fund that expansion. That includes not only manufacturing and tooling equipment, but customer support infrastructure (sales, service, and charging). Having an extra billion or two in the bank would go a long way. Under the prior plan to hit 500,000 by 2020, Tesla had felt confident that it would not need to raise external capital. But things have changed.

While Tesla has now garnered about $400 million in customer reservation deposits for Model 3, the company does not want to rely on that as a funding source. They are refundable, after all, even if they technically count as working capital for the time being. Note that most of these deposits were not included in the balance sheet data released yesterday since the quarter closed on the same day as the Model 3 unveiling and standard payment processing times pushed receipt into April.

But from a corporate finance perspective, Tesla now must choose whether it wants to raise equity capital or debt capital. As a shareholder, I'd vote for equity capital.

But at what cost?Equity capital and debt capital come with very different types of associated with costs. Equity capital is generally more expensive than debt capital, since equity investors take on a lot more risk than credit investors. Shareholders are also farther back in line in the event that a company comes under financial distress.

The cost of equity is the required rate of return that shareholders demand in order to continue holding the stock. This includes both dividends and capital appreciation. If a stock fails to deliver this required rate of return, investors will sell their shares. The tricky part is that cost of equity is an abstract concept, but more important, it's an implicit cost.

The cost of debt is a lot more straightforward: It's simply the interest that the company pays on its paper. Most debt instruments (other than zero coupon bonds) will have a specified coupon payment that is paid to credit investors. While debt is cheaper, it's more of an explicit cost.

All of this gets even more complicated if we consider convertible notes, though, which are bonds that can be converted into shares. Tesla does have convertible bonds outstanding in its capital structure, but the cost of those is a topic for another day.

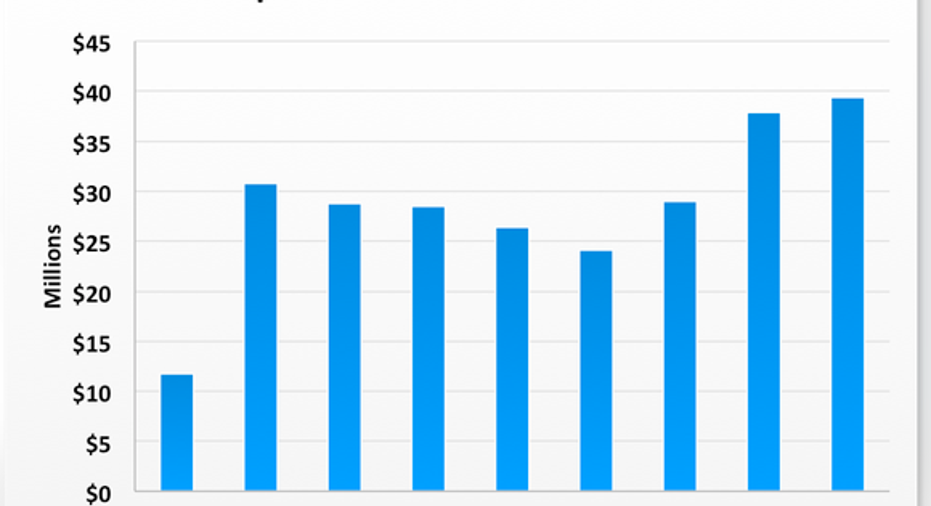

Enough is enoughI think that Tesla's current debt load is already quite meaningful ($3.1 billion in long-term debt and capital leases), so adding more debt to the equation adds more explicit financial pressure to Tesla's results, even if it's theoretically cheaper than equity capital.

Tesla has paid over $130 million in net interest expense over the past four quarters related to this debt.

Data source: SEC filings.

Normally, I'd look at interest expense as a percentage of operating income, but Tesla operates in the red, so that comparison isn't meaningful. Interest expense fluctuates between 2% and 4% of GAAP revenue. Tesla already pays enough interest expense, an explicit cost, while it could more easily issue more equity, an implicit cost.

With shares still fetching a lofty premium in the market, dilution (the cost to existing shareholders) would be rather minimal. It will be up to new CFO Jason Wheeler to make the call, but I hope he agrees.

The article Forget Debt -- Tesla Motors Should Raise Equity Capital originally appeared on Fool.com.

Evan Niu, CFA owns shares of Tesla Motors, andhas the following options: long January 2018 $180 calls on Tesla Motors. The Motley Fool owns shares of and recommends Tesla Motors. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.