For Illinois Tool Works, Another Impressive Quarter

Diversified industrial Illinois Tool Works (NYSE: ITW) is acquiring a reputation for underpromising and overdelivering, and the latest fourth-quarter results only served to strengthen it. Its peer 3M Co.recently affirmed full-year 2017 guidance, and Illinois Tool Works did the same. Despite the excitement around what Donald Trump's election victory could mean for U.S. industrial output, management claimed its segments remained pretty much on track -- which suggests there might be some upside to current guidance. Let's take a look at another solid quarter, and how the company is set for 2017.

Image source: Illinois Tool Works.

Illinois Tool Works' fourth quarter: The raw numbers

Starting with the headline numbers for the fourth quarter:

- Organic revenue growth of 2% came in at the high end of guidance of 0% to 2%.

- Operating margin of 23.8% compared to previous guidance of approximately 23.5%.

- GAAP EPS of $1.45 was ahead of previous guidance of $1.31 to $1.41.

In short, a pretty good quarter, and the company continued to expand operating margin despite moderately growing end markets. Turning to the full-year guidance, management merely reiterated the outlook given at its investor day presentation in December:

- Full-year organic sales growth of 1.5% to 3.5%

- Full-year GAAP EPS in the range of $6 to $6.20

- Full-year operating margin to exceed 23.5%

- Organic revenue growth of 1% to 2%

- First-quarter GAAP EPS in the range of $1.39 to $1.49

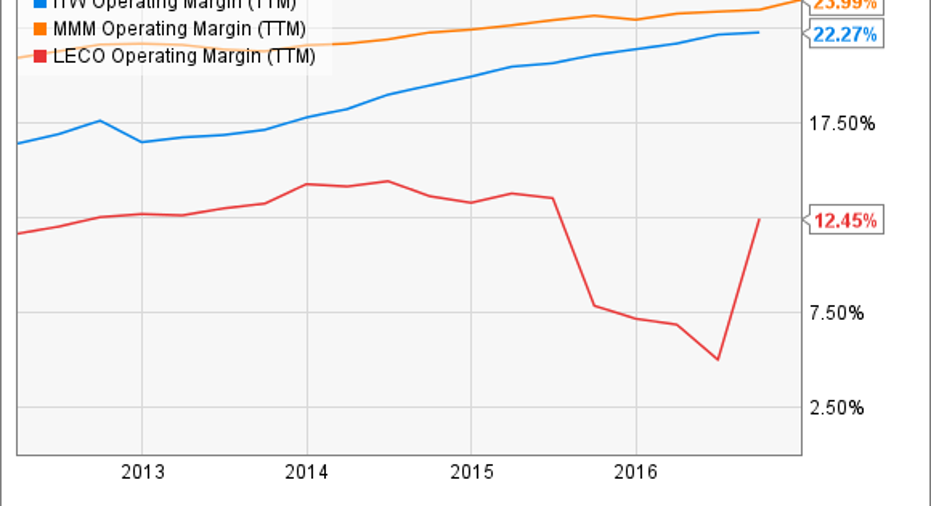

A pretty solid quarter of execution, and as you can see below, the full-year operating margin of 22.5% continues the company's excellent history of margin expansion.

ITW Operating Margin (TTM) data by YCharts.

2017 outlook discussion

Given the improvement in industrial markets noted by other companies in the current earnings season, analysts felt obliged to pepper Illinois Tool Works' management with questions relating to why the guidance range wasn't increased. It's a legitimate question because in the investor day presentation, management claimed that its guidance didn't include any assumption for a bounce in industrial or oil and gas markets (the troubled welding segment has heavy exposure to the latter).

Management's replies alluded to its plans being made based on the trends it was currently seeing. Moreover, they pointed out that the ongoing margin expansion is largely a consequence of internal actions taken that they call "enterprise initiatives" -- all the more attractive because margin expansion is not reliant on end-market growth.

Indeed, operating margin expanded 110 basis points (where 100 basis points equals 1%) in the fourth quarter, with enterprise initiatives contributing 130. In fact, if it hadn't been for the impact of the acquisition of EF&C, an engineering, fasteners and components business in the automotive sector, overall margin would have risen 150 basis points.As you can see below, all seven segments generated organic operating margin expansion and five of the seven generated revenue growth in the fourth quarter.

The strength in automotive OEM (original equipment manufacturing) is of particular note because it was stronger than auto builds in each reported region. For example, North America was up 2% compared to auto builds up 1%, Europe was up 8% compared to a 3% increase in auto builds, and China was up 33% compared to a 15% increase in builds. In other words, Illinois Tool Works is demonstrating it can outgrow its end markets. It's notable because some analysts are worried that global auto builds are set to plateau and possibly fall in 2017.

Data source: Illinois Tool Works presentations. Chart by author.

Looking ahead

All told, it was a good quarter for the company. Margin expansion is ongoing, and if the company can get some help from end markets, its management may yet raise earnings forecasts in the future. Recent industrial data has been encouraging, and there are early indications of oil-and-gas capital spending recovering, and if thistranslates into meaningful end-market improvement, then Illinois Tool Works' underlying margin expansion will bear fruit.

Meanwhile, the company continues to quietly beat expectations and investors continue to be rewarded, even as they wait for better end-market conditions.

10 stocks we like better than Illinois Tool Works When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Illinois Tool Works wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Lee Samaha has no position in any stocks mentioned. The Motley Fool recommends Illinois Tool Works. The Motley Fool has a disclosure policy.