FireEye Inc's Biggest Win in 2016 So Far

Image source: Getty Images.

FireEye (NASDAQ: FEYE) hasn't given its shareholders much to celebrate this year. Billings growth has disappointed both investors and management, leading the cybersecurity specialist to announce an executive shake-up aimed at getting the company back on track.

Yet there is one area where FireEye is significantly outperforming expectations: cost-cutting. Operating expenses have plunged as a percentage of revenue, and while net profits still seem far off, this improvement is critical for the business.

Two years ago, FireEye was spending far more than 100% of its revenue on operating expenses. The biggest piece of that was sales and marketing, which accounted for a whopping 80% of sales. Next up was research and development at 48%, followed by general and administrative costs at 22%. With the software specialist in a growth phase, it made sense that R&D and marketing would ring up such large balances, since they both (ideally) prime the pump for future billings gains.

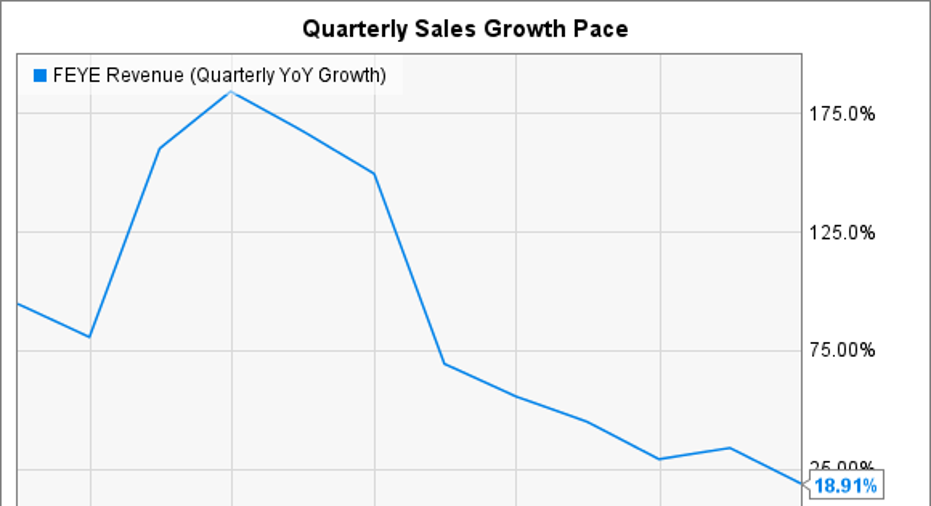

That spending isn't sustainable for long, though, certainly not while sales growth is decelerating. Back in 2014, FireEye was posting triple-digit gains in billings, but lately, the rate has been closer to 15% or 20%.

Data by YCharts.

Some of that decline can be attributed to the migration of customers from outright hardware purchases to subscriptions, but management is still not satisfied with the underlying growth pace.

The good news is that costs are falling at an even faster pace. Adjusted operating expenses decreased to roughly 100% of sales last quarter, down from 113% last year and 135% two years ago. The company's operating margin, while still deep in the red, improved from a 41% loss last year to 28%.

Sure, that's far from profitability, but it still marks FireEye's best performance on that measure since 2012. Management sees more room for cuts ahead, too. "We are taking additional measures in the third quarter to reduce our costs and align our operations with our growth," Chief Financial Officer Michael Berry told investors in early August.

The main risk FireEye faces is in balancing investments for long-term growth against the need for short-term savings. The most significant cost cuts, after all, have to come from marketing and sales spending, along with R&D. To some extent the company needs to trim its selling infrastructure and product development budgets to match the growth it is projecting, not the gains it was enjoying as recently as a year ago.

Skimp too much, or for too long, on these priorities, and you threaten your ability to compete effectively in the marketplace. Because FireEye uses an approach that's complementary to the traditional package of firewalls, gateway, and antivirus software, the company has to convince IT directors to make extra room in their security budgets for its products. That task becomes harder if the product isn't delivering broad results, or if the sales team can't effectively convey those benefits to potential customers.

It won't surprise investors to hear that FireEye's management believes it can execute around both of these sometimes competing initiatives of cost cuts and sales gains. "FireEyehas competitive advantages that will help reinvigorate our growth and deliver shareholder value in the future," new CEO Kevin Mandia said as he highlighted assets like its MVX threat detection architecture. "As we introduce the latest versions ofFireEyeproducts, improve sales execution, and continue to optimize our costs, I believe we will see steady improvement in our performance," he explained.

Steady worsening of sales growth trends is what shareholders have seen over the last few quarters. Yet FireEye has also provided good evidence on the expense side of the equation to support management's forecast of achieving non-GAAP profitably by the end of next year, even if the expansion pace continues to disappoint.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Demitrios Kalogeropoulos has no position in any stocks mentioned. The Motley Fool owns shares of and recommends FireEye. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.