FireEye Inc in 5 Charts

Image source: FireEye.

It hasn't been a great year to be a FireEye (NASDAQ: FEYE) shareholder.

Year-to-date, shares of the cyber security firm have lost nearly 30% of their value. A steady stream of disappointing earnings reports has taken a toll. Earlier this month, FireEye shares tumbled after the company turned in a poor second quarter. The business is growing, but not nearly as fast as analysts had anticipated.

But there's more to FireEye's business than disappointing revenue growth and curtailed guidance. The following five charts serve as a snapshot of the trends affecting FireEye's business.

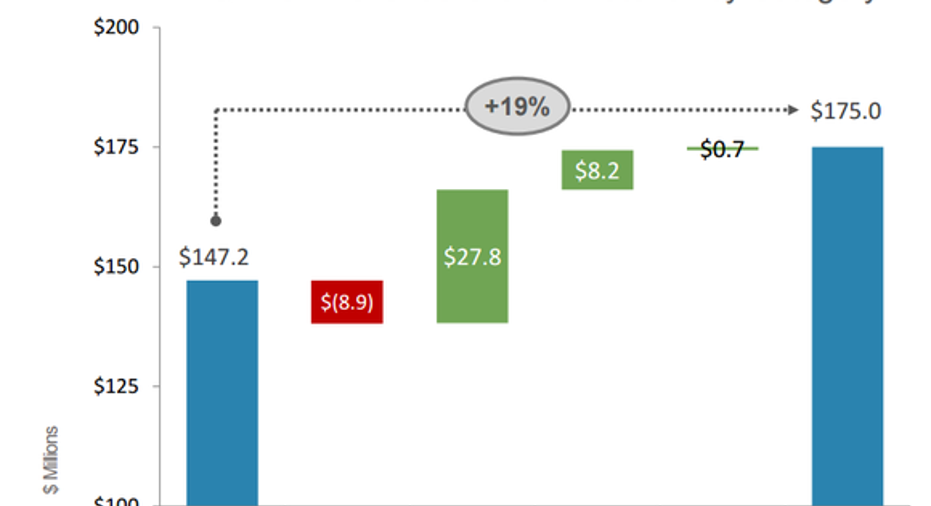

A closer look at FireEye's sales growth

Image source: FireEye.

FireEye isn't profitable, nor does it expect to be anytime in the near future. Investors interested in the company have overlooked this blemish, instead focusing on FireEye's (until recently) rapidly growing sales. Last quarter, FireEye's billings rose by only 10% on an annual basis, while its revenue increased 19%. As FireEye's revenue growth has slowed, subscriptions have generated a larger share of FireEye's revenue, while product revenue has receded in importance.

Breaking down FireEye's billings by category

Image source:FireEye.

This chart provides a closer look at FireEye's billings, an adjusted metric that includes subscription services FireEye has billed to its customers but not yet recorded as revenue. Although product-related billings fell $8.8 million on an annual basis, the gain in product subscription billings, and to a lesser extent support and professional services, was more than enough to offset the decline.

Breaking down FireEye's revenue by category

Image source:FireEye.

The same was largely true for FireEye's revenue. Product subscriptions enjoyed a large gain, more than enough to offset falling demand for FireEye's hardware products. FireEye's management has been cognizant of this shift for some time, and has spoken about the subject repeatably in earnings calls. Traditionally, FireEye derived much of its revenue from the sale of physical appliances (categorized here as Product), but in recent years, the company has introduced new offerings, such as FireEye-as-a-Service, that don't require the purchase of physical hardware.

Tracking FireEye's expenses

Image source:FireEye.

FireEye hopes to be profitable on an adjusted basis by the fourth quarter of 2017. To get there, the company has undertaken a restructuring, shedding workers to reduce its expenses. FireEye believes the restructuring will reduce its annual costs by at least $80 million. That should show up in future quarters. But even before that adjustment, the company's expenses had been improving. In the second quarter, the company's operating expenses were roughly equal with its revenue -- a notable improvement from the second quarter in 2015 and 2014. Notably, sales and marketing costs contracted from 80% of revenue in the second quarter of 2014 to just 57% last quarter.

FireEye is nearing break-even on an adjusted basis

Image source:FireEye.

This chart provides a broader view of FireEye's path to profitability. FireEye's expenses as a percentage of revenue have been trending down for most of the last two years. This is a positive trend, as it suggests that FireEye could succeed in achieving its profitability targets.

FireEye has never been a value stock, but with its growth slowing so dramatically, investors betting on the firm may expect the company to get on a sustainable operating path at some point in the near future. If this trend continues, FireEye could succeed in achieving some semblance of profitability by next year.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Sam Mattera has no position in any stocks mentioned. The Motley Fool owns shares of and recommends FireEye. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.