Enterprise Products Partners Shakes Off Several Quarters of Flat Results, Boasts a Strong First Quarter

Investors expected that it was only a matter of time before Enterprise Products Partners (NYSE: EPD)would manage to post a quarter with strong growth. After bringing billions of dollars' worth of new assets on line in 2016, the midstream giant was supposed to benefit from any uptick in oil and gas activity.

It appears this was that quarter investors were waiting for, as Enterprise was able to show spectacular growth across the board. What's even more promising is that growing production from the Permian is now fueling another wave of expansion projects. Let's check in with the company's most recent quarterly results to see what fueled the impressive showing and why management chose now to start stepping on the growth pedal again.

Image source: Getty Images.

Enterprise Products Partners' earnings: The raw numbers

| Results* | Q1 2017 | Q4 2016 | Q1 2016 |

|---|---|---|---|

| Gross operating margin | $1,469 | $1,357 | $1,324 |

| Net income | $771 | $670 | $670 |

| EPS | $0.36 | $0.31 | $0.32 |

| Distributable cash flow | $1,129 | $1,031 | $1,054 |

*IN MILLIONS, EXCEPT PER-SHARE DATA.DATA SOURCE: ENTERPRISE PRODUCTS PARTNERS EARNINGS RELEASE.

For several prior quarters, Enterprise Products Partners' earnings were more or less holding serve. Declines in production and drilling activity across the U.S. meant its existing pipes, storage facilities, and processing plants were experiencing lower demand, but it was able to offset those declines with earnings from new assets coming on line.

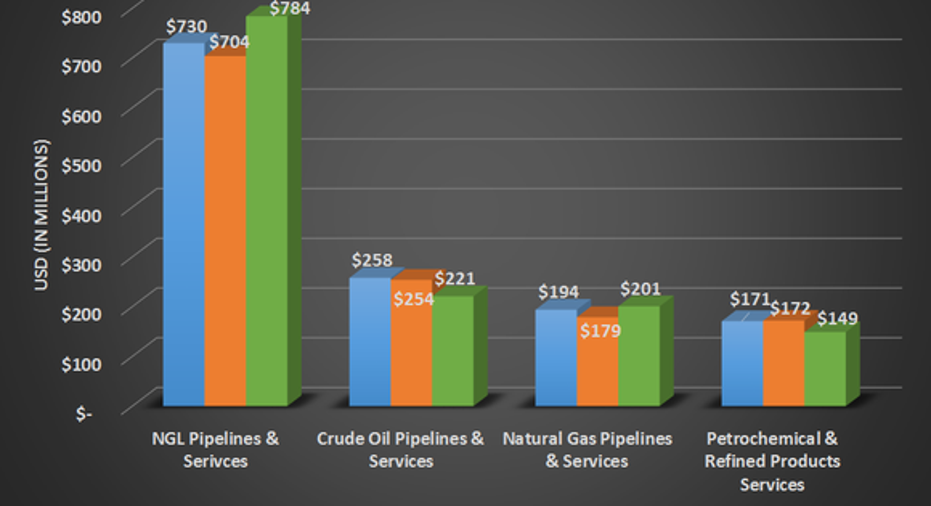

This quarter, though, earnings had their breakout quarter as volumes across Enterprise's system picked up in earnest. Pipeline volumes for liquids -- crude oil, refined products, and natural gas liquids (NGL) -- and marine storage terminal volumes were both at all-time highs for the company. Also, several of its new natural gas processing plants are still in the process of ramping back up, so volumes there should increase in the coming quarters.

DATA SOURCE: ENTERPRISE PRODUCTS PARTNERS EARNINGS RELEASE. CHART BY AUTHOR.

The one place investors could probably nitpick is the natural gas pipelines and services business, which saw both volume and gross operating margin declines. It should be noted, though, that the company hasn't been adding a lot of new assets to this particular business segment of late.

What happened with Enterprise Products Partners this quarter?

- Total capital spending for the quarter was $460 million. Management expects total capital expenditures for the year to be $2.7 billion to $3 billion. That is a $500 million increase in spending from guidance provided in the company's analyst-day presentation in March. The increase in spending has to do with a recent acquisition, as well as accelerating the development of several projects.

- Management maintained its distribution growth rate by increasing its payout to shareholders by 5.1%. That was the 51st consecutive quarterly payment increase.

- The distribution coverage ratio for the quarter was 1.3, which meant management retained about $238 million in distributable cash flow to be used in its capital program.

- Management decided that growing activity in the Permian Basin meant it was time to accelerate the development of several projects. It gave the green light for the 240,00-barrel-per-day Shin Oak NGL pipeline that will originate in the heart of the Permian and terminate at Enterprise's Mont Belvieu NGL fractionation complex; it will expand its Midland-to-Sealy crude oil pipeline by 50%, to 450,000 barrels per day; and it will expand its NGL transportation and storage infrastructure in the Houston-Mont Belvieu area to increase capacity to its export terminals.

- The addition of these projects means Enterprise's project backlog stands at $8.4 billion. Management anticipates these facilities will all come on line by 2020.

- Enterprise also made a splash by acquiring private natural gas transportation company Azure Midstream Partners for $189 million.

What management had to say

CEO James A. Teague expanded on the market forces that led management to accelerate its project development schedule:

Teague also mentioned that the management team is making progress on several other projects that would add to the backlog.

10-second takeaway

It's refreshing to see a nice bump in Enterprise's results after so many quarters of mostly flat results. Next quarter could also be a pleasant surprise as projects worth $2.6 billion are slated to come on line, headlined by the company's new propane dehydrogenation facility (producing propylene). Management also keeps the development pipeline filled with new projects, which should allow the company to maintain its distribution growth for several more years in a row.

10 stocks we like better than Enterprise Products PartnersWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Enterprise Products Partners wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of May 1, 2017

Tyler Crowe owns shares of Enterprise Products Partners. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.