Energy Transfer Partners' Earnings Reveal Why Dividend Lovers Should Avoid This Troubled MLP

Source: Energy Transfer Partners

The worst energy crash in half a century has left long-term dividend investors with a remarkable opportunity to buy high-quality, high-yield midstream MLPs at severely undervalued prices.

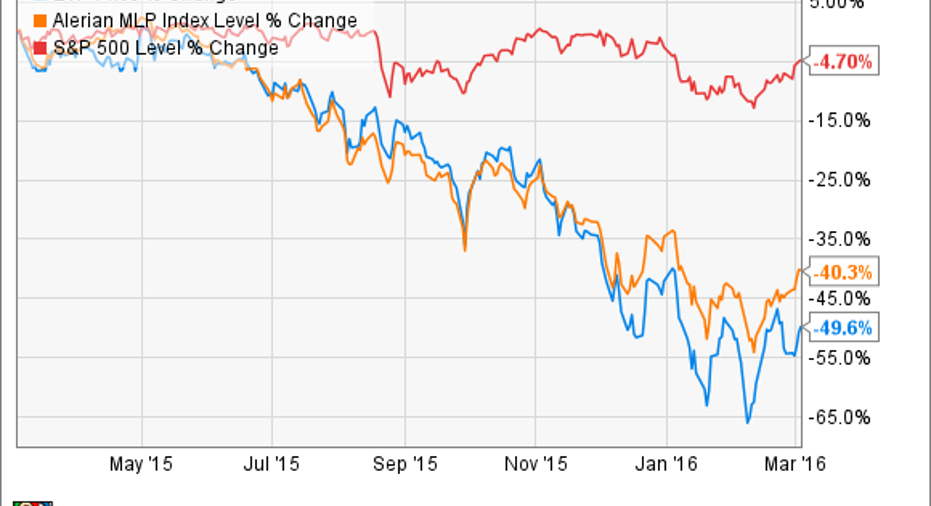

However, the challenge is determining which MLPs truly represent great values and which are high-yield value traps. Take for instance, Energy Transfer Partners which has underperformed its peers over the past year by a significant margin.

A quick check of Energy Transfer Partners' full year 2015 resultsreveals three troubling reasons why Wall Street is right to hate Energy Transfer Partners. More importantly, it shows whyall but the most high-risk income investors would likely be smart to avoid it.

2015 earnings revealsome major concerns

| Metric | 2014 | 2015 | Change |

| Adjusted EBITDA | $5.71 Billion | $5.714 Billion | 0% |

| Distributable Cash Flow (DCF) | $3.249 Billion | $3.445 Billion | 6% |

| Distribution Per Unit | $3.86 | $4.16 | 7.8% |

| Distribution Coverage Ratio (DCR) | 1.59 | 0.99 | (37.7%) |

Sources: earnings release, Yahoo Finance

Given Energy Transfer's business model that's built on long-term, fixed-fee contracts -- which are theoretically immune from commodity prices -- what explains 2015'sweak results; especially the alarmingdecline in the MLP's coverage ratio? The answer lies in several problems that make Energy Transferone of the poorerchoices in this industry.

First, management chose to unwisely make distribution growth a priority in 2015, despite the continuing decline in energy and its unit price. This was probably to try to support the unit price which would theoretically make raising equity capital cheaper and more profitable.

However, Wall Street's panicked rush to dump all things oil and gas related overwhelmed the payout increases and the 150.1 million units Energy Transfer Partners'issued in 2015 ended up selling at extremely low valuations. Thisresulted in 42.2% year-over-year dilution that brought the more expensive payout to the brink of unsustainability.

Another negative factorlast yearwas that Energy Transfer's quarterly earnings revealed that its contract mix didn't provide nearly the cash flow security investor's expected. For example, while 80% of 2015 volumes were technically "fee-based," only 64% of its volumes were protected by minimum volume guarantees.

Thisexposed Energy Transfer Partners' to declining volumes and cash flows when oil and gas producers in North Texas, Oklahoma, and the mid-continent region began cutting back production.

Distribution profile is getting hammered by oil crash

- Yield: 14.4%

- Distributable cash flow per unit(2014, 2015, respectively): $7.56, $4.62

- Analyst 5 year annual distribution growth projections: 3.6%

As you can see Wall Street is pricing Energy Transfer Partners as if its distribution is at high risk of a short-term cut. In addition analysts aren't very optimistic about the MLP's long-termgrowth prospects.

Given Energy Transfer's 39% decrease in annual DCF per unit both facts are understandable. However, analystprojections are educated estimates at best and always need to be taken with a grain of salt. After all, Energy Transfer Partners does havea growth project backlog ofaround $9 billionscheduled to come online through the end of 2017that could theoretically boost its distribution coverage and future payout growth beyond Wall Street expectations.

Source: Energy Transfer Partners investor presentation.

In addition, its sponsor Energy Transfer Equity ,thanks toits 2015 $38 billion buyout of Williams Companies , oversees America's largest pipeline empire and has access to vast oceans of potentially valuable assets it could theoretically use to bail out its troubled MLP.

So is the market wrong about Energy Transfer Partners? Is it mispricing this high-yield MLP creating a potentially lucrative profit opportunity you should consider taking advantage of? I believe the answer to be "no" because of the biggest risk facing Energy Transfer Partners' long-term investment thesis.

Major liquidity problems make profitable growth extremely difficultThe midstream MLP industry is incredibly capital intensive and partnerships have only three sources of funding: excess DCF, debt, and equity. Thanks to management's unwisely aggressive payout growth policy last year Energy Transfer Partners' barely sustainable DCR means that it's almost completely dependent on debt and equity markets to fund its ambitious growth plans.

Managementis quick to point out that it has $1.36 billion in available borrowing power remaining under its $3.5 billion revolving credit facility, which has an interest rate of just 1.86%.

However, given the MLP's debt/EBITDA or leverageratio of 4.5, (as measured under its credit agreements) it might not actually be able to borrowthe full amount because that same credit facility includes covenants that limit its leverage ratio to 5.0.

As for financial salvation coming from Energy Transfer Equity, investors shouldn't count on that because it turns out that the Williams Companies acquisition, given current market conditions, has become a nightmare.

The New York Times recently reported that Energy Transfer Equity is desperate to kill the deal, which would force Energy Transfer Equity to raise $6 billion in very expensive cash to pay Williams Companies investors. In fact, with the Williamsdeal now potentially no longer profitable,Energy Transfer Equity is rumored to have offered Williams $2 billion to walk away but due to the terms of the deal, only Williams investors, (or a highly unlikelyEnergy Transfer Equity bankruptcy), can kill the merger.

Bottom lineEnergy Transfer Partners' may not be the worst midstream MLP investment prospect you can buy but it's also far from the best. Given its: relatively poor contract mix,limited access to cheap growth capital, and itssponsor's own financial difficulties, I think itwise for dividend investors to steer clear of this troubled pipeline giant for now.

The article Energy Transfer Partners' Earnings Reveal Why Dividend Lovers Should Avoid This Troubled MLP originally appeared on Fool.com.

Adam Galas has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.