Emerson Electric: Worth Buying As a Dividend Aristocrat?

For those on the hunt of dividend yield, industrial stalwart Emerson Electric's (NYSE: EMR) nearly 3.9% dividend yield is surely attracting some attention. Unfortunately, investing is rarely as simple as picking out a stock based on yield, so I thought I would discuss some of the pros and cons of buying dividend aristocrat Emerson Electric for its yield.

The case for Emerson ElectricA brief summary of the key points, starting with the pros:

- There's a history of strong cash-flow generation across the business cycle.

- According to management's guidance, the cash-flow numbers will stack up for the next few years.

And now the cons:

- The spin-off of Network Power operations will see the company lose a good cash-flow business.

- Management plans for acquisitions, something that could lead to dividend growth in the future.

- The trading environment appears to be getting worse for the company.

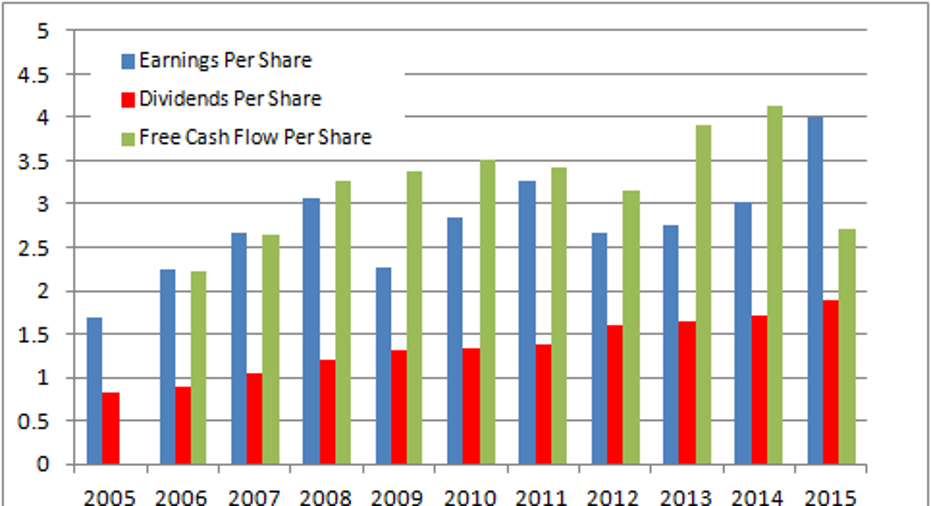

Show me the cash flowThe company has a history of generating good free cash flow. Even in the recession-hit year of 2009, free cash flow generation was strong and covered dividends paid by 2.6 times. Incidentally, the data in the following chart for 2015 is "reported" free cash flow (operating cash flow minus capital expenditures), but if adjusted for the $424 million paid in taxes on divestiture gains, free cash flow in 2015 would have covered the dividend by 1.7 times.

DATA SOURCE: EMERSON ELECTRIC PRESENTATIONS.

In addition, the near-term outlook is for good cash flow generation. On the earnings call, CEO David Farr forecast net sales to decline 6% to 8% in 2016, implying full-year 2016 sales in the range of $20.52 billion to $20.97 billion. When talking about a figure operating cash flow as a share of sales for 2016, Farr said, "I look at next year, we're going to be up around that 14%," which implies operating cash flow of around $2.9 billion at the midpoint of revenue guidance.

Assuming next year's capital expenditures are similar to this year's $685 million, it would mean free cash flow would come in at around $2.2 billion in 2016 -- enough to cover a dividend of $1.90 per share 1.7 times. Not bad for a company operating within a slump in its end markets.

Risks aheadOn the other hand, there are three longer-tem risks to the idea of buying Emerson Electric as an income stock. First, management plans to spin off its Network Power operations, implying a reduction in future cash flows. The segment generated 8.9% of segmental earnings during the past two years, and on the earnings call, Farr confirmed Network Power's "good cash flow generation, better than you normally see."

To be fair, Farr directly addressed the issue on the call by stating: "We will not be reducing our dividend. The new company, the new Emerson that comes out, when it comes out in 2017, let's say it's around $15.5 billion in size with margins of over 19%; margins generate very good levels of cash flow." However, the reduction in cash flows could constrain dividend growth in the future.

Second, any significant acquisition activity is likely to pressure the ability to increase dividends in the future. Market observers have long speculated that Rockwell Automation would be a good strategic fit, but given the enterprise value (market cap plus net debt) of around $14 billion, and the relative outperformance of Rockwell, it's hard to see how Emerson Electric could pull off a deal.

EMR Enterprise Value data by YCharts

Third, there's the omnipresent risk that end market conditions could deteriorate further for Emerson Electric. Although macroeconomic risk exists for all companies, Emerson has been particularly hard hit by recent conditions.

Foolish takeawayThe company's dividend looks sustainable for the next few years, and it's a genuine candidate for dividend hunters. Longer-term investors will want to keep an eye out for management's commentary on future plans. Any kind of large-scale deals -- for example, with Rockwell Automation -- could put pressure on dividend growth, and stabilizing earnings in the next year or so is important, too. After weighing the evidence, this is an attractive dividend aristocrat for income-seeking investors willing to stomach modest long term risks.

The article Emerson Electric: Worth Buying As a Dividend Aristocrat? originally appeared on Fool.com.

Lee Samaha has no position in any stocks mentioned. The Motley Fool recommends Emerson Electric. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.