Electronic Arts Stock Up 500% Over Last 5 Years: What's Next?

Over the last five years, the S&P 500 Index is up about 70%. This return is no match for Electronic Arts' (NASDAQ: EA) roughly 500% return over the same time period,but what can investors expect for the next five years? Will the stock continue to be a home run for shareholders?

We'll review how the stock delivered its massive run over the last five years, and what expectations investors should hold for the next five.

How Electronic Arts stock delivered 500%

EA has fueled its run with in-game content sales from hit franchises like Battlefield. IMAGE SOURCE: ELECTRONIC ARTS INC.

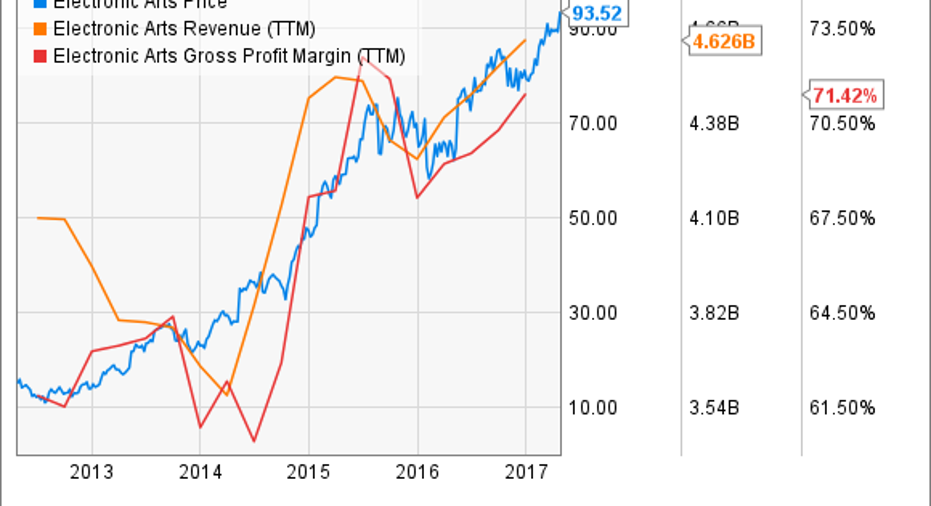

The video game industry has been undergoing a very profitable shift from physical sales of game discs to digital distribution, where players can purchase and download games directly through their consoles. This has been a common method of buying games for a long time with PC gamers, but it's just now catching on with console gamers.There has been no greater beneficiary of this business model shift than Electronic Arts.

In April 2012, EA had just wrapped up its fiscal 2012 year ending in March, where it reported $4.1 billion in net revenue and $0.23 in earnings per share.The company was in the middle of a major turnaround effort after reporting losses on the bottom line for several years. Management was aggressively pursuing higher-margin digital revenue sources, including mobile games and additional in-game content distributed directly to gamers via console, in order to position the company for long-term profitable growth.

The reason for EA's phenomenal stock performance cannot be explained by any new blockbuster games released, as the company is still producing the same hit titles, such as FIFA, Battlefield, and Mass Effect. Total revenue hasn't grown much, as EA is expected to report $4.8 billion in revenue for fiscal 2017, a cumulative increase of only 17% over fiscal 2012.

The main reason for the stock's 500% gain is that digital revenue went from less than 30% of total revenue five years ago to 56% for the trailing-12-month period ending December 2016, as more gamers continued to purchase games, along with additional in-game content, directly through their consoles as opposed to buying physical game discs.This caused gross margin to expand from 61.4% in fiscal 2012 to an expected 72.1% for fiscal 2017.

The increase in gross profit dropped all the way to the bottom line as EA is expected to report $3.83 in earnings per share for fiscal 2017, a compound annual growth rate of 75% since fiscal 2012.In April 2012, EA stock traded for about $15.50 per share, and the trailing-12-month PE ratio was 67 -- expensive by conventional standards.However, the high valuation was a sign that investors were expecting rapid growth in earnings as management pursued its turnaround strategy -- and EA delivered, big time.

What to expect over the next five years

Since the company is further down the line in building out its digital revenue channels across mobile games and direct buying through consoles, I expect EA to grow its earnings, but nowhere near 75% per year over the next five years. Here's why investors should lower their expectations.

1. Slowing digital revenue growth: Although digital revenue is still growing fast, at 18% over the trailing-12-month period, this is way down from the 47% growth rate EA was posting five years ago, when the company was just getting the ball rolling on its digital revenue opportunities.

2. Moderating earnings growth: Stemming from slower digital revenue growth, the last three years have shown a moderating growth rate in earnings per share. EA's fiscal 2017 expected earnings should show 21% year-over-year growth (assuming the company reports $3.83 for full-year earnings per share), which is down from the previous year's 30% growth rate.

IMAGE SOURCE: Electronic Arts.

EA's 21% growth rate for fiscal 2017 was based on a year when the company released a new Battlefield version, one of its best-selling games. For fiscal 2018, the company will be releasing a newStar Wars:Battlefront game, which produces lower margins than Battlefieldbecause of the cost of the licensed content EA pays to Walt Disney'sLucasfilm subsidiary.As a result, analysts are expecting EA's earnings growth to slow to 8% in fiscal 2018, with growth through the next five years expected to average 16.5% per year.

Electronic Arts should be a rewarding investment

I expect physical sales of games will continue to slowly decline, digital revenue will continue growing around 15% per year or faster, and gross margin will continue to gradually expand over the next five years as digital revenue becomes a greater percentage of total revenue.

While I wouldn't expect the stock to return anything close to 500% by 2022, I think analyst estimates of mid-teen level growth are very reasonable, and with the stock trading for 22 times fiscal 2018 expected earnings, investors are arguably getting a good deal.

10 stocks we like better than Electronic ArtsWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now...and Electronic Arts wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of April 3, 2017.

John Ballard has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Walt Disney. The Motley Fool recommends Electronic Arts. The Motley Fool has a disclosure policy.