Don't Let Your House Trap You in a Poor Retirement

Image source: Pixabay.com.

According to the U.S. Census Bureau, most of Americans' net worth is tied up in their houses. While a home can provide a wonderful place to raise a family and great protection from the elements, your home may actually be standing in the way of you building your retirement nest egg.

The reason? Houses cost money. You're either paying interest on a mortgage, or you have a lot of cash tied up in an asset that may only appreciate at around a 3% rate.You pay property taxes. You pay upkeep, maintenance, and insurance. Additionally, many of those costs are higher the more your house is worth, which means if you bought a bigger house than you needed as a way to build your retirement nest egg, you're that much more exposed to those costs.

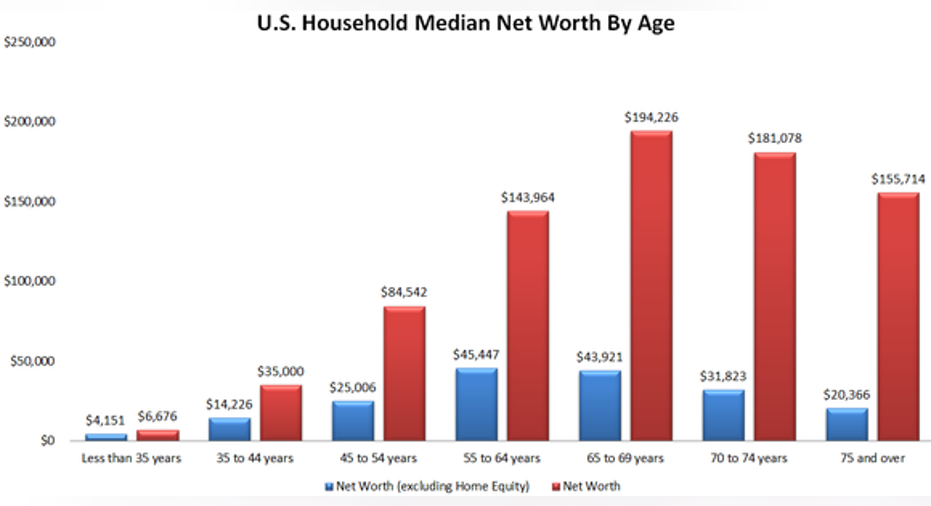

Is this the retirement you want? As the chart below shows, a household's net worth typically peaks at almost $200,000 near a traditional retirement age around 65 -- with over $150,000 of that net worth tied up in home equity. Even more concerning for a retiree, look at both the size and the direction of the blue bar that measures net worth excluding home equity. It drops the deeper into retirement people get, and at only around $20,000 for those age 75 and up, it hardly provides a one-time-use emergency fund, much less a nest egg.

Data source: U.S. Census Bureau.

As a retiree, you will be relying on your assets, any pension you may get, and Social Security to cover your costs of living. Your home is an asset -- but it's one you have to pay to keep, rather than one that pays you for owning it. In addition, reverse mortgages -- often touted as a way to get money out of your home in retirement without selling it -- tend to be incredibly expensive.

Your home can be an incredible source of comfort for you and your family, but you need to tread carefully with it if you want it to help, rather than hinder your retirement plans.

How to think about housing in retirement When you retire, you'll still need somewhere to live, but the needs your house fulfills change as well. Key changes include:

- Location: As a retiree, you're no longer tied to a location based on your commute time, and if your children are grown, the school district matters less, too. You don't have to move far away from friends and family, but you could easily find that a few miles could mean a substantially lower total coston a home that meets your needs as a retiree.

- Size: In any given area, smaller houses usually cost less than larger ones do -- both from a cost to acquire and a cost to operate perspective. Lower taxes, lower utility bills, lower maintenance costs, and lower insurance costs can all be yours if you're able to downsize as a retiree. If you're officially an empty nester, shrinking the nest can shrink its costs without sacrificing what you really need.

- Ability to age in place: The later in retirement you get, the tougher mobility will probably become. You can likely extend your independence (and stave off the costs of assisted living) by retiring to a home that's designed around aging in place. Things like walk-in-showers with safety bars and seats, first-floor master bedrooms, convenient access to transit, and minimal yard work can make it easier to stay independent for longer at a lower total cost.

Why this matters to you The less money you have tied up in your house, the more your net worth shifts from the red bar in the above chart to the blue bar. That gives you better flexibility every month and a better buffer against the unexpected. Additionally, the less you're spending every month on your house, the farther the money in that blue bar will go toward your other priorities in retirement.

So, if you're after a great retirement, keep your housing costs down both in terms of the money you have tied up in your home and in terms of your monthly household operating costs. Combine that with a home designed around allowing you greater independence for longer, and you have a recipe for turning your house from a trap keeping you from a great retirement into a tool to help you rule it.

The article Don't Let Your House Trap You in a Poor Retirement originally appeared on Fool.com.

Chuck Saletta has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.