Do Fat Dividends Make General Motors a Buy?

Two big reasons why dividend investors should consider GM: CEO Mary Barra and the advanced technology -- and thinking -- that went into the battery-electric Chevrolet Bolt. Image source:General Motors.

By historical measures, General Motors' stock is cheap. It's trading at around 4.5 times earnings, versus a historical valuation of more like 10 times earnings. More to the point, that low stock price also makes for a great dividend yield, currently about 5.2%.

That yield makes GM shares tempting. But is the Detroit giant really a buy right now?

The case for buying GM

GM still doesn't get a lot of respect among American investors (or American car shoppers, for that matter). But GM has come a long way since its crash into bankruptcy in 2009. That crash followed decades of mismanagement, though even then, GM had begun the process of finally getting its act together, improving its manufacturing and making big strides in quality.

That process accelerated under the new management that arrived after GM came out of bankruptcy. Today, GM has a "fortress" balance sheet: As of the end of the first quarter, GM had $30.6 billion in cash and available credit lines, versus just $10.8 billion of well-structured long-term debt.

That wouldn't mean much if GM CEO Mary Barra didn't have a plan for growth -- and a plan to out-disrupt the Silicon Valley companies aiming to transform the way we get around. But she does, and the plans are already well under way.

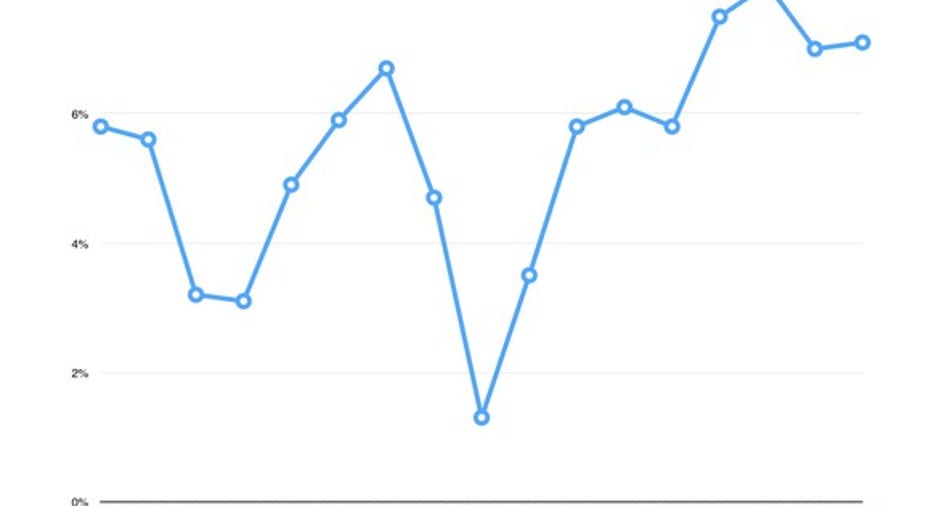

Barra's growth plan, announced in the fall of 2014, aims to put GM's profits on par with those of its closest global rivals, Toyota and Volkswagen , by boosting GM's global "EBIT-adjusted" (operating) profit margin to between 9% and 10% by early next decade (from 5.8% when the plan was first announced).

It's already making progress: GM's EBIT-adjusted margin was 7.1% last quarter.

Setting aside the recall mess that hurt GM's profits in the first half of 2014, the General's quarterly "EBIT-adjusted" profit margin has been trending upward over time. Data source: General Motors.

GM's also making tangible progress on another front: Fending off Silicon Valley "disruptors" like Tesla Motors , Alphabet's Google Self-Driving Cars project, and ride-hailing giant Uber. All are seeking, in various ways, to change the traditional model of private car ownership.

But Barra and her team are fighting back by keeping pace. Lots of automakers are talking a good game when it comes to the emerging world of "personal mobility," but few can match the action with which GM has backed its talk. GM is arguably leading the race to a self-driving car, its building its own ride-sharing business to compete with ZipCar (and not incidentally, to build brand awareness with urban 20-somethings), and investing in Uber rival Lyft -- with whom it will soon begin testing a fleet of self-driving Chevrolet Bolt taxis.

Long story short: Today's GM is in great financial shape and taking the right steps to ensure that its business endures and grows in the years to come.

Why GM might not be a buy

But all that said, there is a good reason to be concerned about GM, and that concern may be why the stock is cheap right now.

GM is a global company, but a big portion of its profits still come from truck and SUV sales in the United States. (In part, Barra's growth plan is about diversifying away from that dependence, but GM isn't quite there yet.) The good news for GM is that the U.S. new-car market is near record highs -- but that's also the reason for caution.

U.S. Light Vehicle Sales data by YCharts.

The chart above shows the pace of U.S. light-vehicle sales, expressed as a seasonally adjusted annualized number, for every month going back to the beginning of 2000. As you can see, the pace of sales plateaued for much of the last decade before the 2008 economic crisis. The good news is that sales are now close to where they were, and GM's profits have been strong.

But, the thinking goes, that might mean that U.S. auto sales are peaking. With its much-improved cost structure and hefty cash reserves, GM's not in serious danger if U.S. auto sales decline, or even if the U.S. plunges into a recession. A decline in U.S. sales, though,will squeeze GM's profits.

Will it put the company's dividend at risk? Barra and CFO Chuck Stevens have been cautious with GM's dividend, in hopes of sustaining it through any future downturn. But if the next recession is a steep one, it's possible that GM's dividend could get cut or even suspended for a few quarters.

The upshot: For patient investors, the potential rewards outweigh the risk

Full disclosure: I'm a GM shareholder, I reinvest the dividends, and I have no plans to sell. I think Barra and her team absolutely have GM on the right course, not only for survival but for bottom-line growth.

That said, GM shareholders like me might have to ride out a recession (and a few years of sluggish stock price growth, or even a decline) before we see the gains that Barra's plan looks likely to generate. Still, for patient investors who are willing to hold for five years or more, I think it's likely that a recession won't mean deep trouble for the General. In fact, if GM's stock spends some time in the doldrums, it might well be an opportunity for shareholders to dollar-cost average with those dividend reinvestments.

So to answer the question in the headline: Yes, I do think GM's dividend yield warrants serious consideration, and I think there's significant price upside, too. If you're willing to be patient, take a closer look.

The article Do Fat Dividends Make General Motors a Buy? originally appeared on Fool.com.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. John Rosevear owns shares of General Motors. The Motley Fool owns shares of and recommends Alphabet (A shares), Alphabet (C shares), and Tesla Motors. The Motley Fool recommends General Motors. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.