Dividend Investors: Meet the New HCP, Inc.

Image source: Getty Images.

As of October 31, 2016, HCP, Inc. (NYSE: HCP) completed its planned spin-off of its skilled nursing/post-acute care properties into a newly created REIT known as Quality Care Properties (NYSE: QCP), or QCP for short. Since the goal was to leave HCP with a stable portfolio of high-quality healthcare properties and produce a steady stream of income for shareholders, here's what you should know about the current state of HCP, currently yielding 5%, and what path the company plans to take from here.

What's left in HCP's portfolio?

The main objective of spinning off QCP was to rid the portfolio of skilled nursing/post-acute properties, which have been financially unreliable lately and depend largely on government reimbursement programs. The goal, as stated by HCP, was to create a portfolio of stable, high-quality, private-pay assets.

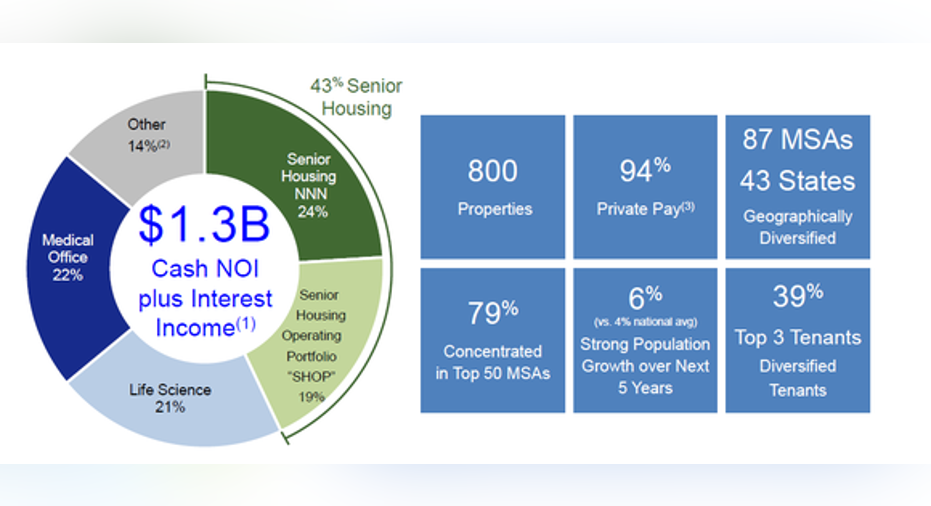

HCP had previously estimated what its post-spinoff portfolio would look like, but now we know for sure. The company has 800 properties spread across 43 states, 94% of which are now private-pay (read: stable). 43% of the portfolio is senior housing, 22% is medical office buildings, 21% is life science properties, and 14% is made up of other healthcare property types.

Image source: HCP presentation.

Current priorities

In a presentation released along with its third-quarter earnings, HCP outlines its current priorities. The first one is already done: Complete the spinoff of QCP, which was finalized on October 31. Three other near-term priorities were listed as well:

- Reduce the exposure to Brookdale Senior Living -- After the spinoff, Brookdale will account for 35% of HCP's income, a rather high concentration. Along with the earnings report, HCP also announced a deal to sell 64 of its Brookdale-occupied properties, which will reduce the concentration to 27% by the end of 2017. The transaction will also produce a higher overall occupancy rate as well as a more profitable portfolio.

- Improve balance sheet metrics -- HCP plans to use the proceeds from the QCP spinoff and the Brookdale sale to pay down debt.

- Become a leader in transparency and clarity -- HCP is taking steps to improve its disclosures to investors.

HCP's financial condition -- present and future

As I mentioned, one of HCP's main strategic priorities is to improve its balance sheet, so let's look at how things look now, and what the company hopes to achieve.

Between the QCP spinoff, the Brookdale sale, and other transactions, HCP expects a total of $3.35 billion in proceeds by the end of 2017's first quarter, virtually all of which will be used to pay down the company's debt.

This will immediately result in an overall leverage ratio of 45%, a fixed charge coverage of 3.75-to-one, and a debt-to-EBITDA ratio of about 6.5. By the end of 2017, HCP hopes to improve these metrics even further, and it has set rather ambitious long-term targets of leverage under 40%, fixed charge coverage less than 3.5-to-one, and debt-to-EBITDA in the range of 5.5 to 6.0. The goal is to regain the Baa1/BBB+ credit ratings the company formerly achieved and to have a sustainable portfolio of high-quality properties.

What's next?

Now that HCP has shed its unwanted assets, it can start to look toward the future. Currently, HCP has $810 million worth of properties in development, all of which are life science and medical office properties, and they are expected to produce a stabilized return on cost in the range of 7.5% to 8%.

This is certainly a good start, and over the next few years, I'd like to see the company grow in a gradual, sustainable manner by adding to its core property types without letting its debt levels creep up too high, and without its tenant concentration getting out of balance again. If HCP can do that, it will be well on its way to creating a stable and dependable stream of growing dividend income for its shareholders that can be sustained for decades.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early, in-the-know investors! To be one of them, just click here.

Matthew Frankel owns shares of HCP and QCP. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.