Can Amazon.com Inc. Hit $1,000 Per Share?

Shares of Amazon.com (NASDAQ: AMZN) have soared 60% over the past 12 months, butanalysts at J.P. Morgan, RBC Capital Markets, and Evercore ISI all believe that the stock could rise another 20% to $1,000 within the next two years. Is that target realistic, or will Amazon be pulled down by fundamental gravity before that happens?

Image source: Amazon.com.

What Amazon's valuations tell us

Amazon currently trades at 208 times earnings. That sounds lofty, but it's actually lower than itsprojected earnings growth rate of 366% this year. The stock's P/E has also been declining rapidly compared with previous years, thanks to the growing profitability of its Amazon Web Services (AWS) segment.

Source:YCharts

If Amazon hits the average earnings estimate of $5.82 per share this fiscal year, a stock price of $1,000 would imply a trailing P/E of 172 -- which looks reasonable compared with Amazon's historical P/E ratios.

Amazon currently trades at 80 times forward earnings, which matches the 80% earnings growth analysts expect next year. If Amazon matches the average earnings estimate of $10.50 per share for next year, a stock price of $1,000 would equal a trailing P/E of 95 -- its lowest multiple since late 2011. By these measures, a $1,000 price target could be considered conservative based on Amazon's historical multiples.

What's fueling Amazon's growth?

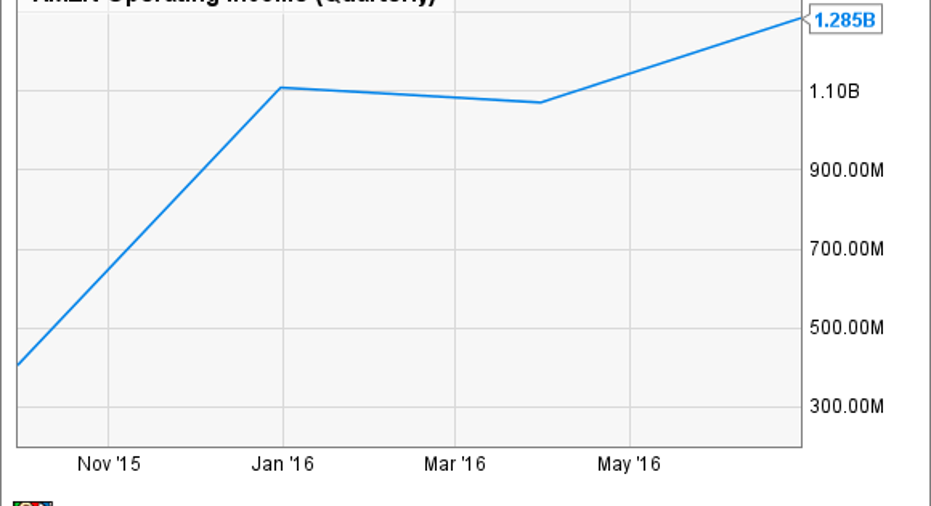

Of Amazon's revenue, 90.5% came from its North American and international marketplace businesses last quarter, while the remaining 9.5% came from AWS. But AWS revenue rose 58% annually during the quarter, as revenue at its North American and international marketplaces respectively rose just 28% and 30%.

More importantly, AWS operating profit surged 138% and accounted for 56% of Amazon's operating income -- making it the company's most profitable business unit, with an operating margin of 25%. By comparison, the North American marketplace had an operating margin of 4% while the International marketplace posted an operating loss. Therefore, AWS became Amazon's main earnings growth driver over the past 12 months.

Source:YCharts

AWS is the world's largest cloud computing platform, withan annual run rate of $11.5 billion as of last quarter, and it doesn't show any signs of slowing down. It launched its sixth AWS region in the Asia Pacific region in Mumbai last quarter, bringing its total coverage area to 35 availability zones across 13 technology infrastructure regions, and it plans to add nine new availability zones across four regions next year.

It also added 422 new services and features to AWS within the first half of 2016, which represents an acceleration from the 722 services and features it added throughout all of 2015.

AWS profits support marketplace growth

AWS's growing profitability gives Amazon more financial freedom to expand its Prime ecosystem. The $99-per-year service offers free same-day delivery on select items, discounts, unlimited video streaming, e-books from the lending library, unlimited cloud storage for pictures, and other perks.

Amazon sells Kindles, Fire TV set-top boxes, Echo smart speakers, DRS-enabled appliances, and Dash buttons to keep users tethered to that ecosystem. It's alsobeen linking new services such as grocery deliveries, restaurant deliveries, and home services to Prime.

This prisoner-taking strategy works wonders. Back in July, research firm CIRP claimed thatAmazon had 63 million Prime members in the U.S., an increase of 19 million from last June. It also estimated that Prime shoppers spent an average of $1,200 last year, versus $500 for non-members. While Prime margins will remain thin, its growth will help Amazon gain market share and further marginalize its rivals with economies of scale. That's why analysts expect Amazon's sales to climb 28% this year and another 22% next year.

But mind the headwinds ...

Amazon is formidable, but it isn't invincible. Apple, one of Amazon's major AWS customers, recently moved some ofits services to Alphabet's Google Cloud to reduce its dependence on AWS. Spotify also moved its infrastructure to Google Cloud instead ofAWS or Microsoft's Azure.

These moves indicate that AWS's dominance of the cloud platform market isn't absolute, and that competition from Google, Microsoft, and others could still spark fresh pricing wars and reduce the segment's profitability. On the e-commerce front, a resurgent Wal-Mart could hurt Amazon with aggressive price matching, curbside pickups, and subscription-based delivery services.

I believe that Amazon could easily rise above $1,000 in the near futuresince that price is heavily supported by its earnings growth and historical valuations. However, I think investors should still pay close attention to the challenges that its AWS and marketplace businesses could face.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Leo Sun owns shares of Amazon.com. The Motley Fool owns shares of and recommends Alphabet (A and C shares), Amazon.com, and Apple. The Motley Fool owns shares of Microsoft and has the following options: long January 2018 $90 calls on Apple and short January 2018 $95 calls on Apple. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.